A founder signs a lease in Toronto, then hears the building owner may sell. Another founder in New York is reviewing a shareholders’ agreement and spots a right of first offer buried in the transfer section. In both situations, the clause’s significance is often underestimated. Mayo Law regularly sees right of first offer terms become either a practical business tool or a source of avoidable conflict, especially when a deal crosses Ontario and New York lines.

A right of first offer gives one party the first chance to make an offer before the owner markets the asset to others. That sounds simple. The hard part is how the clause is triggered, how price gets set, what happens if talks fail, and where enforcement lands if the parties are in different countries.

Understanding the Right of First Offer in Your Business

A right of first offer usually appears in leases, shareholders’ agreements, partnership arrangements, and strategic joint ventures. The owner decides to sell, lease, or transfer an asset, then must approach the rights holder first. Only after that process runs its course can the owner go to the outside market, subject to the contract’s limits.

That matters because these rights are common. Approximately 30% of commercial leases worldwide include a right of first refusal or right of first offer clause, according to the American Law and Economics Review source cited here. In practical terms, if you’re leasing space in Toronto or New York, or buying into a closely held company, you may encounter one sooner than you expect.

Where founders usually see it

- Commercial leases: A tenant wants a shot at buying the premises or taking adjacent space.

- Shareholder exits: Founders and investors want an orderly process before stock goes to an outsider.

- Joint ventures: One party wants early access if the other decides to sell.

- SME acquisitions: Strategic buyers use it to preserve a future path to control.

The clause can be useful, but only if it matches the transaction. In early-stage companies, people often copy language from another agreement without thinking through timing, valuation, or financing realities. That shortcut tends to create problems later.

For founders building their structure from scratch, the best time to think about transfer rights is when you’re also thinking about governance and formation. A practical starting point is this guide on Ontario incorporation steps, costs, and timelines, because entity setup and transfer rights usually belong in the same planning conversation.

Practical rule: A right of first offer isn’t just a purchase right. It’s a negotiation system. If the system is vague, the dispute is built in from day one.

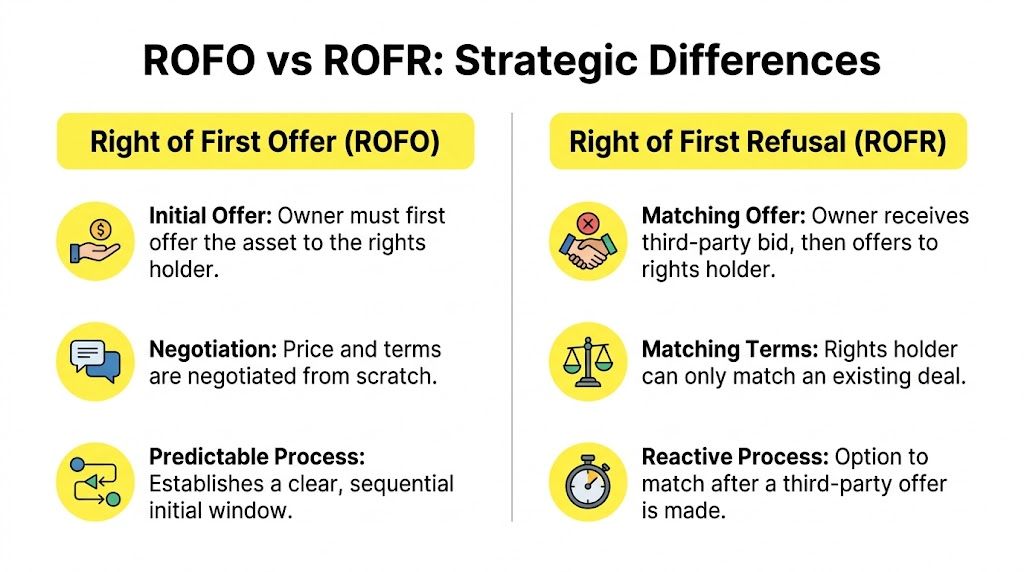

ROFO vs ROFR A Critical Distinction for Your Strategy

A right of first offer (ROFO) and a right of first refusal (ROFR) are not interchangeable.

A ROFO gives the holder the first word. The owner must come to that holder first, before going to the market. A ROFR gives the holder the last word. The owner shops the asset first, gets a third-party deal, then asks the holder whether they want to match it.

Why the difference changes leverage

With a ROFO, the seller controls sequence and timing. The parties negotiate from the front end. That often makes the process more predictable.

With a ROFR, an outside bidder may spend time and money on diligence, only to be used as the benchmark offer. That can cool bidding interest. Some buyers prefer to avoid deals where their offer might be matched.

| Issue | ROFO | ROFR |

|---|---|---|

| Trigger | Owner decides to sell | Third-party offer arrives |

| Holder’s role | Makes first offer | Matches existing offer |

| Seller control | Higher at the start | Reduced after market testing |

| Third-party friction | Lower | Often higher |

Why poorly designed ROFRs can backfire

Britain's Landlord and Tenant Act 1987 introduced a statutory ROFR that ended up strengthening landlord bargaining power instead of helping tenants. The historical summary in Harvard Business School's analysis explains that the structure let sellers use the tenant's matching right to deter lower third-party bids, and the provision was repealed after only one year because it distorted the market and failed to help tenants as intended. See the Harvard discussion of when rights of first refusal are a bad deal.

That example matters because founders often assume the stronger holder protection is always better. It isn't. A right that looks protective on paper can reduce real market participation or create pressure points that work against the intended beneficiary.

A useful way to choose

Use a ROFO when the parties value a cleaner sequence, want direct negotiation first, and need a process that fits a future exit or property transfer.

Use a ROFR only if the holder's priority is matching a real market-tested deal and both sides understand the friction that may follow.

The label doesn't decide the outcome. The mechanics do.

How the Right of First Offer Process Works

A good right of first offer clause follows a sequence. If the sequence is muddy, everyone argues about whether the right was properly triggered.

Step one is the trigger event

The clause should say exactly what activates the right. In real estate, that may be the owner's decision to sell. In a company agreement, it may be a shareholder's intent to transfer shares.

If you don't define the trigger, parties fight over whether informal conversations, board discussions, refinancing pressure, or asset reorganizations count.

Step two is notice

In cross-border commercial real estate practice, ROFO clauses commonly give the holder a 30 to 60 day window to submit an offer after notice, as described in LoopNet's explanation of how a right of first offer works. The notice usually needs to include the material business terms and enough information for the holder to evaluate the deal.

A usable notice clause should answer three questions:

- How is notice sent: email, courier, certified mail, or a defined contract portal.

- When is it deemed received: on sending, on delivery, or after a set period.

- What must it contain: price expectations, asset description, key conditions, and timing.

Step three is the negotiation window

The holder gets an exclusive period to respond and negotiate. Weak drafting often becomes evident. If the clause says the parties will negotiate "in good faith" but says nothing about timelines, required content, or what counts as rejection, the clause may become a stall tactic.

This is also where deal counsel should line up financing, diligence, and board approvals in advance. That is especially true in stock transfers and founder exits. If your transfer documents are part of a larger cap table package, this article on stock purchase agreements is often relevant because the transfer mechanics need to align.

Step four is release to market

If the holder declines or the parties don't reach terms, the owner is usually released to market the asset to others. But that release should not be unlimited.

Common post-negotiation protections include:

- A price floor: the seller can't accept less favorable terms from an outsider without coming back.

- A time limit: if no outside deal closes within the release window, the ROFO resets.

- A scope limit: the release applies only to the asset and terms described in the original notice.

Without those protections, the first offer process loses meaning.

Drafting an Enforceable ROFO Clause A Checklist

The difference between a workable right of first offer and a litigation exhibit is usually drafting discipline.

Define the asset and the trigger

Start with precision. Is the right tied to shares, membership interests, IP, a specific property, a business division, or a bundle of assets?

Then define the trigger with equal care.

- Sale decision: Is board approval enough, or does there need to be a signed intent to sell?

- Indirect transfers: Does a sale of the parent entity trigger the right?

- Exempt transfers: Family transfers, affiliate reorganizations, or financing transactions may need carve-outs.

A startup clause often fails because it covers direct equity sales but ignores asset sales. That gap matters in tech deals where the primary value sits in IP, contracts, or a subsidiary.

Lock down notice and timing

Notice terms should be unglamorous and exact. That's a compliment. Good contract language leaves little room for improvisation.

Include:

- the delivery method

- the contents of the notice

- the holder's response deadline

- the period for exclusive negotiations

- the date the owner may go to market if no deal closes

A founder should also ask whether the right is personal or assignable. In many cases, a personal and non-assignable ROFO gives the owner more control and reduces surprise transfers.

Build in a valuation mechanism

Many clauses often falter. A key gap in many ROFO clauses is the failure to address valuation disputes. The WeConservePA guide notes that, for startups, valuation can fluctuate 30% to 50% between funding rounds, making independent appraisals or market-based adjustment mechanisms important if the parties want to avoid deadlock. The discussion appears in this guide on rights of first offer and rights of first refusal.

That doesn't mean every ROFO needs an appraisal. It does mean the agreement should say what happens when the holder's offer and the owner's expectations are far apart.

Options include:

- Independent expert determination: Useful when both sides want speed and a narrow valuation question answered.

- Appraisal process: Often better for real estate or tangible asset transfers.

- Formula pricing: Sometimes used in shareholder agreements, though it can age badly if the business changes.

- Market reset clause: If no outside buyer appears on comparable terms, the parties revisit the holder's offer.

For founders, this issue often belongs beside the rest of the transfer and governance package. If you're reviewing buy-sell mechanics, deadlock protections, and transfer restrictions together, this piece on shareholders' agreements and founder dispute prevention is closely connected.

Drafting note: If the clause says "fair market value" and nothing else, you've probably deferred the hardest issue instead of solving it.

State the post-failure rules

The owner's freedom after failed negotiations should be clear. Can the owner sell to a third party at any price? Only on no more favorable terms? Within a fixed time? With revised terms only after a renewed offer?

These details shape actual advantage more than the title of the clause.

Match remedies to the deal

A ROFO in a lease amendment may need different remedies than a ROFO in a founder buyout. If the asset is unique, specific performance may matter. If the transaction is one piece of a larger commercial relationship, damages or a buy-sell reset may be more realistic.

Negotiation Strategy for Holders and Owners

A right of first offer shifts bargaining power. It doesn't eliminate bargaining.

If you're the owner granting the ROFO

Don't grant a broad right just to get the main deal signed. Ask what you are giving up later.

In U.S.-Canada partnership agreements, ROFOs often produce 12% to 18% premium outcomes for sellers over ROFR alternatives because the seller controls the sale sequence and avoids some of the delay and market chill that matching rights can create, according to the summary at ContractsCounsel's right of first offer overview.

That seller advantage is real, but only if the clause is tight. Owners usually do best when they negotiate:

- Narrow triggers

- Short response periods

- A clear release right after failed talks

- A prohibition on assignment by the holder

- A no-breach condition for the holder's exercise

If you're a founder granting investors a ROFO, also think about transaction fatigue. Multiple rights layered across common, preferred, and side letters can jam an exit process.

If you're the holder receiving the ROFO

Preparation matters more than rhetoric. Once notice arrives, the clock runs quickly.

A holder should think through three issues before signing the clause:

- Can you finance the purchase fast enough

- Who approves the deal internally

- What information do you need in the owner's notice

If the clause doesn't require enough disclosure, the right may be too thin to use well. The holder should push for financial statements, material contract summaries, cap table details, or property diligence materials, depending on the asset.

Strategy in founder and investor exits

ROFOs can reduce friction in buyouts when nobody wants a surprise outsider at the table. They may also help a founder keep more control over process while still offering investors a defined priority.

A smart holder doesn't wait for the notice. They line up capital, internal approvals, and valuation assumptions while the relationship is still stable.

Cross-Border ROFOs US-Canada Enforcement and Tax Rules

The biggest drafting mistake in cross-border deals is assuming the right is enforceable solely because the contract says so. It may not be, at least not in the way the parties expect.

A major gap for U.S.-Canada businesses is how ROFO rights are enforced across borders. The Horn Wright discussion notes that remedies such as specific performance may differ between New York and Ontario, which is why choice-of-law and dispute resolution terms are central to making the right meaningful. See the discussion of right of first offer versus right of first refusal in cross-border context.

Choice of law is not housekeeping

If the grantor is in New York, the holder is in Ontario, and the asset sits in a different jurisdiction from both, you need to decide what law governs:

- the existence of the ROFO right

- the notice process

- the remedy for breach

- the forum where the dispute gets heard

These are separate questions. Parties often collapse them into one sentence and create ambiguity.

Litigation versus arbitration

Cross-border parties often prefer arbitration because it may offer a cleaner path for confidentiality and enforcement. That said, some disputes still need urgent court relief, especially if one side is trying to close a transfer quickly.

For businesses that expect cross-border enforcement issues, it may be worth comparing litigation clauses with structured arbitration provisions. This overview of arbitration in Canada, including Ontario and international enforcement is a useful place to start.

Tax should be addressed early

Tax doesn't disappear because the clause is in the back of the contract. A ROFO on real estate, shares, or IP may trigger very different tax consequences depending on the asset and where the parties sit.

At a minimum, parties usually want tax advisors and transaction counsel aligned on:

| Issue | Why it matters |

|---|---|

| Asset type | Share sale and asset sale treatment may differ |

| Jurisdiction | Ontario and New York rules won’t line up perfectly |

| Timing | Exercise timing can affect reporting and withholding |

| Structure | The same commercial result may be taxed differently |

A common business mistake is negotiating the commercial right first and treating tax review as cleanup. In cross-border deals, cleanup often turns into renegotiation.

Key Considerations and Common Pitfalls to Avoid

Most right of first offer disputes start with a clause that felt "good enough" when everyone was optimistic.

The most common problems are predictable.

Pitfalls that show up repeatedly

- Ambiguous triggers: If nobody can tell when the right starts, the right invites conflict.

- Thin notice requirements: A holder can't make a serious offer without enough information.

- No valuation mechanism: In a volatile company or active real estate market, silence on price disputes creates deadlock.

- Unlimited release rights: If the owner can walk away and sell on materially better terms without coming back, the holder's protection may be mostly cosmetic.

- Cross-border blind spots: Enforcement, forum, and remedy language often get too little attention.

- Tax left to the end: By then, business terms may already be locked in.

What strong clauses usually have in common

They are specific. They separate trigger, notice, timing, valuation, release, and remedy into distinct provisions. They also reflect actual deal dynamics, rather than copying generic precedent.

If you're forming or expanding a U.S. operation, transfer rights should also fit your entity design and ownership structure. This guide on choosing the right entity for your U.S. business is relevant because entity choice and transfer restrictions often work together.

Rights of first offer work best when both sides know exactly what happens next. They work worst when the contract leaves the hard questions for later.

A right of first offer can be a smart tool for leases, founder exits, investor buyouts, and strategic acquisitions. But it has to be built for the actual transaction, especially when Ontario and New York are both in the picture.

If you're negotiating a right of first offer in a lease, shareholders' agreement, partnership arrangement, or cross-border acquisition, Mayo Law may help you evaluate the business trade-offs and draft terms that fit your structure in Ontario and New York. Build Your Business on Solid Legal Ground. Mayo Law advises startups and SMEs in Ontario and New York. Contact Mayo Law to discuss your needs.

LEGAL DISCLAIMER: The information provided in this article is for general informational and educational purposes only and does not constitute legal advice. Reading this article, visiting mayo.law, or contacting Mayo Law does not create an attorney-client relationship. The content of this article should not be relied upon as a substitute for professional legal counsel tailored to your specific circumstances. Legal outcomes depend on the particular facts and circumstances of each individual case, and no attorney can guarantee a specific result. Laws, regulations, and legal procedures are subject to change and may vary by jurisdiction. If you require legal assistance, you should consult with a qualified attorney licensed to practice in the relevant jurisdiction. Mayo Law expressly disclaims any and all liability with respect to actions taken or not taken based on the contents of this article.