When you're buying or selling a business, the Stock Purchase Agreement (SPA) is the single most important document in the entire transaction. It’s the legal blueprint that dictates every term of the deal. For entrepreneurs navigating a company sale or an acquisition, especially across the U.S.-Canada border, getting this agreement right is non-negotiable. At Mayo Law, our business law attorneys regularly advise startups and SMEs in Ontario and New York on these critical transactions, ensuring their interests are protected from start to finish. A well-drafted SPA can be the difference between a successful exit and a costly dispute.

What Is a Stock Purchase Agreement, Really?

At its core, a stock purchase agreement formalizes the transfer of a company's shares from the seller to the buyer. Think of it as the detailed rulebook for the sale, covering everything from the final price to the specific conditions that must be met before the keys are handed over.

This approach is fundamentally different from an asset purchase, where the buyer cherry-picks the assets they want—like equipment, real estate, or intellectual property—and leaves most liabilities behind.

In a stock sale, the buyer doesn’t just get the good parts; they acquire the entire business entity. This includes all its assets, contracts, permits, and, crucially, all of its liabilities. The company continues to operate without interruption, but the new owner inherits its complete history—both the triumphs and the skeletons in the closet.

Grasping this "warts and all" concept is the first step, as it shapes the deal's entire risk profile and determines how you need to protect yourself during negotiations.

Stock Purchase vs. Asset Purchase at a Glance

The choice between a stock and asset purchase carries significant legal and financial weight. This decision influences everything from due diligence to post-closing risk. Here is a brief comparison:

| Feature | Stock Purchase | Asset Purchase |

|---|---|---|

| What’s Being Sold? | Shares of the corporate entity. The buyer takes over the whole company. | Specific, chosen assets (and sometimes liabilities) of the business. |

| Continuity | The legal entity remains the same. Contracts and permits often transfer automatically. | The seller’s corporate entity remains. Assets must be individually retitled. |

| Liabilities | Buyer inherits all liabilities of the company, known and unknown. | Buyer generally only assumes liabilities they explicitly agree to take on. |

| Complexity | Often simpler from a transactional standpoint (fewer individual transfers). | Can be more complex, requiring new contracts, permits, and title transfers. |

While a stock purchase can be simpler on paper because existing contracts and permits usually stay in place, the catch is that the buyer takes on all the company's baggage. To learn more about how your business's legal form impacts these decisions, check out our guide on choosing the right entity for your U.S. business.

The Power and Nuance of SPAs

These agreements are powerful instruments. During the 2008 financial crisis, the U.S. Department of the Treasury used a specialized SPA to inject capital into Fannie Mae and Freddie Mac, committing up to $200 billion each to stabilize the housing market.

While people often use the term "equity purchase agreement" interchangeably, there's a small but important technical distinction.

- A Stock Purchase Agreement (SPA) is specifically for buying shares in a corporation.

- An Equity Purchase Agreement is a broader term for buying ownership in any business entity, including LLCs (where you buy "membership interests") or partnerships.

This inherent risk in a stock sale is precisely why the due diligence process and the negotiation of protective clauses in the SPA are so incredibly important.

Understanding the Key Clauses in an SPA

A well-crafted stock purchase agreement is the operational blueprint for the transaction. For anyone buying or selling a business in Ontario or New York, understanding these core components is the first, most crucial step toward a successful deal. While every SPA is tailored to the specific company, they all share a common anatomy.

Purchase Price and Payment Terms

This clause defines the total price for the shares, but how that price gets paid can be just as important as the amount itself. The price is often a mix of different components:

- Cash at Closing: The straightforward, immediate payment you receive (or make) the day the deal is finalized.

- Promissory Notes: This is a form of seller financing where the buyer pays off a portion of the purchase price over an agreed-upon timeline, with interest.

- Earn-outs: A portion of the payment is made contingent on the business hitting specific performance targets after the sale. This tool can help bridge valuation gaps.

- Working Capital Adjustments: A standard, but critical, adjustment made after closing to ensure the buyer receives the company with a normal, pre-agreed amount of cash to run day-to-day operations.

Representations and Warranties

Welcome to what is often the longest, most intensely negotiated part of the entire SPA. "Reps and warranties" are a series of promises the seller makes about the business. They are definitive, factual statements covering nearly every facet of the company's past and present.

Key Takeaway: Reps and warranties act as a detailed disclosure from the seller. If one of these promises turns out to be false after the deal closes, the buyer usually has a legal right to seek compensation for the financial damage caused by that broken promise.

Sellers will be asked to make official statements on things like:

- Financial Statements: A promise that the books are accurate.

- Taxes: A confirmation that all tax returns have been filed correctly and taxes paid.

- Legal Compliance: A statement that the business has operated by the book in jurisdictions like Ontario and New York.

- Contracts: An assurance that all important contracts are valid and in good standing.

- Intellectual Property: A warranty that the company owns its IP and isn’t infringing on anyone else’s.

Covenants

If reps and warranties are about the past, covenants are about the future—specifically, the period between signing the agreement and the official closing day. Covenants are the "rules of the road" both sides agree to follow.

- Pre-Closing Covenants: These are the seller's promises on how they’ll run the business before the deal is final (e.g., no new debt or major asset sales without buyer approval).

- Post-Closing Covenants: These obligations kick in after the deal is done. The most common are non-compete clauses and non-solicitation clauses, which stop the seller from poaching employees or clients.

The covenants in an SPA often have to align with existing founder agreements, a topic we cover in our guide on the 12 clauses that prevent founder wars in shareholders' agreements.

Conditions Precedent

Think of this section as the deal's final checklist. It lists everything that must happen before the buyer is legally required to close the deal. If a condition isn’t met, the buyer can typically walk away without penalty. Common conditions include securing key third-party approvals, government sign-offs, and confirming that no "material adverse change" has occurred to the business since the SPA was signed. This clause is a critical escape hatch.

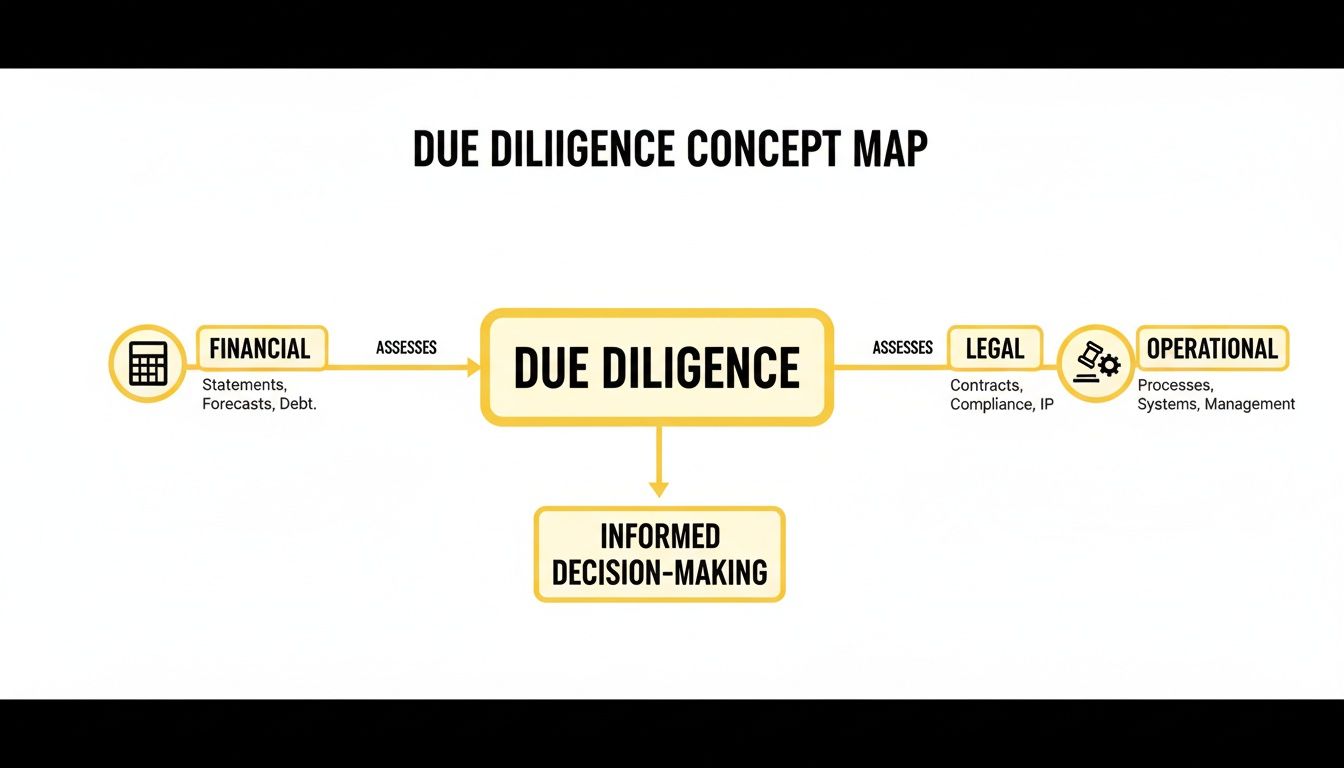

Navigating the Due Diligence Process

Due diligence is the ultimate "look under the hood" phase, where a buyer gets to verify that the business they’re about to acquire is everything the seller has promised. It’s an exhaustive investigation to uncover hidden risks, liabilities, or operational skeletons before the contract is signed. This is the stage where all the promises made in the "reps and warranties" section are put to the test.

Key Areas of Investigation

Due diligence is a multi-faceted review, usually broken down into three core areas that create a complete picture of the company's true value and risks.

- Financial Due Diligence: A forensic accounting exercise where auditors pore over financial statements, tax filings, and cash flow records to confirm the numbers are accurate and sustainable.

- Legal Due Diligence: Legal experts comb through corporate records, contracts, IP filings, permits, and any litigation to check for a clean title and ensure compliance with regulations in jurisdictions like New York or Ontario.

- Operational Due Diligence: This assesses the strength of the management team, customer and supplier relationships, and the integrity of its technology and internal processes.

For companies with operations in both the U.S. and Canada, legal and financial diligence becomes even more complex. You’re not just looking at one set of rules, but two.

Cross-Border Due Diligence Checklist for US-Canada Deals

| Diligence Area | Key Items for US (New York) | Key Items for Canada (Ontario) |

|---|---|---|

| Corporate Structure | Certificate of Incorporation, Bylaws, NY Good Standing Certificates, Foreign Qualifications. | Articles of Incorporation, Bylaws, Ontario Corporate Profile Report, Extra-Provincial Registrations. |

| Employment & Labor | Compliance with FLSA, NYS Labor Law, at-will employment agreements, benefits (ERISA). | Compliance with Employment Standards Act (ESA), common law notice periods, WSIB filings. |

| Taxation | Federal (IRS) and NYS tax returns, sales tax compliance, nexus evaluation. | Federal (CRA) and Ontario tax returns, HST/GST filings, residency determinations. |

| Regulatory & IP | US securities law compliance, industry-specific permits (e.g., environmental), USPTO filings. | Canadian securities law compliance, provincial permits, CIPO filings for trademarks/patents. |

This checklist is just a starting point, but it illustrates how diligence requirements multiply when a business straddles the border. Each item can uncover issues that need to be addressed before a deal can close.

Preparing a Data Room for Sellers

As a seller, a meticulously organized data room does more than just facilitate the buyer's review—it sends a powerful message that you run a tight ship and have nothing to hide.

Best Practice: Structure your data room with a logical, intuitive folder system (e.g., "Corporate Records," "Financials," "Material Contracts"). Anticipate buyer requests and upload all relevant documents proactively. This shows transparency and keeps the momentum going.

Understanding compliance nuances is a huge part of this. For example, knowing your obligations ahead of time is critical. You can learn more by reviewing our article on federal registration requirements in the United States. Taking the time to prepare thoroughly is one of the most effective things a seller can do to ensure a smooth closing.

Reps, Warranties, and Indemnification: Where the Real Risk Lies

If representations and warranties are the seller’s promises, then indemnification gives those promises real teeth. It answers the question: "What happens if a promise turns out to be false?" Simply put, indemnification is the mechanism that protects a buyer from financial losses that arise after the deal has closed. It is a custom-built insurance policy for the buyer, underwritten by the seller.

Breaking Down the Indemnification Clause

Negotiating indemnification is about setting clear boundaries on the seller’s post-closing responsibility. The back-and-forth usually boils down to three key components:

- Survival Period: This is the expiration date on the reps and warranties, setting the time limit for the buyer to bring a claim. A typical survival period is 12 to 24 months, though certain "fundamental" reps may survive indefinitely.

- Basket (Deductible): This sets a damage threshold that must be reached before the seller has to pay, stopping buyers from nitpicking over minor issues.

- Cap (Liability Limit): This sets the ceiling on the seller's total financial exposure for indemnification claims, often a percentage of the purchase price.

The diligence work—across financial, legal, and operational areas—directly informs how you should structure the reps, warranties, and indemnification clauses to properly allocate risk.

Why Indemnification Is So Important in Cross-Border Deals

The stakes get even higher when a deal crosses international borders, such as a transaction between companies in Ontario and New York. You're suddenly dealing with different legal standards, conflicting tax rules, and separate regulatory bodies like the SEC and OSC. This creates more opportunities for costly breaches.

A well-drafted indemnification clause provides a clear, contractually defined roadmap for resolving disputes, which is more efficient than navigating two court systems. This transparency is also important for defense against potential white-collar allegations, a core focus at Mayo Law. You can see the importance of transactional data by reviewing historical information from regulatory bodies like FINRA.

Indemnification isn't about punishing the seller. It’s about correctly allocating risk. It’s a mechanism to ensure the buyer gets the company they paid for and provides a clear, predictable remedy if reality doesn't match the promises made.

Navigating Cross-Border Complexities in US-Canada Deals

When a stock deal crosses the U.S.-Canada border—involving operations in both Ontario and New York—things get complicated fast. Getting these deals right is a core focus for our team at Mayo Law, and it requires a practical understanding of two different sets of rules. A cross-border SPA must be carefully engineered to align different legal traditions, regulatory bodies, and tax systems.

Conflicting Securities Laws

One of the first hurdles is navigating securities regulations. In the U.S., the Securities and Exchange Commission (SEC) calls the shots. In Ontario, you answer to the Ontario Securities Commission (OSC). They don’t always play by the same rulebook.

- Mismatched Exemptions: Both jurisdictions offer exemptions for private stock sales, but the requirements rarely align. An exemption that works for your New York investors might not be valid for your Toronto shareholders.

- Varying Disclosure Standards: The information you’re legally required to give buyers can differ significantly. What the SEC considers adequate disclosure might fall short of OSC standards, or vice-versa.

Key Consideration: In a cross-border deal, you must satisfy the securities laws of every single jurisdiction where a buyer or seller is located. One misstep can unravel the entire agreement.

Tax Implications on Both Sides of the Border

Taxes are where many cross-border deals create value or go sideways. A move that saves money in one country can trigger a massive tax liability in the other.

- Withholding Taxes: When a U.S. buyer pays a Canadian seller, the buyer may be required to withhold a portion of the payment for the government. The Canada-U.S. Tax Treaty can often reduce these taxes, but you must proactively claim those benefits in the SPA.

- Surplus Stripping Rules: This is a major trap for Americans buying Canadian companies. Canada has complex anti-avoidance rules—like Section 84.1 of the Income Tax Act—that an unsuspecting U.S. buyer can inadvertently trigger, creating a huge tax problem for the Canadian seller.

- Corporate Residency: The acquisition structure can affect the tax residency of the target company, which determines which country has the primary right to tax its worldwide income.

Choosing the Governing Law and Dispute Resolution

Your SPA needs a clear answer for what happens if something goes wrong. The agreement must state which jurisdiction’s laws will govern the contract—Ontario or New York? This choice dictates everything. Just as important is deciding where to resolve disputes. For many international deals, private arbitration is preferred as it is often neutral, confidential, and faster. Our article on the framework for arbitration in Canada is a great resource.

Closing the Deal and Handling Post-Closing Matters

The closing is when the SPA is executed, but it also kicks off a new set of crucial responsibilities. At closing, the buyer wires the purchase price, and the seller delivers signed documents transferring ownership. While it feels final, your duties under the SPA are just getting started.

The Post-Closing Checklist

The SPA is a living document and will contain tasks that must be handled weeks or months after closing.

- Purchase Price Adjustments: The price on closing day is rarely final. Most agreements include a working capital adjustment to confirm the business was handed over with the exact level of operating cash promised.

- Indemnification Claims: If the seller breached a warranty, the buyer has a specific window to make a claim for damages. The SPA dictates the process for notification and dispute resolution.

- Earn-Out Calculations: If the deal includes an earn-out, the post-closing period is when the acquired company’s performance is tracked against targets to determine if and how much additional compensation the seller has earned.

Managing Ongoing Responsibilities

Beyond financial mechanics, both sides have other duties. A seller might be required to help with the transition, while the buyer has the major task of integrating the new company.

Properly navigating the post-closing period is what separates a good deal on paper from a successful one in reality. Having experienced counsel manage this final stage ensures every contractual obligation is met and the business transition goes smoothly.

These final steps are fundamental to maintaining a clean corporate structure. For a deeper dive, you can explore our ultimate guide to Ontario business structures. Effectively managing these matters solidifies the deal's value and sets the company up for success.

Build Your Business on Solid Legal Ground

Mayo Law advises startups and SMEs in Ontario and New York. Contact Mayo Law to discuss your needs.

LEGAL DISCLAIMER: The information provided in this article is for general informational and educational purposes only and does not constitute legal advice. Reading this article, visiting mayo.law, or contacting Mayo Law does not create an attorney-client relationship. The content of this article should not be relied upon as a substitute for professional legal counsel tailored to your specific circumstances. Legal outcomes depend on the particular facts and circumstances of each individual case, and no attorney can guarantee a specific result. Laws, regulations, and legal procedures are subject to change and may vary by jurisdiction. If you require legal assistance, you should consult with a qualified attorney licensed to practice in the relevant jurisdiction. Mayo Law expressly disclaims any and all liability with respect to actions taken or not taken based on the contents of this article.

Powered by Outrank