Published: June 27, 2026

Updated: June 27, 2026

Read time: 11 minutes

If you’re a Canadian founder or investor looking at the U.S. market, you’re probably weighing a familiar mix of ambition and risk. You may have a franchise opportunity in Florida, a consulting business ready for a New York launch, or a U.S. acquisition that looks strong on paper but raises one blunt question. Will you qualify for an E-2?

At Mayo Law, we help entrepreneurs in Toronto, the GTA, and across Canada through this process, with experience licensed in both Ontario and New York on a matter that often spans both sides of the border. The hard part usually is separating usable rules from bad assumptions that can cost time, money, and momentum.

This guide gives you a practical breakdown of the visa E2 requirements, with a close eye on issues that come up often for Canadian applicants.

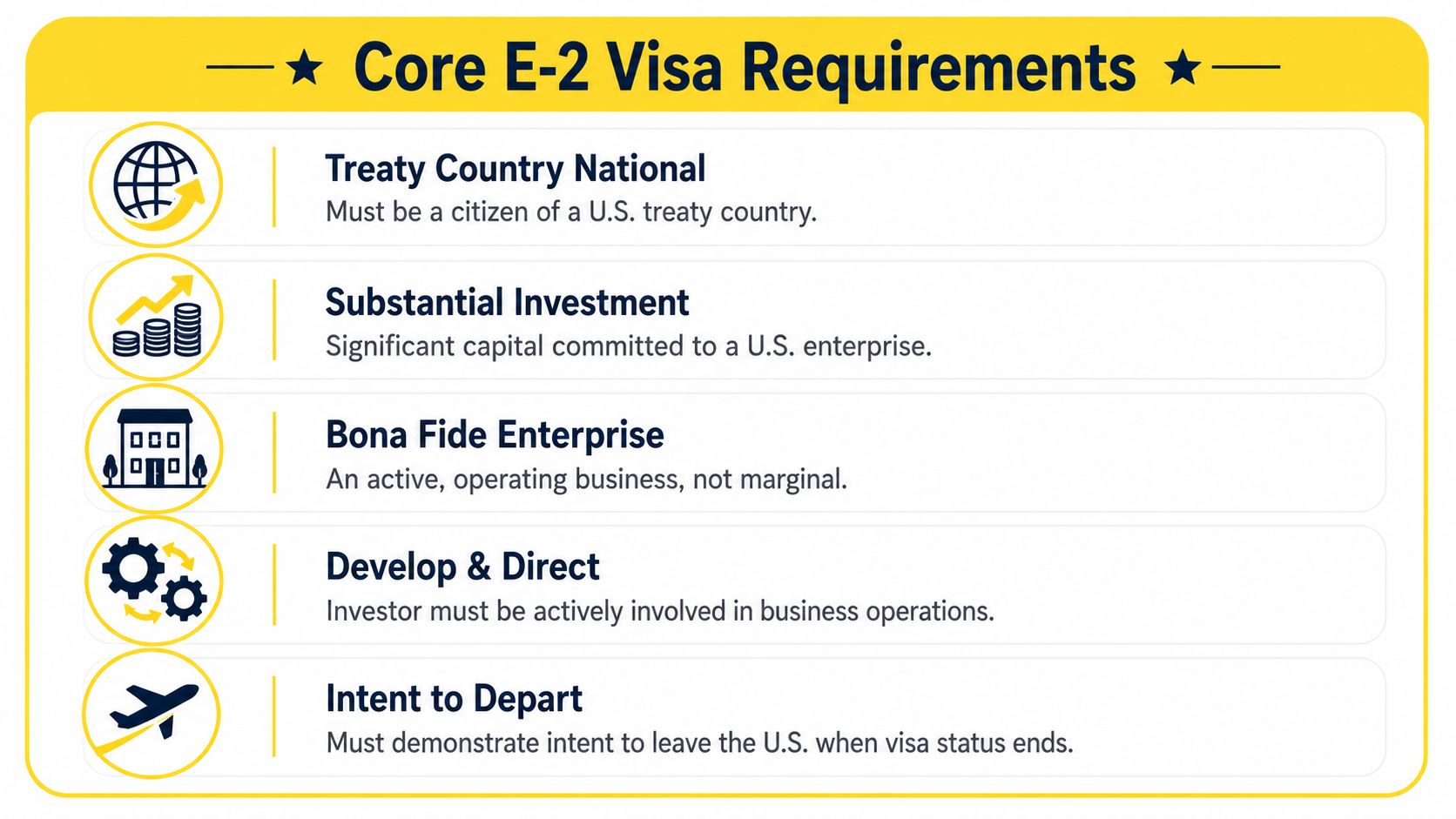

What Are the Core E-2 Visa Requirements?

The E-2 visa is a U.S. nonimmigrant visa for treaty-country nationals who invest a substantial amount of capital in a real U.S. business they will develop and direct. It is one of the more predictable investor visa options for qualified applicants, with 54,364 visas issued globally in FY 2024 and an approximate 90.1% approval rate at U.S. consulates according to E-2 visa statistics.

| Requirement Pillar | What It Means |

|---|---|

| Treaty Nationality | You must hold the nationality of a country with the required U.S. treaty. |

| Substantial Investment | The investment must be substantial relative to the business cost. |

| Real and Operating Enterprise | The business must be active, for-profit, and not merely speculative or idle. |

| Control of the Enterprise | You must own at least 50% or otherwise control and direct the business. |

| Intent to Depart | You must intend to leave the U.S. when E-2 status ends. |

A few practical points matter from the start. The E-2 has no annual numerical cap, unlike some U.S. work visa categories. That helps. It doesn't make the filing casual.

What decides many cases is document quality. The strongest applications prove each pillar with a clean story, consistent records, and a business model that makes practical sense.

Practical rule: Consular officers don't approve effort. They approve evidence.

The Treaty Nationality Requirement

A Canadian founder can have the money ready, the business plan polished, and the U.S. entity formed. If the nationality piece is wrong, the E-2 case still fails.

The rule has two parts. First, the investor must hold the nationality of a treaty country. Second, the U.S. business must be at least 50% owned by people or entities with that same treaty nationality. For many Canadians, the first part is easy. The second part is where cases get misread, especially in startups, holding-company structures, and businesses with outside investors.

What is a treaty country for the E-2 visa?

A treaty country is a country that has the required qualifying treaty relationship with the United States for E-2 purposes. Canadian citizens qualify on that front. The harder question is whether the business itself qualifies as a Canadian treaty enterprise under the ownership rules.

That distinction matters. A Canadian passport does not cure a cap table that is no longer majority Canadian.

Where Canadians get caught

I see the same problem repeatedly with cross-border founders. They assume nationality is personal only. Consular officers examine the company too.

Problems usually show up in four situations:

- Mixed-owner companies: The applicant is Canadian, but too much equity sits with non-Canadian or non-treaty owners.

- Startup financing rounds: The company qualified when it was formed, then a seed round changed the ownership percentage.

- Dual nationality cases: The application has to be presented under the nationality that supports the treaty case, and the documents need to match that approach.

- Parent-subsidiary structures: The U.S. operating company may be owned by a Canadian corporation, which is then owned by several individuals. Officers often want the ownership traced all the way up the chain.

Digital and remote-first businesses run into this more often than traditional small businesses. The company may look simple on the surface, but SAFEs, convertible notes, nominee arrangements, and option pools can make nationality analysis harder than founders expect. For Canadian applicants, this is one of the places where U.S. immigration law and corporate structuring need to be reviewed together, not one after the other.

A common example is a Canadian entrepreneur who owns 40% of a U.S. tech company, while the remaining 60% is split among U.S. and foreign investors. That founder may still control operations day to day. The business may still fail the treaty nationality test because the enterprise is not majority owned by the treaty nationality required for the E-2 filing.

Officers look at the passport and the ownership chart. Both have to work.

Practical review before you spend money

Check the structure before signing a lease, wiring investment funds, or closing on a purchase. Fixing nationality problems after money is committed is harder and more expensive.

Focus on these questions:

- Who owns the U.S. entity today: Officers assess the current structure, not the version you hope to implement later.

- What happens after the next financing event: A pending round can undercut eligibility if it drops treaty ownership below the threshold.

- Whether control rights match the equity story: Titles and side understandings do not replace clear documentary ownership.

- Whether the ownership trail is provable: Share registers, shareholder agreements, corporate records, and subscription documents need to tell one consistent story.

For Canadian investors, early structuring decisions often decide whether the case stays straightforward or becomes an avoidable legal cleanup exercise.

Defining a Substantial Investment

This is the part many individuals ask about first, and often in the wrong way. They ask, "What's the minimum?" U.S. law doesn't give you a fixed minimum.

Instead, the legal standard is a substantial amount of capital judged through a proportionality test, which compares your investment to the cost of buying or starting the business. In practice, E-2 investment guidance notes that service-based startups typically need $80,000 to $100,000, while restaurants or franchises often require $150,000 or more.

For a deeper discussion of practical thresholds, see this guide on the E-2 visa minimum investment amount.

How much money do you need for an E-2 visa?

There isn't a fixed statutory minimum. The key question is whether the amount is substantial relative to the total business cost. Smaller businesses usually require a higher percentage commitment, while larger businesses may qualify with a lower percentage if the total invested is still clearly substantial.

What counts, and what doesn't

A qualifying investment usually looks like money already committed to the business. That may include a signed lease, equipment purchases, inventory, professional setup costs, or funds placed in a proper transaction structure tied to the business launch or acquisition.

A non-qualifying approach is common. The investor keeps funds in a personal or business bank account and assumes the account balance proves readiness. It doesn't.

Here is the cleaner way to approach it:

| Approach | Likely E-2 view |

|---|---|

| Cash sitting untouched in an account | Weak, because it may not be committed |

| Lease signed and deposits paid | Stronger evidence of commitment |

| Equipment and startup costs already paid | Stronger evidence of active investment |

| Passive real estate purchase | Usually not qualifying by itself |

A practical comparison

Consider two Canadian applicants.

The first buys a small U.S. consulting business, signs the office lease, pays for software, furniture, and payroll setup, and closes on the asset purchase subject to immigration timing. That file usually tells a coherent story.

The second buys a condo in the U.S. and says they may manage short-term rentals. That is usually a passive investment problem, not an E-2 business.

Key judgment: The money must be doing real business work, not waiting for permission to matter.

Substantiality is never just about amount. It is also about whether the spending matches the business model. A light-capital consulting practice that claims to need a very large sum can raise credibility issues. A restaurant filing with too little committed capital can raise a different problem. Both fail for the same reason. The numbers don't fit the business.

Ownership, Control, and the Business Plan

The E-2 isn't a visa for passive investors. You need to show that you will develop and direct the enterprise. That usually means owning at least half the business or having real operational control through your role.

A qualifying business also has to be real, active, and for profit. Passive investments, including simple real estate holdings without active business operations, don't qualify under the standard described in this summary of E-2 ownership and active enterprise rules.

A well-prepared E-2 visa business plan is often the document that holds the whole file together.

Can I buy a business for an E-2 visa?

Yes. You can start a new U.S. business or buy an existing one. Either path can work if the enterprise is real and operating, the investment is substantial, and you will actively control and direct the company rather than remain a passive owner.

What control looks like in practice

Control isn't a slogan. It needs to show up in the documents.

Good signs include:

- Ownership rights: You hold at least 50% of the entity, or the governance documents clearly give you operational control.

- Decision-making authority: You can hire, sign contracts, manage budgets, and direct strategy.

- Day-to-day role: Your role fits an executive, managerial, or hands-on founder function.

Weak signs include being called "president" while someone else controls banking, staffing, and contracts.

Why the business plan matters so much

For many Canadian applicants, the business plan is where the case becomes persuasive or falls flat. A generic template usually hurts more than it helps. Consular officers want to see that the plan fits your actual business, your actual market entry, and your actual budget.

The strongest plans usually cover:

- Services or products: What the company will sell and to whom

- Startup spending: How the invested funds are being used

- Operations: Location, staffing, vendors, timing, and launch steps

- Financial projections: Credible assumptions, not inflated optimism

- Hiring plan: Especially important where marginality could become an issue

Mayo Law works with founders, investors, and SMEs across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, so clients with U.S. ties coordinate their legal work in one place rather than juggling two firms.

The non-marginal business requirement

A business can't exist only to support you and your family. It must show present or future economic value beyond that.

For a Canadian owner opening a U.S. design studio, that may mean showing a credible hiring path for U.S. staff. For a retail acquisition, it may mean preserving and expanding local operations. For a solo online business with no U.S. staffing plan, trouble often arises in this situation.

Proving a Lawful Source and Path of Funds

A file can look strong until the officer follows the money.

For E-2 purposes, the question is not only whether the applicant has enough capital. The record must show that the funds were obtained lawfully, came under the investor's control, and were committed to the U.S. business. If any link in that chain is weak, the case can stall fast. I see this often with Canadian applicants who have perfectly legitimate funds but poor paper trails, especially where money moved between personal accounts, holding companies, spouses, or parents before reaching the U.S. entity.

The standard is practical. An officer should be able to trace the funds from origin to investment without guessing. Funds parked in an account with no commitment to the business usually do not help much. Funds already spent on the lease, equipment, inventory, franchise fee, acquisition deposit, or other startup costs usually carry more weight, provided the documentation is clean.

Documents that usually matter

The exact package depends on how the money was generated, but these records often do the heavy lifting:

- Savings from employment or business income: tax returns, T4s or business financials, payroll records, bank statements showing accumulation over time

- Sale of property: agreement of purchase and sale, closing documents, proof of net proceeds, deposit and wire records

- Gifted funds: gift letter or affidavit, donor identification, evidence showing how the donor lawfully obtained the money, transfer records into the applicant's account

- Loan proceeds: signed loan agreement, security documents, proof of disbursement, and proof that the applicant remains personally responsible where required

- Company distributions or shareholder withdrawals: corporate records, resolutions, accountant letters, and statements showing the transfer from the company to the investor

Traceability is the point.

A large incoming transfer with no supporting history creates a credibility problem, even if the money itself is legitimate.

A Canadian example

A strong case might involve an entrepreneur in Ontario who sells a condo, receives the net proceeds in a Canadian account, transfers the funds to a U.S. business account, and then uses them for a commercial lease, equipment purchases, and an acquisition deposit. Each movement is supported by statements, wire confirmations, and closing documents. The officer does not need to infer anything.

A weaker file usually has too many unexplained steps. Money arrives in pieces. Some of it passes through a relative's account. Some comes from an operating company with no shareholder resolution. Then a lump sum appears in the U.S. entity shortly before filing. That pattern invites questions that are hard to answer after the fact.

Canadian applicants run into an extra issue here. Their records are often split across Canadian banks, Canadian corporate entities, and a newly formed U.S. company. That structure can work well, but only if the movement of funds is documented with precision from both sides of the border.

Funding structures that need extra care

Family money is common. So are mixed funding models involving a gift, a personal line of credit, retained earnings from a Canadian corporation, or proceeds from a refinance. These cases are approvable, but they need tighter documentation and better legal framing than a simple savings case.

Two patterns deserve particular caution:

- Loans secured by the assets of the U.S. business: these can create E-2 problems because the investor may not be putting personal capital at risk in the required way

- Layered family transfers: a parent gives money to one relative, who transfers it to another, who then funds the business. Lawful source becomes much harder to prove if the donor's records are thin or the reason for each transfer is unclear

This issue matters even more for digital and service businesses. If the enterprise has fewer visible startup costs, officers often look more closely at whether the capital was genuinely committed and whether the funding story is coherent. That is one reason Canadian founders in consulting, software, marketing, and other low-overhead sectors get pulled into the marginality trap later if they do not build the file carefully at the start.

The best approach is simple. Build the source-and-path record before filing, not after a request for more evidence or a consular interview exposes the gaps. In cross-border cases, that usually means collecting Canadian tax records, sale documents, corporate records, gift evidence, and bank statements early, then matching them to each transfer into the U.S. business with no missing steps.

Common Pitfalls and E-2 Visa Denial Reasons

Many applicants still think the main risk is investing too little. That's only part of the picture. Some denials happen because the business model itself isn't presented in a way that meets current scrutiny.

One issue now matters far more for online businesses. The digital marginality trap has become a real problem. Following 2024 policy memos, denial rates for digital-only businesses rose by 35% in 2025, and officers increasingly expected a 5-year employee projection with concrete U.S. hiring milestones.

If you're assessing business models, this guide to businesses that fit E-2 approval patterns is a useful starting point.

Why digital businesses get challenged

A Canadian founder may have strong revenue, a polished website, and real clients, but still face questions if the U.S. operation looks too remote or too passive. Officers want to see a U.S. enterprise, not just foreign income routed through a U.S. entity.

Warning signs include:

- No U.S. hiring plan: Revenue alone may not solve marginality.

- No physical operating footprint: That can undermine the "real and operating" argument.

- Generic projections: A spreadsheet without operational detail rarely carries enough weight.

Other mistakes that cause trouble

A weak E-2 file often looks complete from the applicant's side. The issue is that the evidence doesn't answer the right legal questions.

Common problems include:

- Underfunding for the industry: The amount doesn't fit the business type.

- Passive structure: The investor doesn't direct the enterprise.

- Thin source-of-funds evidence: The money is there, but the history isn't.

- Weak intent to depart evidence: Applicants forget that E-2 is still a nonimmigrant classification.

For Canadian applicants, the practical lesson is simple. A modern E-2 case has to prove more than enthusiasm, even where the business is genuine.

Frequently Asked Questions

How long is an E-2 visa valid?

For Canadian applicants, the visa foil is often issued for a relatively long period, but the practical question is not just the sticker in the passport. The primary issue is whether the business will still support renewals and re-entry two or three years later.

E-2 status can continue as long as the enterprise remains real, operating, and consistent with the original case. Renewals are never automatic. A business that stalled, shifted into passive income, or never met its hiring plan can create problems at the next application or at the border.

How much does an E-2 visa application cost?

Government filing fees are only one part of the budget. Clients often focus on the consular fee and underestimate the cost of setting up the company, documenting the investment, preparing a credible business plan, and cleaning up source-of-funds records if the money came through multiple Canadian accounts or corporate entities.

That budgeting mistake shows up later. It can leave the business underfunded at the exact point when the case needs to show real operational commitment.

Can my spouse and children come with me?

Yes, in many cases a spouse and qualifying children can accompany the principal E-2 investor.

The legal eligibility is usually straightforward. The planning is not. For Canadian families, timing matters. School calendars, housing, cross-border tax advice, and the spouse's work plans should be addressed before filing, not after visa issuance. I often see families treat dependants as an administrative detail, then run into avoidable stress once the business launch starts competing with the move itself.

How long does processing take in Canada?

Processing times vary by post, interview availability, and the quality of the submission. A well-prepared package can still face delays if the consulate has limited appointments or asks follow-up questions.

Canadian applicants should avoid signing a commercial lease, hiring staff, or committing to inventory on a timeline that assumes a fast approval. Build in slack. The safer approach is to line up the business so it is ready to launch, but not so committed that a short consular delay turns into a financial problem.

Is E-2 better than EB-5?

They solve different problems. E-2 is usually the better fit for a Canadian entrepreneur who wants to direct and grow an active U.S. business now. EB-5 may fit a different investor profile, especially where long-term immigration strategy matters more than day-to-day operating control.

A side-by-side comparison of E-2 vs. EB-5 investor visa options can help frame that decision. In practice, I tell clients to start with the business model, the source of funds, and the family's long-term plans. The right answer often becomes clearer once those pieces are on the table.

Conclusion

If you're a Canadian investor looking south, the E-2 can be a practical route into the U.S. market. It is detailed, but it isn't mysterious. The strongest cases line up the ownership structure, investment, business plan, and money trail before the application is filed. That preparation is what usually separates a workable E-2 strategy from an expensive detour.

How Mayo Law Can Help

Cross-border E-2 matters often involve more than immigration forms. They also involve company setup, ownership structuring, document coordination, and a filing strategy that works on both sides of the border. To discuss your matter, visit Mayo Law's E-2 visa application page.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

Canadian founders usually do best when they look at the E-2 in the broader context of U.S. expansion. A visa strategy that works for a restaurant purchase in Buffalo may be a poor fit for a Toronto software company selling into the U.S. market, especially where ownership, funding, and marginality concerns overlap.

Related reading:

If your case involves a Canadian holding company, mixed personal and corporate funding, or a digital business that needs a stronger marginality story, those topics often connect directly to the E-2 analysis.