An unexpected subpoena lands on your desk. An investigator asks for an interview. Your finance team mentions a regulator’s inquiry that seems broader than a routine request. In that moment, most executives don’t need drama. They need a clear process.

At Mayo Law, our attorneys handle cross-border matters involving New York and Ontario, including white-collar crimes defense for business owners, founders, officers, and professionals. If your company operates across the border, a government inquiry may involve more than one agency, more than one legal standard, and more than one serious mistake to avoid.

White-collar allegations usually involve claims of deceit for financial gain. That can include fraud, tax issues, money laundering, securities matters, or records that prosecutors say were misleading. The right response is calm, disciplined, and documented. If your business has international exposure, your legal strategy should account for contracts, data flows, and entity structure from the start. That broader business context often matters as much as the allegation itself, especially in cross-border international business operations.

Opening Your Guide to White-Collar Defense

White-collar crimes defense starts with understanding what the government thinks happened, and just as vital, what it can prove. A lot of clients first hear the phrase after a subpoena, a search, a bank inquiry, or an internal complaint. By then, the pressure is already high.

Federal white-collar prosecutions have declined sharply over time. U.S. Attorney offices filed 10,269 white-collar prosecutions in fiscal year 1994 and 4,332 in fiscal year 2024, a drop of more than 58 percent. Projections for fiscal year 2025 indicated 3,862 prosecutions, which would be more than 10 percent below FY 2024, according to TRAC reporting summarized here.

That doesn’t make an investigation less serious. It often means agencies may focus on cases they view as significant, document-heavy, or useful as examples.

Practical rule: Fewer prosecutions don’t mean lower stakes. They may mean more concentrated scrutiny in the matters that do move forward.

What Constitutes a White-Collar Crime

A white-collar crime is generally a non-violent financial offense built around alleged deception, concealment, or breach of trust. The label sounds broad because it is. What matters in practice is the conduct, the records, and the claimed intent behind them.

Common allegations executives face

- Securities fraud involves allegations that investors, lenders, or markets were misled through statements, omissions, or reporting.

- Tax evasion is different from lawful tax avoidance. Avoidance uses legal planning. Evasion involves allegations of deliberate concealment or false reporting.

- Money laundering focuses on transactions the government says were designed to hide the source, ownership, or movement of funds.

- Wire or mail fraud often appears when prosecutors say communications systems or delivery channels were used to advance a deceptive scheme.

A case doesn’t always begin with a dramatic event. It may begin with a whistleblower report, an audit issue, a customer complaint, or transaction patterns that attract attention. A routine request can become more serious if a company answers too quickly, too loosely, or without a record-preservation plan.

Strong compliance and risk management practices may help a business spot issues earlier, separate mistakes from misconduct, and avoid making a difficult situation worse.

White-collar matters often turn on intent. The same spreadsheet can look careless, aggressive, or criminal depending on the surrounding documents and who explains them first.

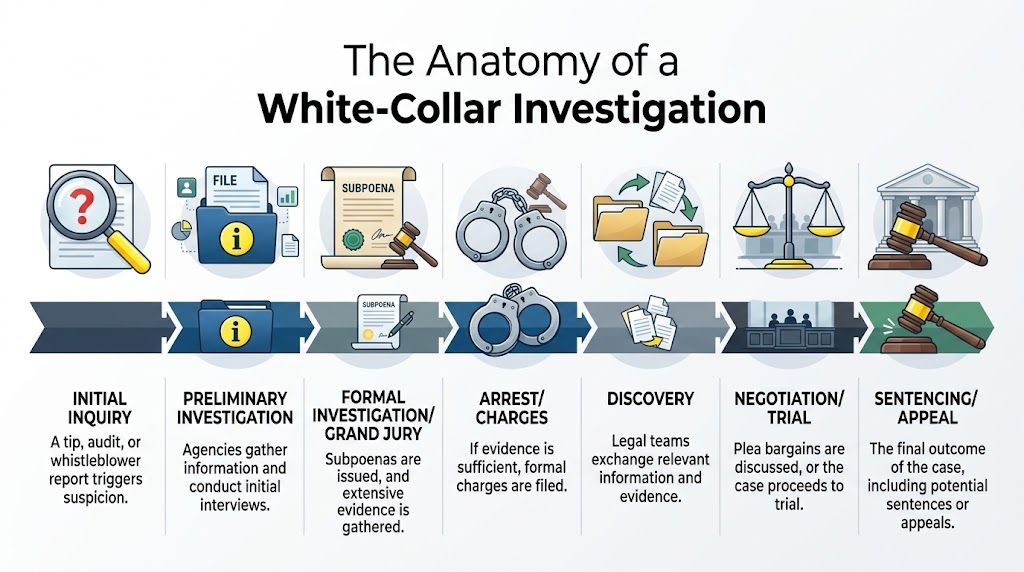

The Anatomy of a White-Collar Investigation

Most investigations unfold in stages, even if the target only sees a piece of the process.

How matters usually develop

-

Initial trigger

A tip, suspicious transaction, audit finding, or internal complaint puts the matter on an agency’s radar. -

Preliminary information gathering

Investigators review public filings, banking material, corporate records, emails, or interview witnesses informally. -

Compulsory process

Under compulsory process, subpoenas, production demands, search warrants, or grand jury activity may appear. -

Charging decision

Prosecutors decide whether the available evidence supports charges, a negotiated resolution, or continued investigation.

Who may be involved

In the United States, executives may see the FBI, IRS-CI, SEC, or a U.S. Attorney’s Office. In Canada, the RCMP, CRA, or provincial securities regulators may be part of the picture. In cross-border matters, those tracks can run at the same time.

That overlap creates practical problems. A document production that seems harmless in one forum may affect privilege, admissions, or sequencing in another. Even settlement discussions can carry strategic consequences if they aren’t coordinated.

Clients with international operations often already know this dynamic from business disputes, investigations, or regulatory reviews involving parallel processes. The same disciplined thinking used in cross-border dispute and arbitration strategy often matters here too, especially when timing and record control are critical.

| Stage | What matters most |

|---|---|

| Early inquiry | Preserve records and centralize communications |

| Formal investigation | Define the facts before answering broadly |

| Charging stage | Test the government’s theory against the documents |

Building a Robust White-Collar Crimes Defense

Every white-collar crimes defense is fact-specific. There isn't a standard script that works across fraud, tax, securities, and money movement allegations. Good defense work starts by narrowing the theory of the case. What exactly is the alleged lie, who supposedly relied on it, and where is the proof of criminal intent?

Defense themes that may matter

A defense may focus on lack of intent. Many business decisions look worse after a loss, a market decline, or a failed transaction. That doesn't automatically make them criminal.

Another common theme is good faith. If a client relied on accountants, counsel, internal controls, or ordinary business assumptions, that may matter a great deal. The same is true when records show confusion, poor controls, or a genuine dispute over valuation or accounting treatment rather than deception.

A third theme is process failure by the government. Search scope, document handling, interview methods, and digital evidence management all matter. In some cases, the defense is strongest when it attacks how the evidence was gathered and interpreted.

Why forensic accounting changes cases

In complex financial matters, forensic accounting is often the center of the defense, not a side issue. Defense experts use transaction tracing and data analysis to test the government's narrative and identify legitimate business explanations for conduct that prosecutors describe as suspicious. According to Branstad Law's discussion of white-collar case complexity, over 90% of federal cases are resolved through pleas influenced by expert rebuttals rather than trials.

That is why early review matters. A forensic accountant may find timing gaps, spreadsheet errors, alternate explanations for transfers, or ordinary related-party activity that was framed too aggressively by investigators.

The government usually tells a story through records. The defense has to tell a more accurate story through the same records.

One practical option in this space is Mayo Law, which advises on cross-border white-collar and compliance matters involving financial records, agency requests, and parallel U.S.-Canada exposure.

Navigating Cross-Border Challenges in NY and Ontario

A domestic defense strategy can break down quickly when the facts touch both sides of the border. That is especially true when tax agencies, securities regulators, or criminal investigators are moving on parallel timelines.

A critical issue in cross-border white-collar crimes defense is that U.S. and Canadian protections don't line up neatly. As noted in this discussion of cross-border defense complexity, a U.S. defense tied to the Fourth Amendment may have no direct equivalent under Canadian Charter protections. The same article notes that clients facing simultaneous IRS and CRA scrutiny need a coordinated strategy that accounts for different evidence rules and prosecutorial standards.

What to do first

- Preserve everything. Don't delete emails, chats, drafts, calendar entries, or accounting files.

- Control internal communications. Limit loose discussion inside the company. Casual speculation creates bad exhibits.

- Route responses through counsel. Different agencies may ask overlapping questions in ways that create risk if answers aren't harmonized.

- Map the entities and transactions. Shared vendors, intercompany payments, and deal documents often become central.

- Review key contracts early. Representations, indemnities, and disclosure clauses in stock purchase agreements and related deal documents may affect both defense posture and business fallout.

What usually doesn't work

Trying to "clear things up" informally rarely helps. Internal fact-gathering without privilege can also create discoverable material. So can partial productions made in haste.

Cross-border cases punish inconsistency. A statement that sounds harmless in New York may create a serious problem in Ontario, or the reverse.

Key Considerations When Under Investigation

Start with restraint. The first hours after learning about an investigation are when people create avoidable problems.

- Consider retaining counsel immediately. Early representation may help protect privilege, manage agency contact, and prevent inconsistent responses.

- Consider preserving all records at once. Missing documents can create obstruction concerns even where the underlying facts are defensible.

- Consider pausing interviews and written explanations until counsel is involved. People often over-explain when they're nervous.

- Consider separating business remediation from defense strategy. Fixing controls may be wise, but it shouldn't happen in a way that creates admissions unnecessarily.

- Consider who inside the company needs to know. Broad disclosure can disrupt operations and generate inaccurate narratives.

Federal enforcement patterns also influence the practical environment. While prosecutions have declined over time, businesses still face major exposure because white-collar crime costs U.S. businesses over $300 billion annually, according to this 2025 industry summary. Prevention and response both matter.

Proactive Compliance and Risk Reduction for Businesses

The strongest white-collar crimes defense often begins long before an investigation. It begins with controls that make misconduct harder, detection faster, and response more disciplined.

For businesses, the internal risk isn't always where leadership expects it. According to these 2025 white-collar crime statistics, approximately 84% of occupational fraud perpetrators showed at least one behavioral red flag before detection, fraud is most common among employees with 1 to 5 years of tenure, and about 52% of occupational fraud perpetrators have a university degree. That combination is a reminder that risk doesn't sit in one department or one stereotype.

Controls worth considering

- Targeted financial controls that separate approval, payment, and reconciliation functions.

- A real whistleblower path that employees trust enough to use.

- Documented escalation rules for unusual transfers, related-party activity, and off-cycle payments.

- Training tied to actual workflows, not generic slide decks.

- Periodic review of compliance policies and reporting channels through Mayo Law's compliance and risk management insights.

Good compliance doesn't just reduce risk. It also creates better evidence when a regulator or prosecutor starts asking questions.

Experienced Defense for Significant Legal Challenges. Early legal counsel may make a meaningful difference, especially in cross-border white-collar matters involving New York and Ontario. To discuss your situation confidentially, schedule a consultation with Mayo Law.

LEGAL DISCLAIMER: The information provided in this article is for general informational and educational purposes only and does not constitute legal advice. Reading this article, visiting mayo.law, or contacting Mayo Law does not create an attorney-client relationship. The content of this article should not be relied upon as a substitute for professional legal counsel tailored to your specific circumstances. Legal outcomes depend on the particular facts and circumstances of each individual case, and no attorney can guarantee a specific result. Laws, regulations, and legal procedures are subject to change and may vary by jurisdiction. If you require legal assistance, you should consult with a qualified attorney licensed to practice in the relevant jurisdiction. Mayo Law expressly disclaims any and all liability with respect to actions taken or not taken based on the contents of this article.

![Yellow decorative banner with a maple leaf and city skyline; title reads 'Employment Immigration Attorney Guide for US-Canada Business'.] ,](https://mayo.law/wp-content/uploads/2026/06/employment-immigration-attorney-business-guide-1024x569.jpg "employment-immigration-attorney-business-guide - Mayo Law")