Published: July 4, 2026 | Updated: July 4, 2026 | Read time: 11 minutes

You’re usually looking at an off take contract when the commercial deal is mostly real, but the financing still isn’t. The site is identified, the technology is chosen, internal approvals are moving, and then the lender asks the question that decides whether the project advances: who is committed to buy the output? At that point, the contract stops being a procurement document and becomes a finance document.

At Mayo Law, we help businesses in New York, Toronto, and across the border manage this kind of agreement with experience licensed in both Ontario and New York on a process that often spans both sides of the border. For cross-border contract planning and deal support, see our international business legal services.

Introduction

What Is an Off Take Contract?

An off take contract is a legally binding agreement between a producer and a buyer under which the buyer commits to purchase a specified amount of future product before production begins. It is used to support construction, expansion, or equipment financing by showing lenders there is real demand and an expected revenue stream, as explained by Investopedia’s discussion of offtake agreements.

In plain English, it works like a high-value pre-order. The producer gets a committed buyer. The buyer gets supply certainty. The lender gets a clearer revenue case than “we expect the market will be there.”

That matters most where capital costs are high and production comes later. Energy, mining, advanced manufacturing, agriculture, and climate technology projects often use these agreements because the project company needs a credible path from construction to cash flow.

How does an offtake contract secure financing?

Lenders underwrite repayment, not optimism. An off take contract helps because it can establish the framework for a long-term sale of all or substantially all of project output and provide the revenue stream that supports financing, as described by Global Trade Funding on project finance offtake agreements.

The parties are simple to identify. One side is the producer. The other is the offtaker, meaning the buyer. The hard part isn’t naming them. The hard part is deciding what exactly is being bought, on what pricing formula, for how long, and with what remedies if things go sideways.

Practical rule: If your lender is reading the contract more closely than your commercial team, the agreement is carrying financing risk, not just sales risk.

A strong contract gives each side a form of certainty, but not the same certainty. Producers want bankable revenue and room to operate. Offtakers want dependable volume, consistent specs, and recourse if output fails. Good drafting recognizes that tension instead of hiding it.

Essential Clauses in Every Off Take Contract

The contract usually succeeds or fails on a handful of clauses. Not because they’re the most interesting, but because they decide who absorbs price shocks, production failures, transport problems, and timing slippage.

In climate tech, this becomes even sharper. Net Zero Insights explains that these agreements can guarantee specific product volumes before production begins and lock in indexed pricing tied to market benchmarks, which is important in sectors where upfront capital can exceed $500M.

Quantity and commitment

Start with volume. Is the buyer taking all output, a minimum amount, or a scheduled amount? Is the commitment absolute, or is it tied to available production?

Parties often discuss “take-or-pay” and “take-and-pay” economics. In practice, the issue is whether the buyer must pay even if it doesn’t physically take delivery. Producers want that protection because lenders like predictable revenue. Buyers resist if forecast demand is uncertain.

A quantity clause should answer:

- Baseline volume: What amount is committed each period?

- Tolerance bands: How much shortfall or overproduction is acceptable?

- Exclusivity: Can the producer sell excess output elsewhere?

- Consequences: What happens if either side misses the volume commitment?

Price and pricing formula

Price disputes are common because parties think they agreed on economics when they only agreed on a concept. “Market price” is not a pricing mechanism. It’s an invitation to fight later.

For cross-border deals, fixed pricing can create currency risk and indexed pricing can create benchmark risk. Sometimes a floor, ceiling, or adjustment formula works better than either extreme.

Indexed pricing can keep a long-term contract commercially alive. It can also create a mismatch if the benchmark doesn’t track the producer’s actual cost base.

If the formula is complex, define the source, timing, fallback mechanism, and who calculates adjustments. If no benchmark is published on a given date, the contract should already say what happens next.

Term and ramp-up

The term needs more thought than “long enough for financing.” Construction delays, commissioning tests, and ramp-up periods often affect when delivery obligations should begin.

Many draft contracts are often too rigid. A well-drafted agreement distinguishes between signing date, effective date, commercial operation date, and delivery start date. If those concepts blur together, one missed milestone can trigger a default that nobody intended.

Delivery and product specifications

Quality terms deserve precision. If you produce minerals, fuel, agricultural commodities, recycled inputs, or other spec-sensitive goods, your dispute risk often sits here.

Use objective standards where possible:

| Issue | Better drafting approach |

|---|---|

| Quality | Reference measurable specifications and testing methods |

| Delivery point | State exact transfer location and risk transfer point |

| Acceptance | Set inspection timing and deemed acceptance rules |

| Rejection | Limit rejection rights to defined non-conformity |

A producer should also look closely at who pays freight, who bears customs risk, and when title transfers in a U.S.-Canada shipment.

What is a force majeure clause?

A force majeure clause allocates risk when extraordinary events prevent performance. It should define the events covered, notice requirements, mitigation duties, and what happens if disruption continues for an extended period.

In cross-border deals, don't leave this generic. Border disruptions, regulatory actions, transport interruptions, grid constraints, and supplier failures may or may not be covered depending on the wording.

Sample language: “If a force majeure event prevents a party from performing a material obligation, that obligation is suspended only for the duration of the event, provided the affected party gives prompt notice and uses commercially reasonable efforts to mitigate the impact.”

Conditions precedent and termination

Conditions precedent are the gates that must open before the contract is fully operative. Financing closing, permits, board approval, and completion testing are common examples.

Termination rights need symmetry, or at least a reasoned asymmetry. One-sided termination for convenience is often a financing problem because it makes projected revenue less reliable. If disputes will be resolved in court or arbitration, the forum choice matters too. A clear forum selection clause analysis can prevent the added cost of litigating jurisdiction before litigating the actual problem.

Navigating U.S.-Canada Cross-Border Considerations

A domestic offtake agreement is hard enough. A U.S.-Canada one adds legal, tax, currency, enforcement, and credit issues that generic templates don't handle well.

The first question is usually governing law. Ontario law may feel natural for a Canadian project company. New York law may feel familiar to a U.S. buyer or lender group. Neither choice is automatically right. What matters is fit with the financing structure, enforcement strategy, and the bargaining strength of the parties.

Creditworthiness is not a side issue

This is the nuance many business teams miss. The offtaker's financial quality can matter as much as the promised volume. ACore notes that most new wind, solar, and clean energy projects require a PPA with a creditworthy offtaker before they can advance development, and a weak offtaker can collapse the financing structure.

That logic applies beyond a classic power project. If a Canadian project relies on a U.S. buyer, lenders will usually want to know whether that buyer can perform over the contract term. A beautifully drafted contract with a weak buyer is often not bankable.

A practical credit review usually asks:

- Who is the actual obligor? Parent, subsidiary, or special-purpose buyer.

- What support exists? Guarantee, letter of credit, security package, reserve account.

- What happens on downgrade or distress? Cure rights and replacement support.

- Can revenue be captured? A lender may ask for account control or related protections. That's where tools such as a deposit control account agreement become relevant.

Governing law, tax, and payment mechanics

Currency and tax terms often produce avoidable friction. If the contract price is in U.S. dollars but project costs are mostly in Canadian dollars, exchange-rate movement can materially change economics even when physical performance is fine.

Tax should be reviewed early, not after the term sheet is agreed. Depending on the structure, cross-border payments can raise withholding or reporting questions. Executives should confirm the current rules with the IRS and the Canada Revenue Agency, then align the contract with the tax advice. If tax allocation language is vague, the parties can end up renegotiating economics after signing.

Fair negotiation is also a financing issue

Hard bargaining isn't the same thing as durable drafting. In sectors with fragmented supply chains or smaller producers, a one-sided process can produce a contract that is technically enforceable but commercially unstable.

A Farm Fit Insights point summarized by Avisen Legal notes that contract negotiations are often imbalanced and should include processes that let producers raise concerns and build trust. That matters in cross-border project finance because investors increasingly examine whether supply commitments are durable in practice, not just aggressive on paper.

Mayo Law works with businesses across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, so clients with U.S. ties coordinate their legal work in one place rather than juggling two firms.

Negotiation Strategies and Red Flags

Most bad offtake agreements don't look bad on signing day. They look workable, efficient, and “close enough.” The trouble appears when the first shipment misses spec, the first delay hits, or the market moves against one side.

If you're the producer, protect the economics that make the project financeable. If you're the buyer, protect the reliability and quality that justify your commitment. Both sides should care about whether the contract will still function when performance is imperfect, because that's the true test.

What are common red flags in an offtake agreement?

Common red flags include vague pricing language, unclear testing methods, one-sided termination rights, broad rejection rights, and force majeure clauses that read well but don't allocate actual operational risks.

Another red flag is a contract negotiated only by procurement and sales teams without finance, tax, and operations pressure-testing the draft. That's how you end up with a signed document that can't survive implementation.

Two short scenarios

A minerals producer agreed to deliver product meeting a stated grade, but the agreement didn't identify the testing method, sampling location, or tie-break procedure. The first cargo was rejected. Both sides had lab reports. Neither side had a contract mechanism to decide which report controlled.

That fight was avoidable. A clause naming the testing standard, sample chain of custody, and independent expert determination would have turned a lawsuit problem into an operations problem.

In another deal, a renewable project company committed future output with a broad force majeure clause but no clear notice standard and no distinction between equipment failure and external events. When production fell short, the producer claimed force majeure. The buyer called it maintenance failure. The dispute quickly became about interpretation rather than recovery.

The best red-flag test is simple. Ask whether an operations manager could follow the clause during a bad week without calling outside counsel first.

Practical negotiation points

Use this list as a deal-room filter:

- Define quality objectively: If quality drives value, build in measurable specs, test timing, and an expert process.

- Limit open-ended exclusivity: Producers should preserve room for excess capacity, substitute products, or additional customers where financing allows.

- Balance termination rights: If only one side can walk away easily, expect financing concerns and future renegotiation pressure.

- Match remedies to breach severity: Immediate termination for every breach often makes the contract less stable, not more.

- Record the business assumptions: If the price formula assumes a benchmark, freight profile, or regulatory treatment, say so clearly.

Template contracts are particularly risky here. A generic purchase template may save drafting time and cost up front, but the mismatch shows up later in dispute spend, project delay, or refinancing trouble. That's why high-value deals often benefit from focused contract negotiation counsel, even when the commercial terms already seem settled.

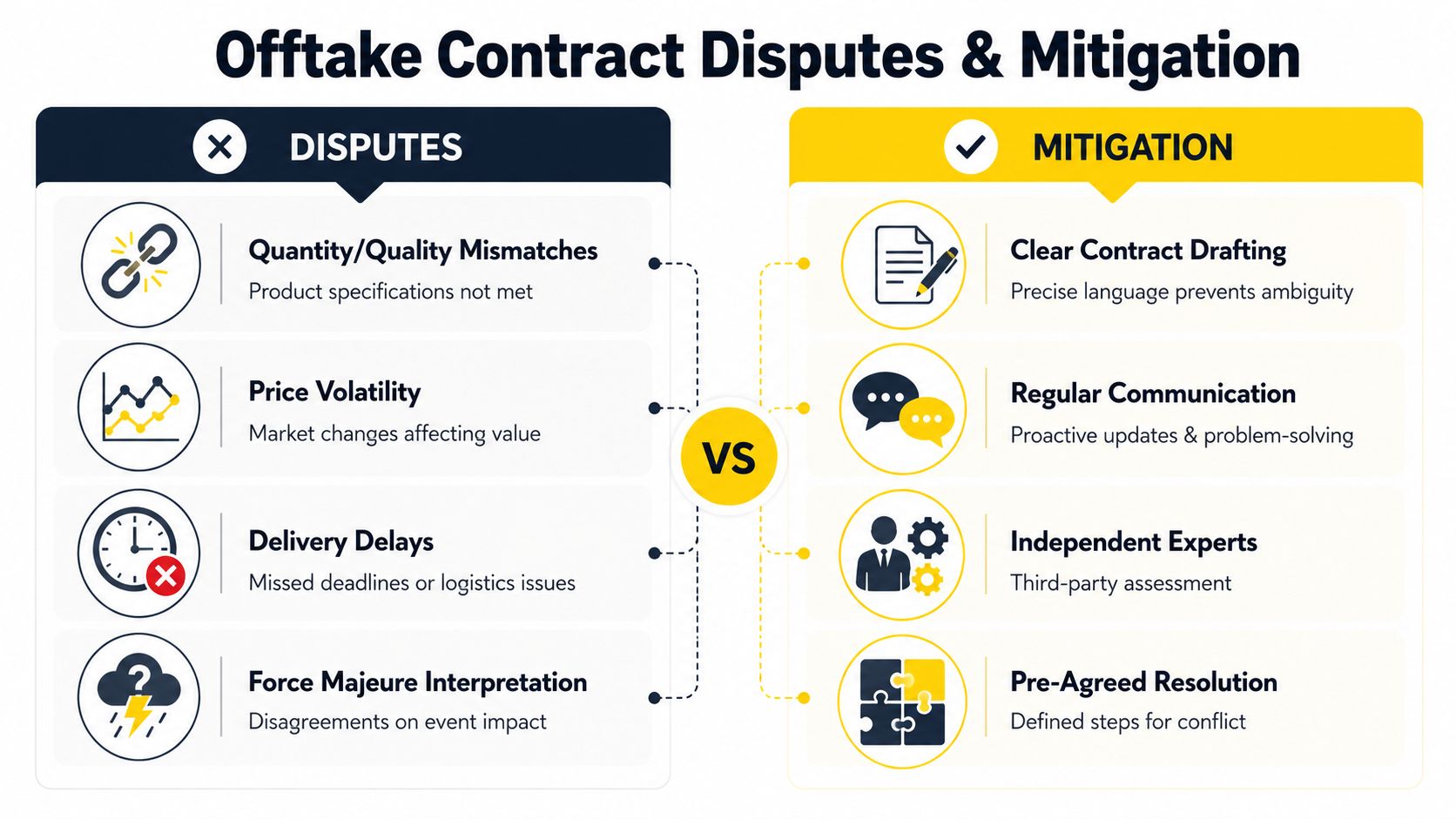

Common Disputes and How to Mitigate Them

The disputes that recur are rarely surprising. Quality, quantity, timing, price adjustment, and excuse clauses generate most of the heat. The practical question isn't whether those issues can arise. It's whether the contract gives the parties a way to contain them.

Where disputes usually start

A producer delivers within the time window, but the buyer says the goods fail spec. A buyer delays payment because benchmark pricing moved sharply and the formula suddenly feels expensive. A project misses output targets and the producer claims disruption outside its control.

These are not unusual failures. They are drafting tests.

How to reduce escalation

Several techniques work well in practice:

- Use independent verification: For quality disputes, appoint a testing expert or laboratory process in advance.

- Create cure periods: Not every shortfall should trigger immediate default or termination.

- Set escalation steps: Operational meeting, senior business review, mediation, then arbitration or court.

- Separate payment disputes from performance disputes: In some deals, undisputed amounts should still be paid on time.

- Write for partial failure: Projects often underperform before they completely fail.

A contract that only describes perfect performance is unfinished.

Dispute resolution also deserves more thought than boilerplate. If the parties expect cross-border enforcement risk, arbitration may be preferable to court litigation. If speed matters and the issues are technical, a staged expert process can preserve the relationship and narrow what reaches counsel. For parties weighing that route, this overview of arbitration in Canada and enforcement is a useful starting point.

Frequently Asked Questions

How much does it cost to draft an off take contract?

There isn't a standard price because the cost depends on complexity, sector, financing needs, and whether the deal is domestic or cross-border. A short-form supply commitment costs less than a finance-driven agreement with guarantees, security support, and tax review. The better way to think about legal cost is against the cost of a failed closing, delayed commissioning, or an avoidable dispute.

How long does it take to negotiate an offtake agreement?

Simple agreements can move relatively quickly. Finance-backed, cross-border agreements often take much longer because business terms, diligence, lender comments, and internal approvals all affect the draft. If the contract is tied to permits, financing, or construction milestones, timing usually depends more on deal coordination than on redlining speed.

Can an off take contract be used for services, or only goods?

An off take contract is mainly used for future output or product supply, not pure services. You can adapt similar commercial ideas to service arrangements, but the classic structure is a commitment to buy produced goods or project output. Power purchase agreements are a familiar example in the energy space.

Do I need a lawyer to draft an off take contract?

For a high-value or project-finance deal, yes. The legal risk isn't only wording. It's whether the document works with financing, tax, operations, remedies, and cross-border enforcement. Templates usually miss the issues that matter most once a problem appears, especially when the parties are in different countries.

What's the difference between an offtake agreement and a PPA?

A PPA, or power purchase agreement, is a specific type of offtake agreement used for power projects. The broader category is the offtake agreement. The narrower category is the PPA. The financing logic is often similar, but the operational terms, regulatory overlay, and performance metrics can differ significantly.

If you're pricing a project, negotiating with a buyer, or trying to satisfy a lender's diligence list, the contract usually needs more than a sales template. Mayo Law advises on cross-border business agreements involving U.S. and Canadian parties, with practical attention to financing risk, enforceability, and execution.

Conclusion

An off take contract matters most when the project is real enough to need money but not yet producing revenue. That's why the strongest agreements do more than promise future sales. They allocate risk in a way lenders, operators, and counterparties can live with. If the buyer's credit is weak or the negotiation process leaves one side boxed in, the contract may look complete and still fail when it matters.

How Mayo Law Can Help

Cross-border offtake work usually breaks down at the point where commercial terms have to satisfy financing, not just sales. A lender will ask whether the buyer can perform, whether the payment structure supports the project model, and whether the contract can be enforced cleanly in the relevant jurisdiction.

Mayo Law advises on U.S.-Canada commercial agreements with that reality in mind. We help clients assess offtaker credit risk, tighten payment and security provisions, choose governing law and dispute mechanisms that fit the transaction, and negotiate terms that are firm enough for bankability without making the deal impossible to close.

The goal is practical. Get an agreement that reflects the actual allocation of risk, works across both legal systems, and stands up when diligence starts.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

Executives structuring cross-border supply and financing arrangements usually need more than a single offtake template. The related topics below address the compliance, workforce mobility, and broader commercial issues that often determine whether a deal closes on bankable terms.