A Canadian company registers to do business in the United States, opens a bank account, starts hiring, and then someone asks a simple question that turns into a compliance problem fast: who are the beneficial owners, and does anything need to be reported?

That question is harder than it looks because a lot of U.S. guidance circulating online is already outdated. Since the U.S. rule shift in March 2025, the old assumption that most small U.S. companies had to file with FinCEN is no longer the practical starting point. At the same time, Canadian companies still need to treat beneficial ownership as an active governance issue, especially when they operate federally or across borders.

At Mayo Law, we help businesses in Toronto, the GTA, and across the border handle compliance issues that don't stay neatly in one jurisdiction. If you're dealing with cross-border reporting risk, internal governance gaps, or timing pressure, our regulatory compliance practice focuses on the kind of practical issues this article addresses.

Introduction

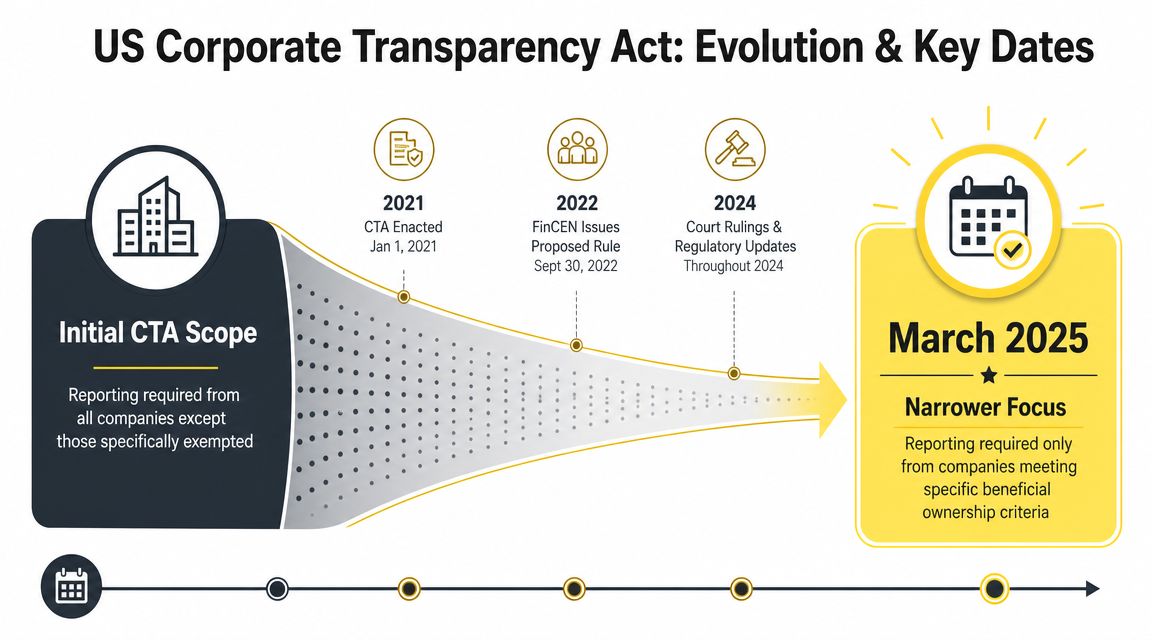

If you just discovered beneficial ownership reporting requirements because your company expanded across the border, you're not behind. Many founders, boards, and in-house teams are working from U.S. guidance that described the original 2024 Corporate Transparency Act rollout, not the narrower rule that applies now.

That matters because the U.S. and Canadian systems don't operate the same way. In the United States, the current issue is often whether a foreign entity registered to do business in the U.S. is still in scope for BOI filing. In Canada, the problem is often maintaining an accurate internal register and proving who really controls the company.

The practical question isn't just who owns 25%. It's who has substantial control, what records support that conclusion, and how quickly your company can update them when governance changes.

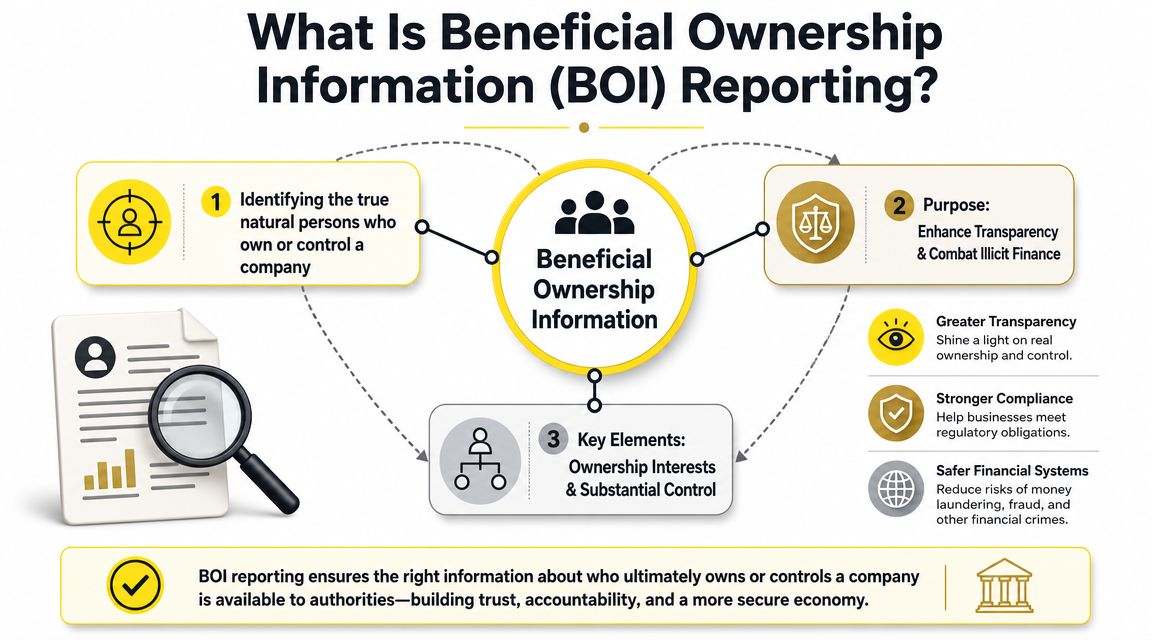

What Is Beneficial Ownership Information Reporting?

Beneficial ownership information reporting is the process of identifying the ultimate individuals behind a company. The point is to get past the entity listed on the corporate record and determine which individuals own it or control it in a meaningful way.

In U.S. practice, that analysis has historically turned on two questions. Who owns at least 25% of the company, and who exercises substantial control. Those tests do different work. Ownership can be measured from the cap table. Control often requires a closer review of shareholder agreements, board rights, appointment powers, veto rights, and layered holding structures.

Who counts as a beneficial owner

A beneficial owner is not always the person with the biggest equity stake. In many files, the harder issue is control. A founder may hold a minority position but retain approval rights over major decisions. A parent company may sit on the share register while one individual controls the chain above it. A senior officer may have enough authority to fall within the control analysis even where ownership is modest or indirect.

That is why I usually start with governance documents before I finalize the ownership chart. Share percentages matter, but they rarely answer the whole question on their own.

What is a reporting company

The reporting company is the entity with the legal duty to report or maintain the required information, depending on the regime. That distinction matters more after the March 2025 U.S. rule change, because older guidance assumed a much wider group of companies had to file. For many businesses, the threshold issue is now whether the entity is still in scope in the United States at all, which for many clients means examining foreign entities registered to do business there.

Canada uses a broader compliance model for many federal corporations. The focus is often less about whether a filing is required and more about whether the company has identified the right individuals and kept its internal records current.

This issue often starts with basic corporate records. If the legal team is tracing ownership from formation documents forward, a practical starting point is this explanation of a certificate of incorporation and what it shows.

US vs Canada A Side-by-Side Comparison

For cross-border businesses, the fastest way to avoid confusion is to stop assuming the two systems mirror each other. They don't. The U.S. has been centered on a filing model tied to FinCEN. Canada's federal approach has focused on maintaining an internal register of individuals with significant control.

| Attribute | United States (FinCEN) | Canada (Federal – CBCA) |

|---|---|---|

| Core model | BOI reporting to FinCEN for entities still in scope | Maintain an internal ISC register |

| Current scope | Mainly certain foreign entities registered to do business in the U.S. | Federally incorporated corporations must maintain ISC information |

| Key ownership threshold | At least 25% ownership, plus substantial control | Significant control can include 25% ownership or votes, and control in fact |

| Main compliance pressure point | Determining whether a foreign entity remains a reporting company and filing on time | Keeping the register accurate as ownership and control change |

| Information focus | Personal identifying details for beneficial owners | Internal corporate records identifying individuals with significant control |

| Practical risk | Outdated CTA guidance causing wrong assumptions about scope | Treating the register as a one-time setup instead of a living record |

The biggest structural difference

The U.S. question has changed. The Canadian question hasn't changed in the same way.

For many companies, the current U.S. issue is narrow and jurisdictional: does this foreign entity, registered in the U.S., still have to file? In Canada, the issue is operational: is your ISC register complete, current, and supportable if examined?

That difference affects internal process. A company with both a Canadian federal corporation and a U.S. registration can easily make the wrong call if the legal team assumes there is one North American beneficial ownership rule. There isn't.

Where businesses get tripped up

A common mistake is to treat ownership reporting as a formation task. It isn't. It sits at the intersection of governance, shareholder arrangements, and ongoing document control.

Another mistake is to look only at legal title. Beneficial ownership analysis often requires you to trace indirect ownership, voting arrangements, or management rights through multiple layers. That becomes even more important when a Canadian company expands into the U.S. market or when a foreign parent registers a U.S. branch or subsidiary structure.

If you're evaluating corporate setup on both sides of the border, this overview of how to start a business in both Canada and the US is a useful companion to the reporting analysis.

The right comparison isn't "Canada versus old U.S. CTA guidance." It's Canada versus the U.S. rule as it exists now.

The US Corporate Transparency Act A Narrower Focus Since 2025

A client forms a Delaware company, assumes the CTA filing still applies, and starts collecting passports from founders and investors. In many cases, that work is now unnecessary. Since FinCEN's March 2025 interim final rule, the U.S. analysis starts with a different question: was the entity formed in the United States, or is it a foreign entity registered to do business there?

For many businesses, that change wiped out the old playbook. Guidance written before March 2025 often assumes that most small U.S. corporations and LLCs must file beneficial ownership information reports. That is no longer the practical starting point. The current rule narrows the reporting obligation to certain foreign entities registered to do business in the U.S., while exempting entities formed in the United States and U.S. persons.

Who still needs to pay attention

The remaining U.S. filing risk is concentrated in cross-border structures.

If a Canadian corporation, UK company, or other non-U.S. entity registers to do business in a U.S. state, that entity may still need a BOI analysis. By contrast, a corporation formed under Delaware law or an LLC formed under New York law generally begins from exemption under the March 2025 rule change. That is a dramatic shift, and it matters because many legal, accounting, and software checklists still reflect the pre-2025 position.

The practical mistake I see is overgeneralization. A business group with one Canadian parent, one extra-provincial registration in Canada, and one U.S. state foreign qualification can look similar on an org chart, but the filing result may be completely different across those entities.

What remains reportable

Where a foreign entity is still in scope, the reporting analysis is familiar in substance even if the pool of reporting companies is much smaller. FinCEN still focuses on the individuals who own or control the entity, including people with substantial control and individuals who meet the ownership threshold, as set out in the FinCEN BOI framework.

That means the hard part has not disappeared. It has become more targeted.

A foreign entity cannot stop at the registered shareholder or parent company name. It still needs to identify the natural persons behind the structure and confirm who has real decision-making authority. In practice, that often requires reviewing shareholder agreements, board appointment rights, veto rights, and constitutional records alongside the cap table. For businesses cleaning up governance records at the same time, this guide on what are bylaws of a company is often relevant because control rights do not always appear in ownership percentages alone.

A better way to assess the U.S. rule now

Use a short sequence.

- Confirm where the entity was formed.

- Confirm whether a foreign entity is registered to do business in the U.S.

- Identify the individuals with ownership or substantial control.

- Collect records that support the conclusion in case the filing position is questioned later.

That approach saves time and reduces false positives. It also avoids the opposite error, which is assuming the CTA disappeared entirely. It did not. It became narrower, and that narrower rule falls most heavily on foreign entities with a U.S. registration footprint.

For cross-border groups, that is the practical takeaway. The U.S. question is no longer, “Does almost every small company have to file?” The better question is, “Which non-U.S. entities in this structure still touch the U.S. registration system in a way that keeps them inside the rule?”

Canada's Federal Regime Maintaining an ISC Register

Canada's federal approach feels less dramatic, but it often creates more day-to-day administrative work. Instead of a FinCEN-style filing model, federally incorporated corporations under the CBCA need to create and maintain an ISC register, meaning a register of individuals with significant control.

The Canadian model is record-based

The practical difference is important. In the U.S. system, the immediate question has often been whether a report must be filed with a government agency. In the Canadian federal system, the question is whether the company has an accurate internal register and can update it when facts change.

That sounds easier. It usually isn't.

A company may know who its direct shareholders are, but still struggle with indirect ownership, family arrangements, unanimous shareholder agreements, or control exercised through rights that don't show up neatly on a cap table. The legal task is less about one electronic filing and more about maintaining a defensible corporate record.

The real burden is keeping it current

Beneficial ownership reporting often poses a challenge for many SMEs. The hard part isn't identifying the original controlling individuals when the company is formed. The hard part is maintaining accuracy after financings, management changes, redemptions, corporate reorganizations, or M&A activity.

Greenberg Traurig's discussion of the U.S. rule captured a point that applies more broadly in practice: the operational burden isn't only identifying the 25% threshold. It's maintaining accuracy as ownership and governance change, especially across restructurings and transactions, as noted in this analysis of beneficial ownership reporting requirements under the CTA.

If your ownership chart changed, your register probably needs review too.

A practical Canadian workflow

For a federally incorporated company, the ISC process usually works better when responsibility is assigned clearly:

- Corporate records lead: One person owns the register and update process.

- Transaction trigger list: Share issuances, transfers, board changes, and reorganizations trigger review.

- Evidence file: Keep the shareholder records, agreements, and identification materials together.

- Board visibility: Directors should know whether the register was reviewed after major changes.

A common scenario is a founder-led business incorporated federally, with family members, a holding company, and a private financing round layered in over time. Another is a Canadian company preparing for U.S. expansion while its Canadian records are still based on an old shareholder structure. In both cases, the issue isn't abstract compliance. It's whether the records reflect reality.

If you're cleaning up foundational records at the same time, this guide on how to incorporate a business in Ontario helps put the governance pieces in order.

Common Exemptions and Key Deadlines

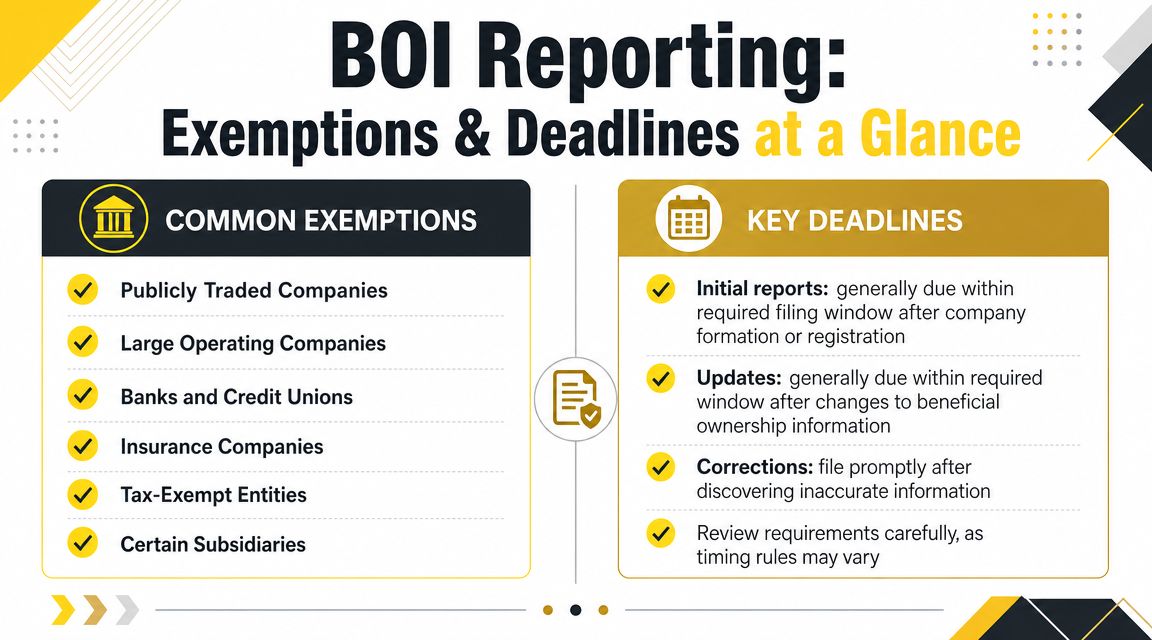

Once the scope question is clear, most clients want two answers. Are we exempt, and if not, when is the deadline?

The exemption analysis differs by jurisdiction and entity type. In both countries, regulated entities and certain other categories may fall outside the core reporting or record-keeping concern, but you shouldn't assume that because your group has a complex structure, it is automatically exempt. The current U.S. issue is narrower and more foreign-entity-focused than before. The Canadian federal issue is usually whether the corporation must maintain its register properly.

U.S. timing rules that still matter

For U.S. reporting companies that remain in scope, timing is tight. FinCEN's regulations require an initial BOI report within 30 days of formation or registration notice, and later changes or corrections generally must be reported within 30 days after the change, as summarized in this review of the beneficial ownership information reporting final regulations.

The March 2025 narrowing also created specific deadlines for foreign reporting companies. Under the same general rule change discussed earlier, foreign reporting companies registered before March 26, 2025 had to file by April 25, 2025, while those registering on or after that date generally had 30 calendar days after notice that registration was effective.

Canadian timing is different

Canada's federal model is less about one filing deadline and more about continuous maintenance. The ISC register has to be accurate, and companies should treat ownership and control changes as events that require prompt review.

That means your calendar trigger in Canada shouldn't be "annual compliance only." It should also include financings, ownership transfers, board changes, and control shifts that happen mid-year.

A quick self-check

- Foreign entity in the U.S.: Confirm whether your registration status makes you a reporting company.

- Recently formed or registered: Assume the timeline is short until proven otherwise.

- Change in ownership or control: Review update obligations immediately.

- Canadian federal corporation: Treat the ISC register as a live record, not a file drawer document.

Penalties Documentation and When to Seek Counsel

The penalty conversation gets attention because it should. In the U.S., noncompliance can be expensive and personal.

According to the March 2025 reporting discussion cited earlier, civil penalties have been cited at $500 per day, adjusted for inflation to $591 per day, and criminal exposure can include a $10,000 fine and up to two years in prison for willful violations, as noted in the same Moody's BOI reporting summary.

Documentation is where compliance succeeds or fails

The filing or register entry is only the visible part. The harder issue is proving why the company identified certain people as beneficial owners and not others.

Useful documentation often includes:

- Ownership records: Share registers, subscription agreements, and transfer documents

- Control records: Bylaws, shareholder agreements, veto rights, and appointment powers

- Identity materials: The personal details required for in-scope U.S. filings

- Change logs: Notes showing when the company reviewed changes and updated records

FinCEN's framework requires reporting companies to identify individuals who exercise substantial control or own at least 25%, and the information includes detailed identity reporting, reflecting the anti-shell-company purpose of the law, according to the FinCEN BOI FAQs.

When should you involve counsel

You probably don't need a memo for a simple company with one shareholder and no unusual rights. You probably do need legal review when control is split, indirect, contractual, or disputed.

Typical triggers include:

- Layered ownership: Parent companies, holdcos, or cross-border chains

- Control below 25%: Special rights that may amount to substantial control

- M&A activity: Acquisitions, roll-ups, or post-closing reorganizations

- Nominee or family structures: Legal ownership and practical control don't match

- Urgent timing: Registration has already happened and the clock may be running

Good compliance records do two jobs. They support the filing, and they show how the company reached its conclusion.

If you're assigning internal responsibility for these issues, this practical overview of compliance officer responsibilities is a good place to start.

Frequently Asked Questions

Do most U.S. companies still have to file beneficial ownership information?

No. As of March 26, 2025, FinCEN states that entities created in the United States and U.S. beneficial owners are exempt from BOI reporting, while certain foreign entities registered to do business in the U.S. remain in scope. For many businesses, the current question is no longer universal filing. It is whether a foreign registration still creates an active obligation.

What information is usually involved in beneficial ownership reporting?

Where U.S. BOI reporting applies, the required information can include names, dates of birth, addresses, and identification numbers for beneficial owners. In both U.S. and Canadian practice, companies also need supporting corporate records that explain why those individuals were identified. The legal conclusion matters, but the file behind it matters just as much.

Is beneficial ownership a one-time exercise?

Usually not. Even where the original analysis was correct, later changes can make it wrong. New investors, management turnover, redemptions, shareholder agreements, and reorganizations can all affect who has ownership or substantial control. In practice, companies get into trouble when they treat beneficial ownership as part of formation only and ignore it during later transactions.

Can I handle this myself without a lawyer?

Sometimes, yes. A simple structure with clear direct ownership may be manageable internally if someone is responsible for records and deadlines. The risk rises quickly when ownership is indirect, cross-border, or subject to special control rights. DIY work tends to fail when the company can identify shareholders on paper but can't explain who ultimately controls the business.

Does a Canadian company with U.S. activity need to review both systems?

Usually, yes. A Canadian company may have Canadian corporate record obligations and, if it registers to do business in the U.S. through a foreign entity, it may also need to analyze whether U.S. BOI reporting still applies. That is why cross-border businesses should avoid using a single checklist for both countries. The systems ask related questions, but they don't work the same way.

Conclusion

If you expanded across the U.S.-Canada border and just ran into beneficial ownership reporting requirements, the key is to stop relying on old assumptions. The U.S. rule changed dramatically in March 2025, and many domestic U.S. entities are no longer the focus. Canada still requires disciplined record-keeping, and foreign entities with U.S. registrations may still face active BOI obligations. The safest approach is to confirm your entity's status, map actual control, and keep the records current before a deadline or transaction exposes the gap.

How Mayo Law Can Help

Mayo Law serves clients across Toronto, the GTA, and on cross-border matters. If your business is sorting out U.S. BOI exposure, Canadian ISC record issues, or a cross-border ownership change, legal review can help you classify the entity correctly and build a workable compliance process. To discuss your matter, visit Mayo Law's compliance services.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

- International business legal services

- Business immigration legal services

- White-collar and investigations services

If your company operates across Canada and the United States, beneficial ownership problems usually show up when time is short and the records are incomplete. Mayo Law advises on cross-border compliance, corporate governance, and related U.S.-Canada legal issues so businesses can address these questions before they become filing, transaction, or enforcement problems.

![Yellow decorative banner with a maple leaf and city skyline; title reads 'Employment Immigration Attorney Guide for US-Canada Business'.] ,](https://mayo.law/wp-content/uploads/2026/06/employment-immigration-attorney-business-guide-1024x569.jpg "employment-immigration-attorney-business-guide - Mayo Law")