A common E-2 scenario looks like this. A founder has a real plan to enter the U.S., enough capital to launch, and a business model that does not require a warehouse, expensive equipment, or a long payroll on day one. The hesitation usually starts when the legal standard shifts from business reality to evidence. Terms like substantial, at risk, and non-marginal sound straightforward until an adjudicator asks how a lean service business will produce more than a modest living.

That issue comes up often with consultants, agencies, software-enabled service companies, professional practices, and other low-overhead ventures. A smaller budget does not automatically weaken an E-2 case. It does mean the file has to be built carefully. Officers want to see that the investment is substantial in relation to the actual cost of starting this specific business, and that the company has a credible path to revenue, staffing, or broader economic activity beyond supporting the investor alone.

Mayo Law advises founders and investors in Toronto, the GTA, and cross-border matters that often involve both Canadian and U.S. planning. If you want a practical overview of investor options, start with a business immigration lawyer for cross-border investors. The strongest E-2 cases treat the application as part of a market-entry plan, with the legal standard, the spending pattern, and the business model aligned from the start.

What Are the Core E2 Visa Qualifications?

E-2 visa qualifications are the core legal requirements an investor must meet to qualify for treaty investor status in the United States. In practical terms, the case must show treaty nationality, a substantial investment in a real U.S. business, active control by the investor, a non-marginal enterprise, and funds that are committed and at risk.

- Treaty nationality: You must hold citizenship in a treaty country.

- Substantial investment: Capital must fit the actual cost of the business.

- Bona fide enterprise: The U.S. business must be real and active.

- Develop and direct: You need control or a managerial directing role.

- Non-marginal business: The enterprise must do more than support one household.

- Funds at risk: Money must be irrevocably committed and exposed to loss.

- Intent to depart: You must intend to leave when E-2 status ends.

A point many applicants miss is the develop and direct requirement. The applicant must hold at least 50% ownership or operational control via a managerial position, and the enterprise must be active, not a passive holding. The business also has to be past the idea stage and already trading or imminently ready to trade, as explained in this discussion of E-2 treaty investors and employees.

Practical rule: Adjudicators don't approve business concepts. They approve operating businesses, or businesses that are clearly ready to start operating immediately.

Who Qualifies as a Treaty Investor?

A founder can have money wired, a lease signed, and a credible launch plan, then lose the case on a point that should have been settled at the start: treaty nationality.

E-2 classification is available only to a citizen of a country that has the required treaty relationship with the United States. For an individual applicant, the analysis starts with citizenship. Permanent residence does not qualify. A company's place of incorporation does not control the answer by itself. Adjudicators want to see who owns the business and whether that ownership gives the enterprise treaty-country nationality.

Individual nationality and company nationality

If you are filing as the investor, your passport has to match a qualifying treaty country. If the investor is a business entity, the ownership chain has to be documented cleanly enough to show that the company itself has the right nationality.

USCIS explains that where the employer is not an individual, it must be at least 50% owned by persons with the nationality of the treaty country, as outlined on the USCIS E-2 treaty investors page.

That sounds straightforward. In practice, it is where many otherwise viable cases weaken. Cap tables change. Shares sit in holding companies. A co-founder from a non-treaty country comes in early and no one asks what that does to E-2 eligibility until the filing is already underway.

The Canadian founder problem

I see this often with Canadian founders. They assume a business operating from Canada, banking in Canada, or incorporated in Canada automatically fits the E-2 rules. It does not. The legal question is nationality under the treaty framework, not commercial ties to Canada.

If you are sorting out that issue, this article on whether a Canadian can get an E-2 visa is the better starting point than generic summaries.

The practical problems usually look like this:

- Strong setup: The investor and the U.S. entity have a clean ownership trail showing treaty-country nationality from the top down.

- Weak setup: The founder relies on a Canadian operating history but cannot show qualifying ownership through the actual U.S. applicant entity.

- Strong setup: Passport records, share certificates, cap tables, and formation documents all tell the same story.

- Weak setup: The structure was revised shortly before filing, and the beneficial ownership records do not line up.

If the ownership chart takes too long to explain, the case usually needs work before it is filed.

Why this matters for service businesses

This issue matters even more for service-based and lower-overhead businesses because the nationality question is often the easiest part of the case for an officer to test quickly. A digital agency, consulting practice, software implementation firm, or design studio may have a sensible E-2 model with modest startup costs. But if the ownership evidence is muddy, the case can fail before the officer ever gets to substantiality or marginality.

That is a real trade-off. Founders often spend time polishing projections and market materials when the better use of time is fixing entity structure, confirming who owns what, and making sure the U.S. company is the right applicant.

A practical scenario

Take a Toronto founder with a profitable service business, U.S. client demand, and a plan to open in New York. Commercially, that may be a sound move. For E-2 purposes, though, the case still turns first on whether the U.S. entity is at least half owned by qualifying treaty-country nationals and whether the records prove it clearly.

Nationality is a threshold issue. If it is weak, the rest of the file does not get much room to recover.

How Much Do I Need to Invest for an E2 Visa?

A founder sets up a U.S. consulting company, wires $25,000 into the business account, pays the filing fees, launches a website, and assumes that is enough for an E-2. In many cases, it is not. The question is not whether the investor put in a round number that sounds serious. The question is whether the investor has committed a substantial amount in relation to the actual cost of this specific business.

There is no fixed statutory minimum for the E-2. Adjudicators apply a proportionality analysis. The lower the total cost of the business, the more of that cost the investor usually needs to have already spent or firmly committed. One commonly cited explanation states that enterprises under $500,000 typically require 75% or more of total cost invested, while enterprises above $3 million may qualify with 30% to 40% if viability is shown, according to this explanation of E-2 qualifications and investor visa requirements.

That framework matters most for modern service businesses. A digital agency, software implementation firm, design studio, recruiting company, or consulting practice often has a legitimate startup model with far less overhead than a restaurant or manufacturing operation. That does not make the case easier by default. It usually means the officer will look more closely at whether the claimed startup budget is real, whether the business is actually ready to operate, and whether the investor has committed enough to reach that point.

In practice, weak service-business cases often fail because the investor understates the true cost of launch. If the business needs staff, sales systems, software licenses, insurance, leased space, contractor support, marketing, and working capital to function for the first several months, those costs belong in the analysis. A low-overhead model can qualify, but only if the numbers are honest and the spending matches the business plan.

For a detailed breakdown of how this applies in 2026, see our guide on the E-2 visa minimum investment amount.

What officers want to see

Officers do not give much weight to money sitting idle in a personal account. They want to see funds that are at risk and tied to the business. That usually means money already spent on startup costs, inventory, equipment, lease obligations, professional fees, technology, payroll setup, or other expenses that cannot be casually reversed.

For service businesses, this point is easy to miss. The investor may assume that because the business can be run lean, a small bank balance is enough. Usually it is not. A stronger file shows that the investor has already built the operating platform of the company and can explain why the amount invested is appropriate for that model.

Common problems include:

- Idle cash: Funds remain in a personal or business account without a clear business use.

- Circular transfers: Money moves through related accounts and the path is hard to trace.

- Incomplete source documentation: Large deposits appear without sale records, tax records, loan documents, or transfer history.

- Revocable commitments: The investor can recover the funds too easily because the spending is not final or the contracts are not binding.

I also look closely at whether the spending pattern makes commercial sense. If the plan says the company will serve enterprise clients, but the investment only covers formation, a logo, and a basic website, adjudicators notice that gap quickly. A persuasive E-2 file does not always require a large investment. It does require a credible one.

Proving Your Business is Real and Non-Marginal

A founder launches a U.S. marketing agency, software consultancy, or design firm with little overhead, a clean website, and real industry experience. On paper, the business looks viable. In an E-2 case, that alone is rarely enough. The officer wants to see an operating business with a credible path to producing more than a living for the investor.

That is the practical challenge for service businesses. The company may be legitimate and commercially sensible, but the file still has to prove two separate points. First, the enterprise is real now. Second, it is not marginal.

What “real” looks like

A bona fide enterprise is an active commercial business. It is not a shell entity, passive holding structure, or speculative idea waiting for funding after approval.

For a service-based company, proof of present or imminent operations often matters more than the absence of a storefront or expensive equipment. Good cases usually include signed client agreements, a lease or coworking arrangement if one makes sense for the model, payroll setup, professional software, vendor contracts, insurance, operating accounts, and evidence that the company can deliver services immediately.

I often see borderline cases in consulting, digital services, and other low-overhead models. The investor has the right background and a plausible plan, but the record only shows incorporation, a website, and a small amount of startup spending. That leaves an obvious question for the adjudicator. If this business is prepared to operate, where is the operating structure?

The answer does not have to be a large equipment budget. It does have to fit the business. A strong file shows why the company can start lean, what has already been built, and how the existing commitments support real revenue-generating activity.

What “non-marginal” really means

Marginality is where many modern E-2 cases weaken. The issue is not whether the business can support the investor for a period of time. The issue is whether the enterprise has the present or future capacity to make a meaningful economic contribution beyond providing a job for its owner.

Officers look closely at that point in service businesses because the startup costs are often modest. A company with low overhead can still qualify, but low overhead creates pressure to prove substance in other ways. That usually means a believable revenue model, identifiable U.S. customers or contracts, hiring plans that match the economics of the business, and a timeline that makes commercial sense.

Profitability by itself does not resolve marginality. A solo founder earning enough to cover personal expenses may still have a weak case if the business appears likely to remain a one-person practice with no broader U.S. impact. By contrast, a company that starts lean but can show signed work, recurring revenue, subcontractor use, or planned hiring often presents a stronger argument.

Evidence that helps a modern service business

Mayo Law works with founders across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, so clients with U.S. ties can coordinate related legal work in one place.

For a remote or service-based E-2 case, the evidence should answer a practical question. Why is this business more than a self-employment arrangement dressed up as a company?

Useful evidence often includes:

- Signed U.S. client contracts: Actual commitments carry far more weight than general market interest.

- Detailed letters of intent: Helpful if the company is close to launch and can tie the expected work to specific revenue.

- A hiring forecast tied to revenue assumptions: Officers notice when staffing projections are disconnected from the numbers.

- U.S. vendor or platform relationships: These help show the business is integrated into the U.S. market.

- Delivery infrastructure: Software stack, workflows, contractors, compliance steps, and other operational pieces that show the company can perform the work now.

- Proof of recurring or scalable revenue: Retainers, subscriptions, licensing arrangements, or repeat customer pipelines can help distinguish a business from a one-off freelance practice.

A thin-cost startup can qualify. A thin-evidence startup usually will not.

If marginality or commercial reality is likely to be a close issue, the business plan needs to do real work. A strong E-2 visa business plan ties the investment amount, operating structure, contract pipeline, revenue assumptions, and hiring path to the actual economics of the business. That is often where service-based cases are won or lost.

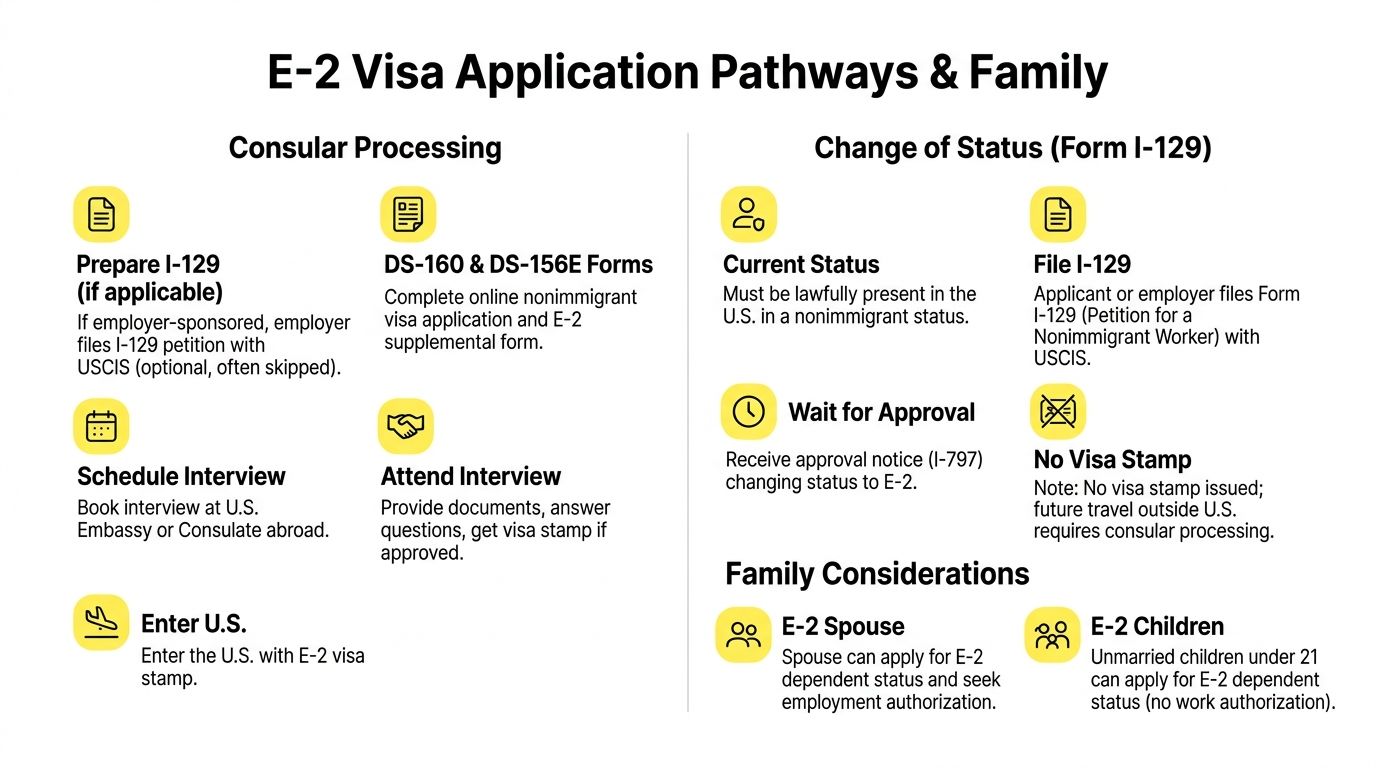

Application Pathways and Family Considerations

A common decision point comes after the business case is ready. The investor may be in the United States in valid status and tempted to file a change of status because it looks faster or less disruptive. That can work. It also creates travel limits that many founders do not fully account for until they need to leave for a client meeting, family emergency, or visa renewal.

Consular processing versus change of status

The two main routes are consular processing abroad and a change of status through USCIS. The better option depends on travel needs, timing, and risk tolerance, not just filing convenience.

| Pathway | Main benefit | Main drawback |

|---|---|---|

| Consular processing | Results in an actual E-2 visa for travel | Requires embassy or consulate processing abroad |

| Change of status | Useful if you’re already in valid U.S. status | Doesn’t give you a visa stamp for re-entry |

For founders who expect regular international travel, consular processing is often the cleaner path. If USCIS approves a change of status inside the United States, you may hold E-2 status for domestic purposes, but that approval does not give you a visa foil in your passport. After departure, you usually need a consular E-2 visa to return in that classification. USCIS filing details and forms remain available through USCIS forms and processing information.

In practice, I also look at the business model. A service business with low overhead often depends on the founder's personal sales activity, client delivery, or cross-border travel. In those cases, the procedural choice is not just administrative. It affects how easily the business can operate.

Validity and renewals

Visa validity depends on the treaty country and the reciprocity schedule. Some applicants receive shorter visa validity periods, while others receive longer ones. E-2 classification can be renewed as long as the treaty business remains active and continues to satisfy the rules, including the non-marginality standard discussed earlier.

That renewability is useful, but it should not create complacency. Renewals go better when the file shows real commercial progress: revenue, operating activity, continued investment, and, where the model supports it, growth beyond supporting only the investor's household.

Spouses and children

A spouse and unmarried children under 21 may apply for derivative E-2 status. That sounds straightforward, but family timing often drives the strategy. School calendars, work authorization planning for a spouse, and whether everyone will travel together can affect where and when the principal applicant should file.

Long-term planning matters here too. E-2 status is a nonimmigrant category, even if it can last for years through renewals. Investors who may later want permanent residence should structure the company, ownership, and job role with that possibility in mind. A later path from E-2 status to a green card is often easier to assess early than to retrofit after several years of operating the business.

Frequently Asked Questions

Can I use a loan for an E-2 investment?

Sometimes, yes. The key issue is whether the funds are at risk and properly committed to the business. Debt secured only by the assets of the E-2 enterprise is a problem under the standards summarized in the verified materials. In practice, secured personal assets and clear source-of-funds records are much easier to defend than aggressive or unclear financing structures.

Does my business need employees before I apply?

Not always. A service business can qualify without employees at filing if it is already operating or imminently ready to operate and the record shows it won't remain marginal. What matters is whether the enterprise is real, active, and capable of generating more than household living income or otherwise adding value to the U.S. economy.

What if my case is mostly digital or remote?

That can still work, but the evidence burden is usually heavier. Remote-only ventures often fail because they show revenue potential without showing U.S. economic integration. Contracts with U.S. clients, documented licensing, vendor relationships, and a credible growth plan matter far more than a polished website or broad market research.

Can I apply inside the United States?

If you're already in valid nonimmigrant status, a change of status may be possible. That route can be practical when travel isn't urgent. The trade-off is that approval inside the U.S. doesn't give you a visa stamp for future re-entry, so you may still need consular processing later before returning from travel abroad.

What happens if my E-2 visa is refused?

A refusal is not always the end of the matter. The first step is to identify whether the issue was nationality, investment structure, source of funds, marginality, or weak operating evidence. Some cases can be refiled effectively after restructuring the ownership, improving the business plan, documenting contracts, or correcting the investment trail.

If you're assessing whether your business fits the E-2 category, Mayo Law can help you test the structure, investment record, and business evidence before you commit to a filing strategy.

Conclusion

If you're trying to enter the U.S. market, the E-2 can be a powerful option, but only if the case is built around the rules adjudicators apply. Most problems come from weak ownership analysis, uncommitted funds, or business plans that don't show a real, non-marginal operation. For service businesses and low-overhead startups, the answer usually isn't just spending more. It's proving that the investment is substantial for this business, at risk, and tied to a real U.S. enterprise.

How Mayo Law Can Help

An E-2 case can look straightforward until the weak point appears. For one founder, it is ownership. For another, it is tracing the funds. For many service businesses, a key issue is proving that a lean operation is still substantial and not marginal.

Mayo Law handles cross-border E-2 matters with that in mind. The work usually involves more than preparing forms. It means identifying what an officer or consular post is likely to question, then building the record around those points. That can include documenting the investment path, tightening the business plan, addressing low-overhead models, and making sure the filing matches the procedural route.

We serve clients in Toronto, the GTA, and on U.S. cross-border immigration matters. To discuss your situation, contact Mayo Law directly.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

If your E2 case involves a service business, a cross-border operation, or a company that must stay clean on licensing and corporate formalities, these related topics are usually the next place to look: