You’re forming a New York business, the product is ready, a lease or client contract is close, and then the structuring question lands. Should you use an LLC or a corporation? For founders working across New York and Canada, that question gets harder fast. A Canadian co-owner, future investor, or E-2 visa plan can change the answer.

At Mayo Law, our attorneys often see this issue at the exact moment a startup in Buffalo, a consultancy in Westchester, or an e-commerce business in Brooklyn is about to commit to the wrong structure for its goals. According to U.S. Small Business Administration data summarized here, LLCs make up 35% of U.S. businesses, compared with 20% for corporations. That popularity makes sense, but popularity is not strategy.

Choosing Your New York Business Structure

A founder usually starts with the wrong question. They ask which entity is cheaper to file. The better question is which entity fits how the business will operate, pay tax, add owners, and raise money.

If you’re comparing LLC vs corporation New York which to choose, start with your real business model. A solo consultant entering the U.S. market from Ontario often wants simplicity and tax flexibility. A software company planning to grant equity to employees and pitch investors usually needs a more formal structure. The legal shell should match the business plan, not just the filing form.

A good starting point is to think through choosing the right entity for your U.S. business. Both LLCs and corporations can protect personal assets if they’re set up and maintained properly. The split usually comes down to governance, taxation, funding, and whether cross-border ownership is part of the picture.

Liability Protection and Governance Structure

Both entities are designed to separate business liabilities from your personal assets. That matters if the company signs a lease, takes on debt, hires staff, or faces a contract dispute. But the liability shield only works if the entity is treated like a real business and not your personal checking account with a logo.

How management actually works

An LLC is usually the more flexible option. It can be managed directly by its owners, called members, or by designated managers. That flexibility is often documented in an operating agreement, which can be customized to voting rights, profit allocations, exits, and deadlock rules.

A corporation uses a layered structure. Shareholders own the company, directors oversee major decisions, and officers handle day-to-day operations. That structure is more formal and often more familiar to lenders, investors, and institutional counterparties.

Practical rule: If the owners want broad freedom to design control rights, an LLC often fits better. If they want a conventional governance model that outside investors immediately recognize, a corporation often fits better.

What corporations require that LLCs often avoid

New York corporations come with stricter governance habits. You usually need bylaws, director and shareholder actions, and cleaner records around approvals. If you’re not sure how those internal rules work, start with what company bylaws do and why they matter.

An LLC generally has fewer mandatory formalities. That’s one reason many small businesses prefer it. In practice, that can mean less friction for owner-managed businesses that don’t need board-style decision making.

- LLC fit: owner-operated business, small group of founders, customized economics

- Corporation fit: outside investors, formal approvals, option planning

- Bad fit either way: founders who ignore records, mix personal and business funds, or sign contracts without clear authority

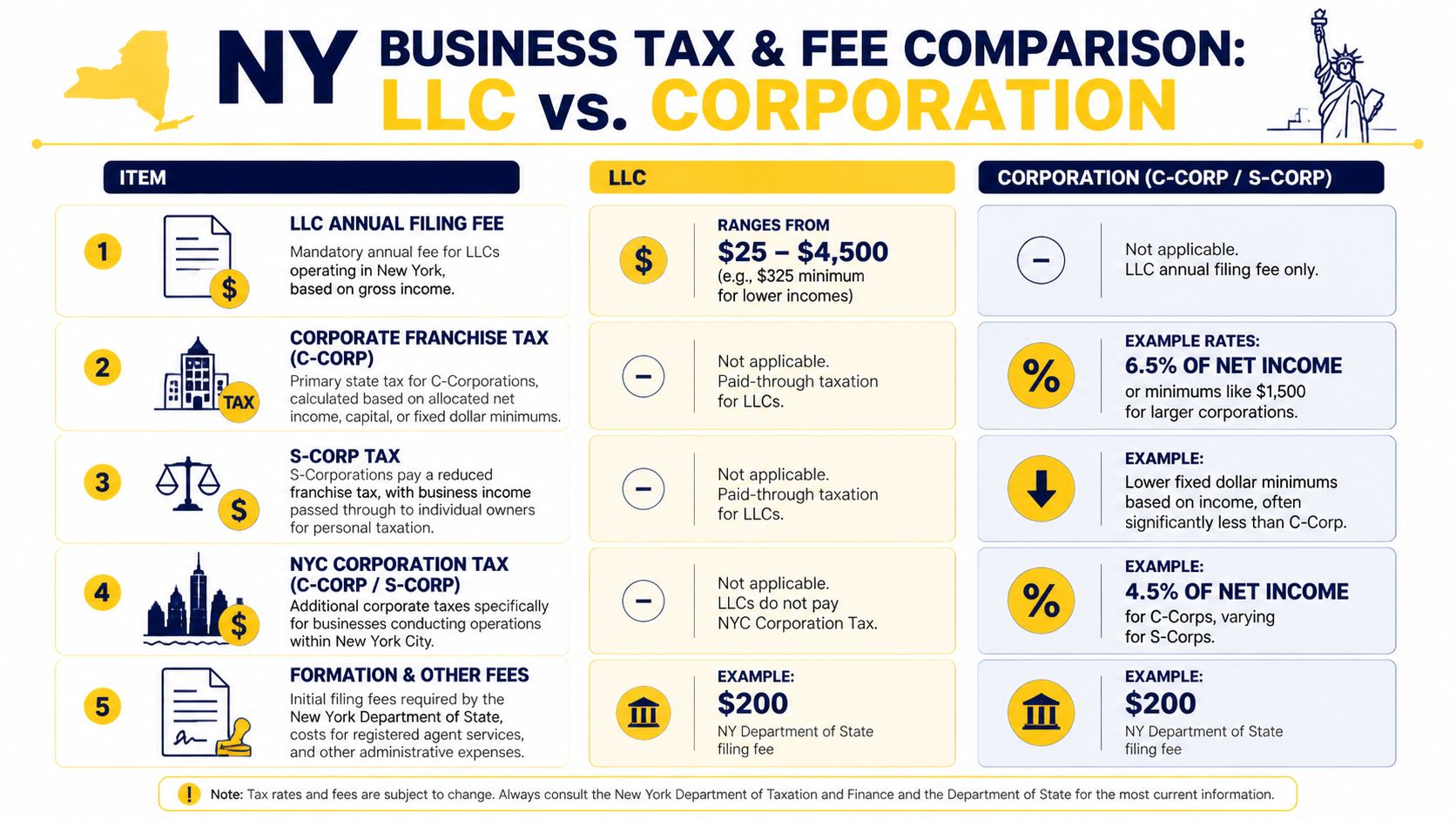

A Deep Dive on Taxation and Fees in New York

The filing fee is only the first cost. New York entity choice affects formation spend, tax treatment, and ongoing compliance.

Formation costs

New York LLCs have a filing cost that looks manageable until the publication rule appears. According to this New York formation guide, an LLC has a $200 state filing fee and must satisfy a publication requirement in two newspapers, with costs often ranging from $500 to over $2,000. A corporation has a $125 filing fee and no publication rule.

That publication requirement surprises many founders, especially those relocating from Canada or another U.S. state. It doesn’t usually make an LLC the wrong choice, but it does affect launch budgeting.

Federal tax treatment

An LLC is commonly chosen for pass-through taxation. That means profits usually pass to the owners’ personal returns rather than being taxed first at the entity level and then again when distributed. For many closely held businesses, that’s attractive because it keeps the tax picture simpler.

A C corporation is different. It is its own taxpayer, so business income may be taxed at the company level, and distributions to shareholders can create a second layer of tax. That structure is often less appealing for a small company that expects to distribute earnings rather than reinvest for growth.

A founder who wants cash flow today often values pass-through treatment differently than a founder who wants to reinvest and build for a future financing round.

New York and city-level issues

An LLC may also face ongoing New York filing fees that scale by gross income. If the business operates in New York City, the city tax picture may also matter. A corporation may avoid some of the pass-through issues that make LLC planning more complex, but that comes with its own compliance burden.

The lesson isn’t that one is always cheaper. It’s that the cheaper filing choice and the smarter long-term choice are often different.

Quick Comparison LLC vs Corporation in New York

If you need a working summary before deciding, use this as a quick reference.

| Feature | New York LLC | New York Corporation |

|---|---|---|

| Liability protection | Personal asset protection if properly maintained | Personal asset protection if properly maintained |

| Governance | Flexible. Member-managed or manager-managed | Formal. Shareholders, directors, officers |

| Internal rules | Operating agreement driven | Bylaws and board-style governance |

| Formation cost | Higher upfront because of filing fee plus publication requirement | Lower upfront filing cost, no publication rule |

| Tax default | Pass-through by default | C corporation taxation unless other tax election applies |

| Investor appeal | Often less attractive for institutional equity raises | Usually more familiar for outside investment |

| Ownership flexibility | Can admit foreign members | S corporation status is not available to foreign owners |

| Best use case | Closely held business prioritizing flexibility | Business planning to scale through equity and formal governance |

Planning for Growth Investor and Funding Paths

A business built to stay founder-owned often has different needs than a business built to raise capital. That’s where the corporation usually becomes the stronger candidate.

Why growth companies often lean corporate

Corporations are built around shares. That makes it easier to issue equity, create classes of stock, document investor rights, and build employee incentive plans. If you expect to negotiate term sheets, preferred rights, or an acquisition, the corporate format tends to create fewer structural headaches.

That matters before the financing documents are even drafted. Founders often underestimate how much future fundraising depends on today’s formation choice.

If your business expects to issue founder equity or bring in investors under negotiated terms, review how stock purchase agreements shape ownership and control before you choose a structure.

The S corporation trap for cross-border founders

Some founders hear that an LLC can elect S corporation tax treatment and assume they’ve found the perfect hybrid. Sometimes that works for a U.S.-only business. It often fails for cross-border ownership.

According to this comparison of LLCs and S-corps in New York, LLC members pay 15.3% self-employment tax on all pass-through income. The same source notes that an S-Corp can reduce that burden on distributions, but New York S-Corps have strict formalities and are limited to 100 U.S. citizen or resident shareholders.

If a Canadian founder, spouse, holding company, or investor is likely to be on the cap table, S corporation planning can collapse before it starts.

That’s why high-growth and cross-border businesses usually separate the tax discussion from the ownership discussion. The right answer isn’t just about saving tax this year. It’s about not breaking the structure when funding arrives.

The Cross-Border Angle for US-Canada Businesses

Generic New York formation advice often falls short. A structure that works for a purely domestic U.S. business may create real friction once Canadian ownership, tax reporting, or immigration planning enters the picture.

Foreign ownership changes the analysis

New York LLCs can admit foreign owners. That includes Canadian individuals and Canadian corporations. By contrast, an S corporation is not available if the business has Canadian co-owners. That rule is stated directly in this cross-border-focused discussion of New York entities.

That one point alone resolves the issue for some founders. If the business has or may have Canadian equity holders, S corporation treatment may not be an option.

Tax treaty friction is real

An LLC’s pass-through treatment can be attractive on the U.S. side, but it may not line up cleanly with Canadian tax treatment for Canadian residents. That can create planning challenges, especially when founders assume the U.S. tax answer automatically carries over into Canada.

This is why cross-border businesses often need the structure reviewed alongside the ownership map, compensation model, and future transfer plan. A Canadian founder who plans to expand through New York may also want to compare U.S. formation with an Ontario incorporation checklist for founders operating in both markets.

For a U.S.-Canada business, the cleanest entity on paper is not always the cleanest entity at tax time.

Immigration and investor planning

Entity choice may also affect how clearly ownership and investment are documented for business immigration purposes. For some founders, especially Canadians exploring U.S. operating roles, a corporation can present a more familiar share-based ownership structure. For others, an LLC may still work, but the documents need to be carefully aligned with the business plan.

If your ownership structure, compensation, and immigration strategy point in different directions, the entity usually needs to be rethought before filing.

Making the Right Choice A Decision Framework

Most founders don’t need a perfect entity. They need the entity that creates the fewest problems for the next stage of the business.

You might choose an LLC if your priority is operational flexibility, owner-managed control, and pass-through taxation. That’s often the practical route for a solo founder, a family business, or a small services company that isn’t planning a venture-style capital raise.

A corporation often makes more sense if you expect to issue equity, build a formal governance structure, or prepare for outside investment. It can also be the cleaner platform when the business is being built for a sale, a larger financing, or more structured internal controls.

Use these considerations:

- Choose an LLC if you want flexible economics and simpler day-to-day governance.

- Choose a corporation if your cap table is likely to grow and investor expectations matter.

- Pause before choosing S-Corp treatment if any current or future owner may be Canadian.

- Revisit the plan if immigration, tax, and ownership are being handled separately. Those decisions need to line up.

- Document founder expectations early. A strong structure can still fail if the owners never settle transfer rights, deadlock terms, and exit rules. In such scenarios, shareholder agreement planning becomes just as important as the formation filing.

Build Your Business on Solid Legal Ground

Before you file, pressure-test the structure against four things. Who owns the business, how profits will be taxed, whether outside funding is realistic, and whether Canada-U.S. issues are in play. Those questions usually matter more than the filing fee.

Build Your Business on Solid Legal Ground. Mayo Law advises startups and SMEs in Ontario and New York. Contact Mayo Law to discuss your needs.

LEGAL DISCLAIMER: The information provided in this article is for general informational and educational purposes only and does not constitute legal advice. Reading this article, visiting mayo.law, or contacting Mayo Law does not create an attorney-client relationship. The content of this article should not be relied upon as a substitute for professional legal counsel suited to your specific circumstances. Legal outcomes depend on the particular facts and circumstances of each individual case, and no attorney can guarantee a specific result. Laws, regulations, and legal procedures are subject to change and may vary by jurisdiction. If you require legal assistance, you should consult with a qualified attorney licensed to practice in the relevant jurisdiction. Mayo Law expressly disclaims any and all liability with respect to actions taken or not taken based on the contents of this article.