A Canadian founder often reaches the immigration question after the business work is already underway. The U.S. entity is formed, early customer conversations look promising, capital is being committed, and then the practical question lands. Who will enter the United States to direct the company on the ground? At that point, the requirements for e2 visa eligibility stop being a generic checklist and become a filing strategy.

The E-2 is often a good fit for startups and owner-led SMEs, but approval turns on evidence, not pitch-deck logic. As practitioners helping Canadian founders with U.S. expansion, we see the same pattern repeatedly. A viable business can still fail if the record does not clearly show treaty nationality, funds committed and at risk, a real operating plan, and a role that supports develop-and-direct authority. A general E-2 visa guide for investing in and building your business in the U.S. is a useful starting point, but Canadian cases usually succeed or fail on the quality of the documents behind each legal element.

That is the issue for cross-border founders. The standard is legal, but the work is evidentiary.

Published: May 20, 2026

Updated: May 20, 2026

Read time: 11 minutes

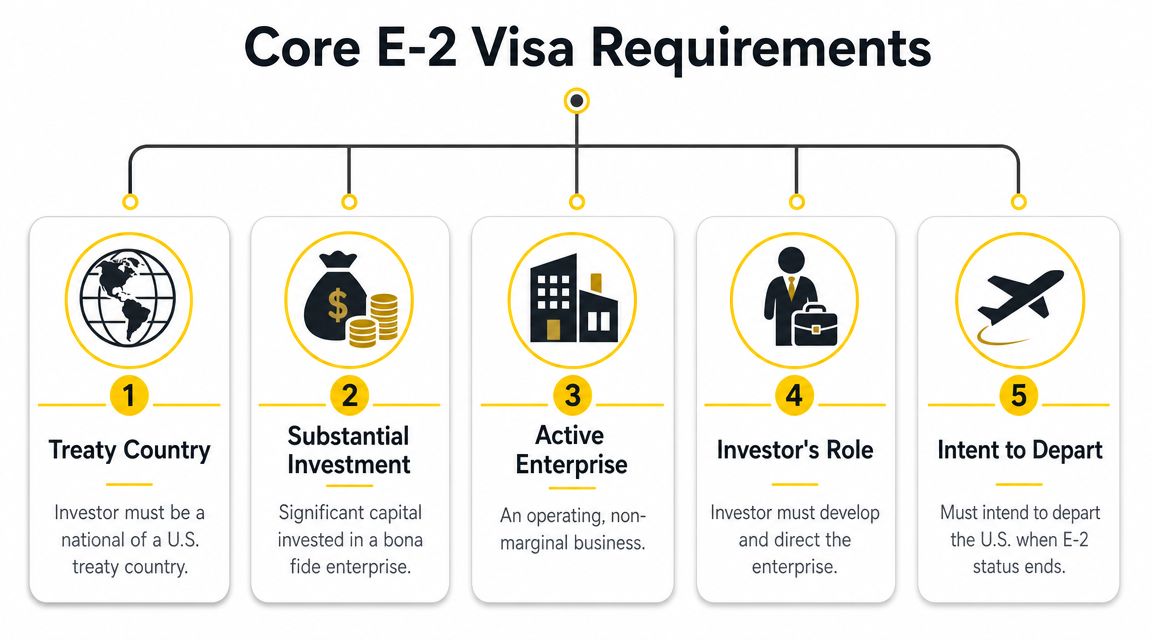

What Are the Core E-2 Visa Requirements?

The core E-2 visa requirements are:

- Treaty nationality. You must be a national of a treaty country, and the U.S. business must also have treaty-country nationality.

- A substantial investment. There is no fixed statutory minimum, but the capital must be sufficient for the specific business and placed at risk.

- A real operating enterprise. The business must be active and bona fide, not passive or speculative.

- A non-marginal business. The enterprise must do more than merely support the investor and family.

- A develop-and-direct role. You must be coming to direct and develop the company, not just hold a passive ownership stake.

That sounds simple on paper. In actual filings, each point becomes a documentation exercise. Ownership charts, bank records, leases, contracts, hiring plans, and role descriptions often matter as much as the legal standard itself.

A useful starting point is understanding that there is no single magic number for the investment. If you're trying to assess capitalization, this discussion of E-2 visa minimum investment amount is the right place to start before you wire funds.

The Five Statutory Pillars of an E-2 Visa

A founder often clears the legal test on paper and still loses on proof. The usual problem is not the rule itself. It is the record. In E-2 filings, especially for startups and owner-operated SMEs, each pillar has to be shown with documents that line up and tell one credible story.

Treaty nationality

Nationality is usually simple for the individual applicant and much harder for the business. The company must be at least 50% ultimately owned by nationals of the same treaty country. For Canadian cases, I often see trouble after a seed round, a SAFE conversion, or a parent company structure that no one mapped carefully.

Officers do not stop at the certificate of incorporation. They look through the ownership chain to the ultimate owners.

What helps:

- A current cap table that matches the share ledger and governing documents

- An ownership chart showing each entity layer up to the ultimate individual owners

- Copies of passports or other nationality evidence for the owners whose citizenship establishes treaty nationality

- Clear explanations of SAFEs, options, side letters, and voting rights

What creates risk:

- Using a stale cap table that ignores post-closing changes

- Assuming a U.S. company with a Canadian founder is automatically a Canadian E-2 company

- Letting treaty-country ownership fall below 50% after fundraising

- Leaving control rights unclear where equity and voting power do not track neatly

For cross-border Canada-U.S. structures, this issue comes up more than founders expect. A file can look strong commercially and still fail because the ownership evidence is inconsistent.

Substantial investment

There is no fixed statutory minimum. The question is whether the amount is substantial for this business, whether the funds are at risk, and whether the investment is already committed in a meaningful way.

That test is practical. A software consultancy can launch with a smaller budget than a restaurant, light manufacturing operation, or retail location. Officers compare the money spent or committed against what the business realistically requires to open and operate.

A useful way to frame the analysis is proportionality:

| Business type | What the officer is likely testing |

|---|---|

| Consulting or software services | Whether the investment covers launch costs, operating runway, and real market entry |

| Retail, food service, or other premises-based business | Whether the funds cover lease obligations, buildout, equipment, inventory, and opening expenses |

| Acquisition of an existing business | Whether the purchase terms show committed funds, transfer of control, and enough capital to keep operating |

For startups and small businesses, the evidentiary standard matters as much as the amount. Bank statements alone are weak if the money is just parked. A stronger record shows where the funds came from, how they moved, and what they were used for. Typical evidence includes wire confirmations, signed lease obligations, equipment purchases, software contracts, payroll setup, marketing spend, licensing fees, and escrow terms if the case involves a closing that depends on visa approval.

Smaller investments often receive closer review. The way to address that is not by arguing in the abstract. It is by showing a tight startup budget, credible launch costs, and proof that the business is funded for the model you chose.

A real and operating enterprise

The company must be active, bona fide, and producing or preparing to produce goods or services for profit. A passive holding vehicle does not qualify. Neither does a company that exists only on formation documents and a business bank account.

Timing matters in this scenario.

Founders often want to file as soon as the entity is formed and the funds arrive. That can be too early. If the record shows only incorporation papers, a draft website, and unspent capital, the business may look speculative. A better file usually includes concrete operating commitments such as a commercial lease, vendor contracts, customer outreach records, software subscriptions, insurance, branding invoices, inventory orders, or state and local registrations.

For a Canadian founder opening a U.S. subsidiary, I also want the file to explain why the U.S. operation is real on day one. If work will be performed in the United States, say how. If the company will serve U.S. clients, identify the pipeline. If the founder will split time between Canada and the United States, the operational plan needs to show what is happening in each location and who is responsible for what.

A real enterprise looks organized before the officer ever reads the business plan.

More than marginal

The business must have the present or future capacity to generate more than enough income to support the investor and the investor's family. For new businesses, future capacity is often the issue. The case rises or falls on whether the growth story is specific, funded, and tied to the documents.

Generic projections do not help much. Officers see many plans that promise rapid hiring and steep revenue growth without showing how either one will happen. A useful E-2 business plan connects the dots between invested capital, operating expenses, sales activity, pricing, and hiring.

Good evidence of non-marginality often includes:

- A hiring plan with timing, roles, and salary assumptions that fit the budget

- Revenue projections tied to actual products, services, pricing, and sales channels

- Letters of intent, signed contracts, or purchase orders, where available

- Market-entry evidence such as distributor conversations, customer pipeline reports, or vendor commitments

- Financial statements and budgets that match the capital already spent or committed

I pay close attention to internal consistency here. If the plan says the company will hire three U.S. workers in year one, the cash flow should show how payroll will be funded. If the company projects strong sales in the first two quarters, the file should show some basis for that assumption. For SMEs, measured growth with clean support is usually more persuasive than aggressive projections copied from a startup pitch deck.

Develop and direct

The investor must be coming to develop and direct the enterprise. In founder cases, that usually means at least 50% ownership, or a smaller stake combined with operational control. The file should prove both legal authority and real business responsibility.

Officers want to see who makes decisions.

A persuasive record usually includes:

- Formation and governance documents showing authority to manage the company

- Ownership records and voting rights

- An organizational chart that places the applicant at the top of the operating structure

- A detailed role description focused on management, strategy, hiring, budgeting, sales oversight, or product leadership

- Evidence of actual involvement such as signed contracts, board consents, hiring decisions, or customer development activity

Risk increases when the applicant's role reads like a technical contributor, outside consultant, or passive investor. That issue comes up in startup cases where a founder has strong product skills but delegated management on paper. The solution is not to inflate the title. It is to document real control over the business and define who reports to the applicant, what decisions the applicant makes, and how that authority appears in the company documents.

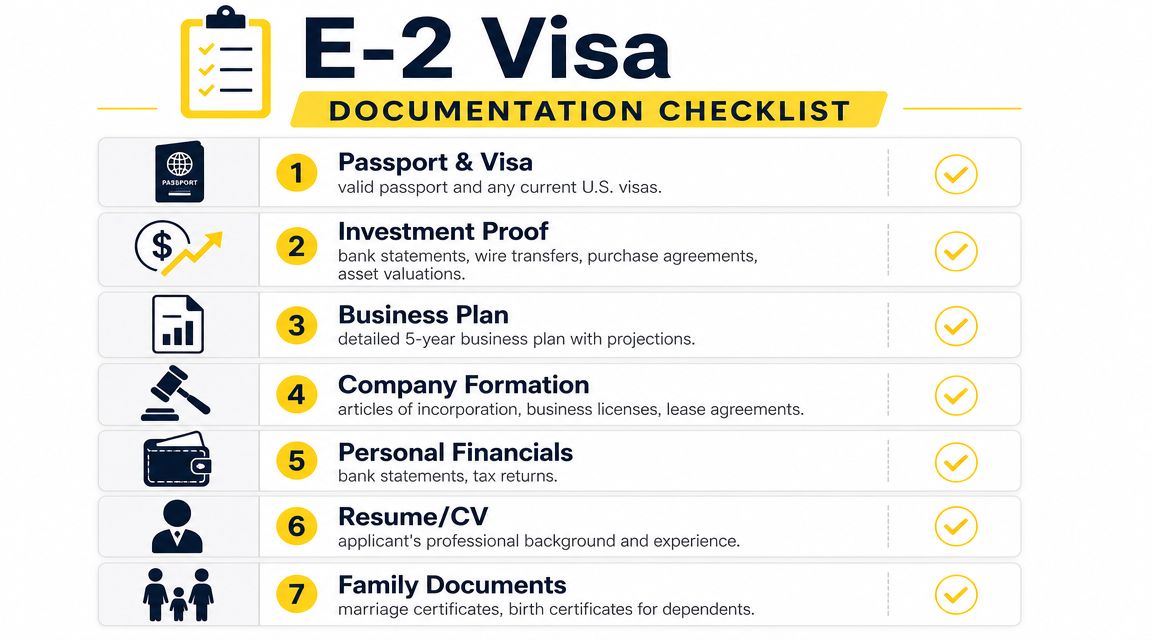

Your E-2 Visa Documentation Checklist

The legal standard matters, but E-2 cases are won or lost on paper. Founders usually know the story of their business. The problem is turning that story into an evidentiary record that an officer can review quickly and trust.

Corporate and identity documents

Start with the basic set, then make sure the documents agree with each other.

- Passport proof showing treaty-country nationality.

- U.S. company formation documents such as articles, certificates, and registrations.

- Share records and cap table showing who owns what.

- Operating agreement or bylaws establishing control rights.

- Organizational chart showing the applicant's position.

For startups, the cap table is where legal theory meets reality. If there are notes, SAFEs, side letters, or a parent entity, someone needs to map them cleanly.

Investment and operating evidence

The officer needs to see that the capital is committed to an actual business.

- Business bank statements

- Wire confirmations

- Asset purchase agreements

- Commercial lease and rent payments

- Equipment, inventory, or software invoices

- Licensing, payroll, insurance, or vendor setup documents

If you're building the operating record, an appropriate E-2 visa business plan should support the file, not try to rescue weak evidence after the fact.

How do you prove the source of E-2 visa funds?

You prove source of funds by tracing the money from lawful origin to the U.S. business. That can require bank records, tax returns, loan documents, and sale agreements. Public guidance also emphasizes that the funds must already be committed or in the process of being invested, not parked in an account, as explained in this E-2 requirements summary on source of funds.

Source of lawful funds

Otherwise strong cases frequently stall. If money moved through multiple accounts, countries, or family entities, the file must explain the path clearly.

Useful source-of-funds records often include:

- Personal and business tax returns

- Historical bank statements

- Property sale documents

- Share sale or dividend records

- Loan agreements

- Gift documents and proof of donor funds

- Remittance and transfer records

A Canadian founder who funded the U.S. company from proceeds of a prior Canadian business sale may need to show the sale documents, tax reporting, bank receipt of proceeds, transfer into the founder's account, and then transfer into the U.S. business. If one step is missing, the officer may question the entire chain.

How Is the E-2 Visa Different for Canadians?

A common Canadian filing problem looks like this. The founder is clearly Canadian, the business opportunity in the United States is real, and the company is already signing contracts. The visa case still runs into trouble because the ownership chart, funding path, or control rights do not show a treaty enterprise in a way a consular officer can approve quickly.

That is the practical difference for Canadians. Nationality is often the easy part. The harder work is proving that the U.S. business remains at least 50 percent owned by treaty nationals and that the applicant will direct and develop that business under the actual governing documents, not just in the pitch deck.

This issue comes up often in startup structures. A Canadian founder may hold shares through a Canadian corporation, add a U.S. subsidiary, then bring in investors from the United States, India, or Europe. At that point, counsel needs to test the cap table, shareholder agreements, voting rights, and board control before filing. A company can look Canadian in branding and management, but fail the E-2 ownership and control analysis once the documents are examined.

Timing also works differently for many Canadians because cross-border travel is so routine. Founders often enter the U.S. market first and deal with immigration later. That approach can create avoidable risk. If U.S. customer contracts are signed, workers are being lined up, and money is moving into the business before the immigration strategy is set, the filing package usually becomes harder to document cleanly. The better approach is to align entity formation, investment steps, and application timing from the start.

How long does it take for a Canadian to get an E-2 visa?

The timeline depends less on the form and more on the record. A well-prepared Canadian case moves faster because the evidence package answers the officer's questions before the interview. A weak case slows down when ownership is hard to trace, the investment documents do not match the business plan, or the founder waits until urgent travel is already scheduled.

For Canadian startups and SMEs, the primary drafting work is evidentiary. Show who owns what today. Show how that ownership changed over time. Show which entity received the investment, who controlled the funds, and what rights outside investors now hold. In cross-border files, I also want the documents to read consistently across Canadian and U.S. records, including incorporations, share issuances, wire transfers, and commercial contracts.

Canadian applicants should also plan past the first approval. E-2 status can be renewed, but renewal depends on the business continuing to satisfy the category. If permanent residence may become part of the founder's long-term plan, that conversation should happen early, before the company depends on one person's ability to enter the United States.

For founders asking the threshold question, this guide on whether a Canadian can get an E-2 visa covers the starting point. In practice, the harder Canadian cases turn on structure, documentation, and timing.

Common E-2 Application Red Flags and How to Avoid Them

A founder can have a real business, real money at risk, and real plans to hire, and still lose an E-2 case if the record leaves gaps. Officers do not approve effort. They approve evidence that matches the legal standard.

For startups and SMEs, the weak points are usually practical, not theoretical. The investment amount does not line up with the business model. The source of funds is hard to trace across Canadian and U.S. accounts. The cap table suggests control issues that the founder did not address. A polished business plan then tries to carry facts that should have been proven with bank records, contracts, payroll setup, lease terms, and corporate documents.

Investment doesn't fit the business

"Substantial" is always relative to the business you are starting. A software consulting firm can often start with less than a restaurant, manufacturer, or retail operation, but the file still has to show that the capital covers true launch costs and early operating needs.

How to avoid it:

- Build the budget from actual startup costs, not round numbers

- Show signed or draft contracts, equipment quotes, lease terms, and payroll assumptions

- Make the business plan match the bank statements and disbursements

- Explain why this amount is enough to get the company open and operating

Industry choice affects scrutiny. Founders comparing models should review which business types tend to fit E-2 approval standards well, because the business model drives both the investment analysis and the amount of supporting evidence you will need.

Template business plans and thin operating records

A generic plan signals that the founder has not done the underlying work. Officers can tell when projections were written to satisfy a visa category instead of reflecting a real launch.

The stronger approach is simple. Use a plan tied to the actual business: the city, the target customers, the pricing, the staffing plan, and the timeline for revenue. Then support it with operating evidence. For a startup, that may include a lease negotiation, supplier discussions, a website in development, invoices for equipment, onboarding with a payroll provider, or customer letters of intent. For a Canadian founder entering the U.S. market, I want the record to show why the U.S. operation exists separately and how it will make money on its own.

How to avoid it:

- Use location-specific market assumptions

- Match revenue and expense projections to real contracts or quotes

- Include proof that the business is already being built

- Keep the U.S. entity's story consistent with any Canadian parent or affiliate

Unclear money trail

This is one of the fastest ways to create avoidable trouble. If the officer cannot tell where the money came from, who owned it, how it moved, and whether it was committed to the U.S. business, the case becomes harder than it needs to be.

Cross-border files often break down here. Funds may start in a personal Canadian account, pass through a holding company, move into a U.S. business account, and then pay vendors from a third account. None of that is necessarily fatal, but every step needs a document trail.

How to avoid it:

- Prepare a source-of-funds timeline before filing

- Keep personal, corporate, and investor funds separate

- Document gifts, loans, dividends, or share sale proceeds clearly

- Include wire records, account statements, and corporate approvals where relevant

- Make sure names, dates, and amounts line up across Canadian and U.S. records

Ownership and control problems

Founders often focus on the money and understate the ownership analysis. The treaty investor must have the required nationality and control the enterprise. Startup financing can complicate that quickly.

SAFEs, convertible notes, option pools, and side agreements are common pressure points. So are cross-border structures where a Canadian corporation owns the U.S. company. The question is not whether the structure looks complex. The question is whether the documents prove treaty nationality and control at the level the adjudicator is reviewing.

How to avoid it:

- Map ownership from the U.S. operating company up through every parent entity

- Confirm that voting control matches the story told in the petition

- Review investor rights for veto power or control provisions

- Update cap tables, share ledgers, and resolutions before filing

Can an E-2 visa be denied?

Yes. Denials often come from preventable problems: weak proof that the investment is substantial for that specific business, incomplete source-of-funds records, ownership documents that do not clearly establish treaty nationality or control, and evidence that does not show a real operating enterprise.

The pattern I see most often is a file built around conclusions instead of proof. A good E-2 package does more than recite the rule. It shows, document by document, how the founder meets it.

Mayo Law works with founders across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, which helps when an E-2 case overlaps with U.S. entity formation, Canadian ownership records, or cross-border structuring questions.

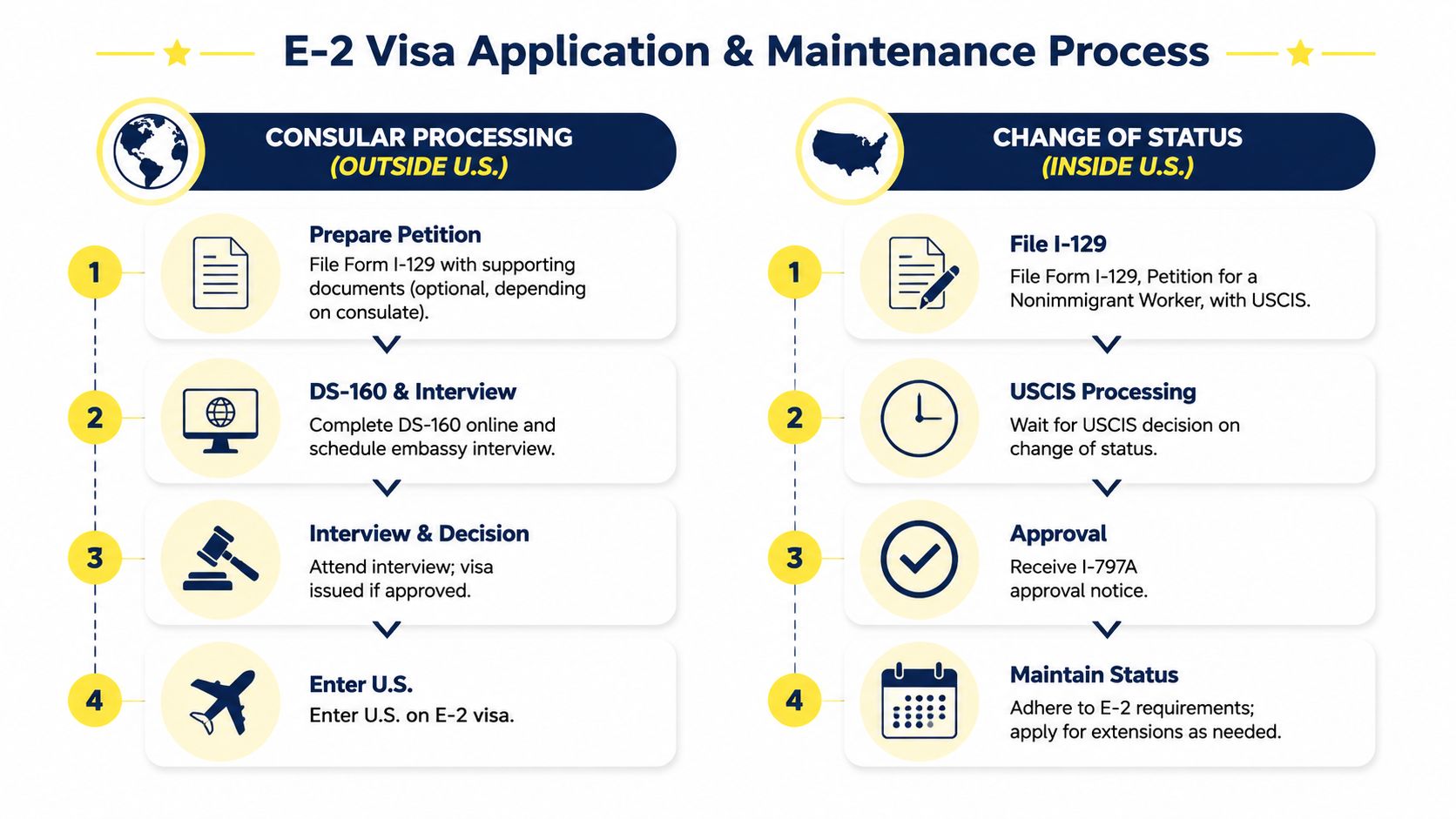

Filing Your Application and Maintaining Status

A founder in Toronto often reaches this stage with the company formed, funds committed, and customers lined up, then runs into a practical question. Do you apply through the consulate, or file inside the United States and deal with travel later? The answer affects timing, interview risk, and how much disruption a single trip can cause.

Consular processing versus change of status

| Path | Usually makes sense when | Main trade-off |

|---|---|---|

| Consular processing | You’re outside the U.S. or need a visa for travel | Requires consular scheduling and interview preparation |

| Change of status | You’re already in the U.S. in valid status | Approval gives status, not a visa stamp for reentry |

For many Canadian founders, consular processing is the cleaner route because it aligns status and travel documentation. If you expect frequent cross-border travel for fundraising, supplier meetings, or client work, having the visa issued through a consulate usually avoids a later scramble.

Change of status can still make sense. It is often used when the founder is already in the U.S. in valid status and needs to start operations without leaving first. The trade-off is practical, not technical. USCIS can approve E-2 status inside the U.S., but that approval does not function as a visa for future entry after international travel. Once you leave, you may need consular processing before you can return in E-2 classification.

That point causes real problems for startups. I often see founders plan a product launch, investor meeting, or family trip as if the status approval solved travel. It did not.

Filing strategy also affects how the evidence should be presented. A consular file usually needs to be organized for a post that reviews many E-2 cases and expects a clean package that proves the investment is already committed and the business is ready to operate. A USCIS filing often benefits from a record built more like a petition, with clear exhibit labeling, transaction tracing, and explanation of why the amount invested is substantial for this specific business model. As noted earlier, there is no fixed minimum investment, but lower investment amounts tend to receive closer scrutiny, especially if the startup has not yet shown meaningful operating activity.

What happens after E-2 visa approval?

Approval is the start of the compliance phase. The business now has to match the file you submitted.

Renewals are not automatic. Officers can review whether the company still meets the treaty nationality and control rules, whether it remains active and operating, whether the investment remains at risk, whether the business is more than marginal, and whether the applicant still fills an executive, supervisory, or essential role consistent with the original filing.

Renewal cases are often harder than first filings because there is now a record to examine. If the application projected hiring, contracts, and business activity, the renewal file should show payroll records, signed agreements, invoices, bank activity, tax records, and updated corporate documents that support that story.

For Canadian and other cross-border founders, ownership changes are a common maintenance problem. A financing round, share transfer, new parent company, or investor consent right can affect treaty nationality or control in ways that are easy to miss until renewal. The business may still be healthy and growing, but the E-2 analysis can weaken if the documents are not updated and reviewed as the cap table changes.

Good maintenance habits include:

- Keeping corporate records, minutes, and ownership ledgers current

- Tracking payroll, contracts, invoices, and operating expenses in a way that can be produced quickly

- Reviewing financings, SAFEs, notes, and equity grants for control issues before closing

- Preserving bank records and transfer documents for later proof of capital movement

- Comparing actual operations against the original business plan before a renewal filing

A well-prepared E-2 file gets you approved. A well-run paper trail keeps you approved.

Frequently Asked Questions

How much does an E-2 visa application cost?

Cost turns on where and how you file. Government fees differ for consular processing and USCIS filings, and fee schedules change. Check the current amounts before filing rather than relying on an older article or checklist. Legal fees also vary for a reason. A Canadian founder opening a new U.S. subsidiary with clean personal funding records is usually a different file from a case involving a share purchase, multiple owners, loans, or funds moving through several accounts.

Can my spouse and children come with me on an E-2 visa?

Yes, qualifying dependants can usually apply with you or follow later. The practical issue is document consistency. Marriage certificates, birth certificates, divorce records, and passports should align on names and dates. For Canada-U.S. cases, problems often start with small discrepancies such as a shortened middle name, a prior legal name, or civil records issued in different provinces at different times.

Can I travel outside the U.S. on an E-2 visa?

Usually, yes. The key distinction is between E-2 status inside the United States and an E-2 visa stamp used for admission at the border or airport. If you changed status with USCIS inside the U.S., that approval does not by itself let you re-enter after travel abroad. Canadian applicants often have a different travel pattern than applicants from other countries, but the status-versus-visa distinction still needs to be checked carefully before any trip.

What happens if my E-2 business fails?

If the business is no longer operating in a qualifying way, the E-2 case weakens quickly. Options may include a new filing based on a different enterprise, a change to another status category if one fits, or departure from the United States. Founders should assess this early, not after payroll has stopped and records are incomplete. In practice, the best risk control is conservative planning at the front end. Build the case around a business the company can fund and run.

Is buying an existing business better than starting one?

The better option is the one you can prove and operate cleanly.

An existing business can help because it already has revenue, staff, leases, vendor accounts, and tax history. That can make the marginality and real-and-operating issues easier to document. It also creates diligence risk. Buyers need to confirm what assets are being acquired, whether the seller's numbers are reliable, and whether the ownership structure after closing still supports treaty nationality and control.

A startup can work just as well, especially for service businesses and founder-led SMEs. The evidentiary burden is different. The file needs to show committed funds, a credible launch plan, signed contracts or active sales efforts where available, and a paper trail that makes commercial sense.

Mayo Law advises founders, investors, and SMEs on E-2 filings, renewals, ownership structuring, and source-of-funds issues across Canada and the United States.

How Mayo Law Can Help

An E-2 matter usually isn't just an immigration file. It often involves company setup, ownership analysis, source-of-funds tracing, and business-plan support. Mayo Law serves clients across Toronto, the GTA, and on cross-border matters. To discuss your matter, visit E-2 visa lawyer.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles