You incorporated your business in New York or Ontario. The certificate is filed, the name is set, and now someone asks for the bylaws. Many first-time founders pause here because incorporation feels concrete, while governance feels abstract.

At Mayo Law, our attorneys often see this moment in cross-border businesses. A founder is ready to sign contracts, open bank accounts, add investors, or appoint directors, but the company still lacks its internal rules. That gap matters.

If you’re asking what are bylaws of a company, the simplest answer is this. Bylaws are your corporation’s internal rulebook. They don’t create the company. They tell the company how to function after it exists. They set the rules for board decisions, meetings, officer roles, voting, and shareholder rights. If you’re still deciding on structure, this guide on choosing the right entity for your U.S. business may help frame the issue.

Introduction Your Company’s Rulebook

Founders often confuse bylaws with filing papers. They are different. Your formation filing creates the corporation in the eyes of the state or province. Your bylaws tell the people inside the corporation how to run it.

Think of bylaws as the house rules for ownership and management. If the corporation has directors, officers, and shareholders, bylaws answer practical questions such as who can call a meeting, how votes happen, what counts as enough attendance to act, and what happens if a director resigns.

Practical rule: Articles form the corporation. Bylaws govern the corporation.

This matters even more in cross-border businesses. A company that operates between New York and Ontario may have founders, investors, and managers in different places. Without clear internal rules, small misunderstandings can turn into stalled approvals, invalid meetings, or disputes about authority.

The Foundational Legal Role of Corporate Bylaws

A founder in Brooklyn approves a contract at a board meeting. A co-founder in Toronto later asks a simple question: was that meeting properly called, and did the board have authority to act? If the answer is buried in assumptions instead of written rules, the problem is no longer administrative. It is legal.

That is the foundational role of bylaws. They convert a corporation from a filing on paper into a working decision-making system. The certificate or articles create the entity. Bylaws tell the entity how to act through directors, officers, and shareholders in a way the law will recognize.

A practical comparison helps. Bylaws work like the operating rules for a building after the deed is recorded. Owning the building tells you who the property belongs to. The operating rules tell you who can open the doors, approve repairs, call meetings, and sign binding contracts.

Why bylaws matter as a legal document

Corporate law does not deal with a company as if it were a free-floating idea. It asks process questions. Who had authority? Was notice given? Was quorum present? Did the right group approve the action?

Bylaws answer those questions before a dispute starts.

That matters in ordinary business settings, not just lawsuits. A bank may ask for resolutions and officer authority. An investor may review governance records during diligence. A buyer may want confirmation that past approvals were valid. If the bylaws are thin, outdated, or inconsistent with actual practice, routine transactions slow down fast.

Common issues include:

- Board authority: which decisions require board approval and how that approval is recorded

- Meeting mechanics: who can call a meeting, how notice is delivered, and whether attendance by phone or video is allowed

- Voting rules: what counts as quorum and what vote threshold is needed to approve action

- Officer powers: which officers may sign contracts, certify records, or handle banking matters

- Shareholder process: when shareholders vote, how meetings are held, and what records they may inspect

The legal role is similar in New York and Ontario, but the framework is not identical

For cross-border startups, the differing expectations between jurisdictions often trip up founders. New York and Ontario both expect corporations to have internal governance rules. But they do not express those expectations in exactly the same way, and the default statutory rules are not identical.

Under New York’s Business Corporation Law, bylaws are a standard part of the corporation’s governance structure and interact closely with statutory rules on meetings, directors, officers, notice, quorum, and shareholder action. Under Ontario’s Business Corporations Act, bylaws also govern the corporation internally, but founders often encounter them alongside a stronger practical focus on director resolutions, shareholder resolutions, and the corporation’s articles. The result is that two corporations can look similar from the outside while relying on slightly different internal mechanics.

For a startup with New York investors and an Ontario parent, or the reverse, that difference matters. A founder may assume the same meeting practice, officer title, or amendment process works on both sides of the border. Sometimes it does. Sometimes it creates a governance gap that only appears during financing, a founder dispute, or a due diligence review.

What bylaws do in day-to-day governance

Bylaws usually set the recurring rules that no one wants to renegotiate every month. They often cover the size of the board, how vacancies are filled, what officers the corporation will appoint, how meetings are held, and how corporate records are maintained.

They also help separate governance from economics. Bylaws say how decisions get made inside the corporation. A shareholder agreement usually deals with owner-level bargains such as transfer restrictions, buy-sell rights, or veto rights. If your startup also has multiple founders or early investors, a shareholders agreement with clauses that prevent founder wars often works alongside the bylaws rather than replacing them.

Good bylaws reduce friction because they replace memory and custom with a rule set people can follow. That is especially useful when the team grows, crosses borders, or stops operating as an informal founder group.

A practical founder takeaway

In New York and Ontario alike, bylaws are evidence of disciplined corporate action. They help show that the corporation acts through proper approvals rather than through whoever spoke first on a call.

That distinction becomes important when money, control, or liability is on the line.

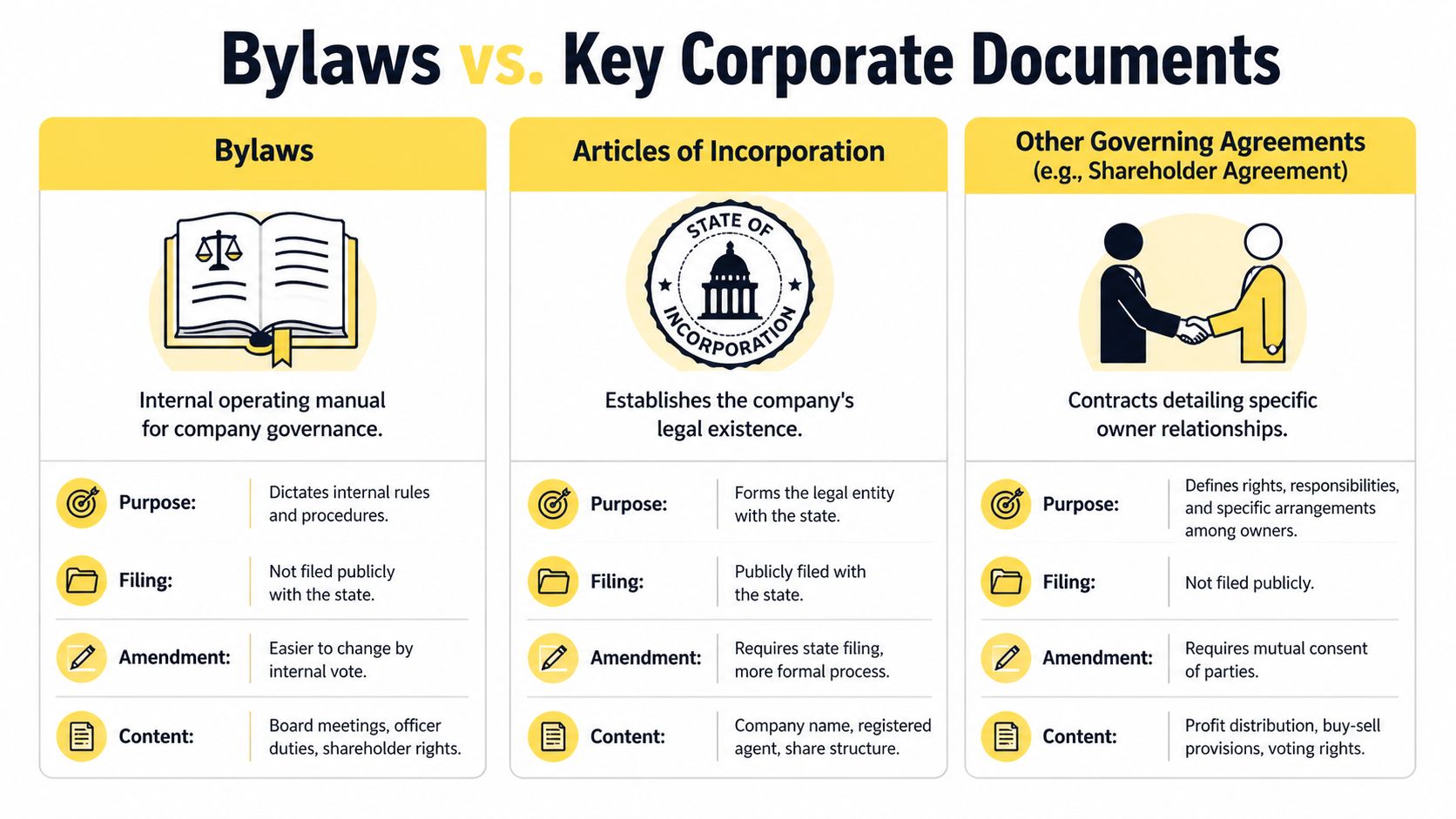

Bylaws vs Other Key Corporate Documents

Founders rarely struggle with the idea of a company rulebook. They struggle with which document does what. That confusion gets expensive when one document says one thing and another says the opposite.

Articles of incorporation

Articles of incorporation are the public filing that creates the corporation. In New York, that filing goes to the state. In Ontario, the incorporation filing creates the legal entity under the applicable corporate statute.

Bylaws are different. They are usually internal. You don’t use them to create the corporation. You use them to govern the corporation after formation.

A simple comparison helps:

| Document | Main job | Public or internal | Typical content |

|---|---|---|---|

| Articles of incorporation | Creates the corporation | Public filing | Name, share structure, registered office, basic formation details |

| Bylaws | Runs the corporation internally | Internal document | Meetings, board process, officer roles, voting rules |

Shareholder agreements

A shareholder agreement is a contract among shareholders, and sometimes the corporation too. It often covers issues that go beyond basic governance, such as transfer restrictions, exit rights, buy-sell mechanics, founder vesting, or deadlock planning.

Bylaws still matter because they apply to the corporation’s internal process. But a shareholder agreement may set more customized rights among owners. In growth companies, the two documents need to fit together. If they conflict, fights tend to follow. This discussion of shareholders agreements and clauses that prevent founder wars gives a good example of where those tensions start.

If your bylaws say one voting rule and your shareholder agreement says another, the problem isn’t academic. It affects whether a decision stands.

Operating agreements

Operating agreements belong to LLCs, not corporations. New York founders sometimes mix these terms because many U.S. businesses use LLCs. A corporation uses bylaws. An LLC uses an operating agreement.

Ontario founders may run into a similar issue when comparing U.S. and Canadian structures. The document name changes with the entity type. The function is similar in one sense. Each document sets internal rules. But the legal framework is different, and the wrong template can cause real confusion.

Where cross-border founders get tripped up

A New York corporation with Ontario stakeholders may end up with all of these documents in play:

- Articles that create the corporation

- Bylaws that manage governance

- Shareholder agreement that allocates owner rights

- Subscription or stock purchase documents for investment rounds

That’s normal. The key is consistency. If one document gives a founder a board seat, another shouldn’t undermine it through meeting or voting mechanics.

Core Provisions Every Company Bylaw Should Contain

A founder forms a New York corporation, adds an Ontario co-founder, closes a small friends-and-family round, and then needs board approval for a bank mandate and new share issuance. Everyone agrees on the business decision. The dispute starts over mechanics. Who had authority to call the meeting? How many directors had to attend? Could one director join by video from Toronto? Good bylaws answer those questions before a routine approval turns into a governance problem.

The easiest way to read bylaws is as the company’s operating rulebook for recurring decisions. In New York, those rules sit under the Business Corporation Law. In Ontario, they sit under the Ontario Business Corporations Act. The statutes are not identical, but they ask many of the same practical questions: who decides, how they decide, and what makes the decision valid.

Board of directors

Start with the board because the board carries the corporation’s decision-making authority between shareholder votes. Your bylaws should state the number of directors or the range allowed, how directors are elected, their term of office, and how the company fills vacancies.

This matters more than founders often expect. A three-director board works differently from a five-director board. So does a board where one seat is tied to an investor right. In both New York and Ontario, the bylaw should match the company’s real governance plan, not a generic template copied from formation day.

For cross-border startups, pay attention to whether the bylaw gives flexibility to change board size later. Early-stage companies often add an investor nominee or an independent director long before they rewrite their governance documents.

Officers and their duties

Officers run the company’s day-to-day business. The bylaws usually name the officer roles, explain how officers are appointed and removed, and describe what authority comes with each office.

Common roles include:

- President or CEO: leads operations and often signs major contracts

- Secretary: keeps minutes, maintains records, and handles formal notices

- Treasurer or finance officer: oversees financial administration and reporting

Titles can mislead. A person called “Chief Operating Officer” may have broad business responsibility, but the bylaw should still say whether that person can sign borrowing documents, certify resolutions, or bind the corporation in routine transactions.

That point often matters in cross-border banking and financing. A New York lender or Ontario investor will often ask for proof that the person signing had authority under the company’s internal rules.

Shareholder meetings

Shareholder meeting provisions set the ground rules for owner decisions. The bylaws should cover annual meetings, special meetings, notice requirements, record dates, voting procedures, and whether action can be taken by written consent or written resolution if the governing law allows it.

Founders sometimes treat these clauses as formality because the shareholder group is small. Later, during due diligence, those details become very real. Buyers, investors, and counsel often check whether share issuances, director elections, and major approvals were properly authorized.

New York and Ontario corporations often use similar concepts here, but the drafting should reflect the statute that applies to the company. A bylaw borrowed from the wrong jurisdiction can create confusion about who may call a meeting or what notice period applies.

Director meetings, quorum, and voting

This section does a lot of the heavy lifting. Board decisions are only as reliable as the meeting rules behind them.

Your bylaws should answer at least four questions:

- What is quorum for a directors’ meeting?

- Can directors participate by telephone or other electronic means?

- What vote is needed for ordinary board action?

- Do certain matters require a higher approval threshold?

Quorum is the minimum number of directors who must participate before the board can act. A simple way to view it is the board’s minimum attendance line. If the bylaw is vague, the company can end up debating whether a meeting produced a valid approval at all.

A board can discuss business without quorum. It usually cannot take binding corporate action without it.

For a cross-border startup, remote participation language matters too. Directors are often split between New York and Ontario, and the bylaw should clearly permit virtual attendance if the applicable law permits it. That avoids procedural arguments over whether a director who joined electronically counted toward quorum or voting totals.

Share issuance and transfers

Bylaws often address the mechanics of issuing shares, maintaining the securities register, replacing certificates if the company uses them, and recording transfers. These provisions should fit with the company’s cap table process and with any separate investor or founder agreements.

This is a common friction point in growth companies. The bylaw may describe how the corporation records a transfer, while a shareholder agreement limits when that transfer is allowed. Both rules can coexist, but they need to line up. For example, a right of first offer on share sales may sit in a separate agreement, while the bylaws explain the internal steps the company follows once a transfer is approved.

New York and Ontario corporations both need clear internal procedures here. The exact terminology may differ, but the business question is the same: who can transfer shares, on what conditions, and how does the company record the change?

Indemnification and records

Bylaws often include indemnification provisions for directors and officers. In plain English, those clauses say when the corporation may reimburse or protect decision-makers who face claims because of their corporate role, subject to the limits of applicable law.

The bylaws should also set expectations for records. Minutes, resolutions, registers, and notices are the company’s memory. If a dispute arises two years later, the corporation usually wins or loses credibility based on whether it can produce a clean record of what happened and who approved it.

That is especially true for companies operating across New York and Ontario. Cross-border teams tend to make decisions by email, messaging apps, and quick video calls. Good bylaws do not prevent that pace. They turn those decisions into a process the company can prove later.

The Process of Adopting and Amending Bylaws

Bylaws usually begin life shortly after the corporation is formed. The incorporator or the initial board adopts them at the organizational stage. That first set of governance decisions often includes appointing directors or officers, approving banking arrangements, and authorizing share issuance.

For founders, this is the point where the company shifts from “formed on paper” to “ready to operate.” If you’re still working through early setup, this Ontario incorporation checklist covering steps, costs, and timelines can help place bylaws in the larger formation process.

Adoption

The adoption step should be documented. The corporation should keep the bylaws with its minute book or records book, along with the resolutions or minutes showing they were approved.

That internal record matters because bylaws are meant to be followed, not just drafted. If a dispute later arises, people usually look for proof that the corporation adopted the document and acted under it.

Amendment

Good bylaws also explain how they can be changed. Such changes often cause difficulties for growth companies. The bylaws should say who may amend them, the required vote, and whether some provisions need stronger approval than others.

A solid amendment clause often addresses:

- Who has authority: board, shareholders, or both

- What vote is needed: simple majority or a higher threshold

- Whether notice is required: especially if the amendment affects control or voting

- When the change becomes effective: immediately or after another approval step

If your bylaws contain an amendment procedure, follow it exactly. Informal shortcuts often create formal problems later.

In cross-border businesses, amendment discipline matters even more. When stakeholders are spread across jurisdictions, assumptions about what was “agreed” can drift quickly unless the corporate record is clear.

Common Pitfalls and Cross-Border Compliance

A common cross-border startup story goes like this. The founders incorporate in Ontario, open a sales office in New York, bring in a U.S. investor, and keep using the short bylaws they approved at formation. Nothing seems wrong until a board seat is disputed, a meeting notice is challenged, or a financing document points one way while the bylaws point another.

By then, the issue is rarely academic. It affects who can approve actions, whether past decisions were made properly, and how expensive the cleanup will be.

Weak amendment and dispute clauses

One recurring problem is vague amendment language. Early-stage founders often write bylaws for a friendly two-person company. Later, those same bylaws must govern investor rights, board appointments, and consent mechanics under pressure.

Dispute provisions are often thin as well. If the bylaws say little about how internal conflicts are handled, the company is left arguing about process before it can address the actual disagreement. That becomes more difficult when the corporation also has a shareholders’ agreement or financing documents, such as a stock purchase agreement used in an equity financing, that assign approval rights differently.

The practical rule is simple. If one document gives the board power and another gives a veto right to shareholders or a particular investor, the conflict needs to be resolved on paper before it becomes a live dispute.

Governance traps that slow companies down

Some bylaw problems do not look dramatic, but they can stall a company just as quickly.

- Quorum rules that are too rigid: A board cannot act if the bylaws require attendance levels that are unrealistic once directors are in different cities or countries.

- Meeting rules written for in-person governance: If the bylaws do not clearly support remote participation, notice, and written consents where permitted, routine approvals can become procedural fights.

- Outgrown governance terms: A bylaw set written for two founders may stop making sense after outside investment, an independent director, or a U.S. subsidiary is added.

- Document conflicts: Bylaws, unanimous shareholder agreements if used, board resolutions, and share issuance documents should fit together like one operating manual.

Bylaws work like the company’s internal traffic rules. If the signals are unclear, people do not stop driving. They start colliding.

New York and Ontario issues

Cross-border founders often make avoidable mistakes. New York and Ontario both allow corporations to adopt bylaws that govern meetings, directors, officers, and internal procedure. But the governing statute is not interchangeable. A New York corporation is primarily governed by the New York Business Corporation Law. An Ontario corporation is governed by the Ontario Business Corporations Act.

That sounds obvious, yet founders regularly borrow forms across the border without adjusting them.

Here are the questions that usually matter first:

| Question | Why it matters |

|---|---|

| Where is the corporation incorporated? | The home statute usually decides what the bylaws can say and how conflicts are resolved |

| Is there a unanimous shareholder agreement in Ontario, or investor side rights in New York? | Those arrangements can shift powers away from directors or create approval rights that the bylaws must respect |

| How will directors meet and approve actions? | Remote attendance, written resolutions, and notice mechanics should match the governing law and actual practice |

| Who is signing off on financings or share issuances? | Approval steps in the bylaws should line up with board authority, shareholder rights, and offering documents |

A useful way to frame the difference is this. New York and Ontario both treat bylaws as internal governance rules, but Ontario founders must be especially alert to whether shareholder arrangements reallocate powers that would otherwise sit with the board. New York founders, by contrast, often run into trouble when they assume investor expectations or operating habits can override formal corporate procedure without corresponding bylaw support.

The safest approach is to draft bylaws under the corporation's home law, then test them against the way the business will operate across the border. If the company lives in both markets, the paperwork should anticipate that reality instead of pretending the second jurisdiction is just a sales territory.

Key Considerations for Drafting Your Bylaws

When founders ask what are bylaws of a company, they usually want more than a definition. They want to know whether their current document is usable. These questions help test that.

Questions worth asking early

- Does the board structure match the business you have? A two-founder company and an investor-backed company need different governance mechanics.

- Are quorum and voting rules workable in real life? A rule that looks protective on paper can create deadlock in practice.

- Do the bylaws fit your shareholder agreement? If the documents clash, the conflict usually surfaces at the worst time.

- Is the amendment process clear enough to follow under stress? A vague process invites procedural fights.

- Have you addressed vacancies, resignations, and tied votes? These are ordinary events, not edge cases.

- Will the document still make sense after a financing or cross-border expansion? Bylaws should support growth, not lag behind it.

A founder’s practical checklist

Keep your review focused on a few business realities:

-

Ownership changes

New investors often change governance expectations. -

Board operations

Remote meetings, scheduling, and approval speed matter more than founders expect. -

Document harmony

Check bylaws against subscription documents, share terms, and any stock purchase materials, including a stock purchase agreement.

Bylaws are not exciting. But they are one of the documents most likely to matter when the company faces pressure.

If your business operates in Ontario, New York, or both, Mayo Law advises startups and SMEs on bylaws, shareholder agreements, governance disputes, and cross-border structuring. If you need help aligning your corporate documents with your growth plans, you can schedule a consultation with Mayo Law.

LEGAL DISCLAIMER: The information provided in this article is for general informational and educational purposes only and does not constitute legal advice. Reading this article, visiting mayo.law, or contacting Mayo Law does not create an attorney-client relationship. The content of this article should not be relied upon as a substitute for professional legal counsel specific to your particular circumstances. Legal outcomes depend on the particular facts and circumstances of each individual case, and no attorney can guarantee a specific result. Laws, regulations, and legal procedures are subject to change and may vary by jurisdiction. If you require legal assistance, you should consult with a qualified attorney licensed to practice in the relevant jurisdiction. Mayo Law expressly disclaims any and all liability with respect to actions taken or not taken based on the contents of this article.