Published: June 10, 2026

Updated: June 10, 2026

Read time: 11 minutes

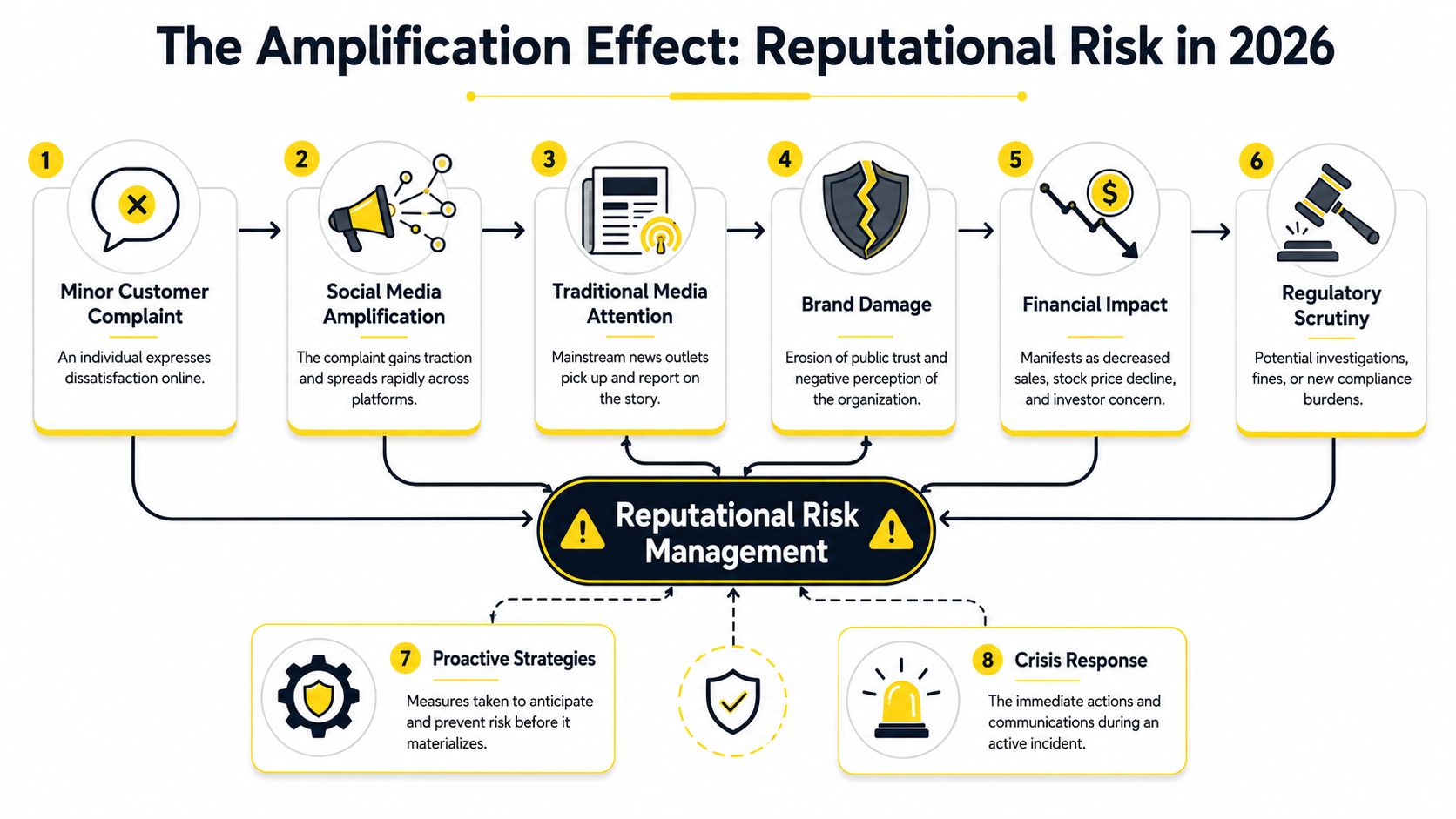

A reputational problem rarely starts looking important. It starts as a customer post, a supplier allegation, a privacy complaint, or an employee screenshot that lands in the wrong Slack channel and then on the right social feed. For U.S.-Canada companies, the problem gets harder fast because legal exposure, disclosure expectations, and stakeholder pressure often move across both markets at once.

At Mayo Law, we help businesses in Toronto, the GTA, and across the border manage compliance and governance problems that can quickly become public problems, with experience licensed in both Ontario and New York on a process that often spans both sides of the border. If your leadership team still treats reputational risk management as a media issue, you are already behind. It is a governance issue, an operational issue, and in the wrong fact pattern, a securities, regulatory, employment, or white-collar issue.

Defining Reputational Risk Management in 2026

Reputational risk management is the process of identifying, assessing, monitoring, and responding to threats that can damage an organization's credibility, stakeholder trust, and brand standing. In practice, it sits inside enterprise risk management, not outside it. The job is not solely to protect image. The job is to reduce the gap between what the company says, what it does, and what stakeholders discover under pressure.

A board should treat this as a control function. Marketing can support it. Communications can execute parts of it. But neither should own it alone.

Why boards now own this issue

The old model was reactive. A problem became public, PR drafted talking points, legal reviewed them, and management hoped the story died. That approach fails when the underlying issue is operational, repeated, or documented.

Aon's 2025 Global Risk Management Survey ranks damage to reputation or brand as the 8th-largest global risk today and projects it to fall to 19th by 2028, while tying that shift to broader categories such as cyber threats, ESG scrutiny, and social-media amplification in enterprise strategy and crisis planning (Aon's 2025 Global Risk Management Survey). That projected drop does not mean reputation matters less. It means the risk has been absorbed into other board-level exposures.

That distinction matters for directors. If reputation is embedded in cyber, supply chain, labor, conduct, and disclosure, then the board can't delegate it downward and call it handled.

Practical rule: If a problem can trigger litigation, regulator interest, customer loss, or board reporting, it belongs in the risk register before it belongs in a press release.

What works and what does not

What works is structured ownership. One executive should coordinate risk intake, legal should define escalation triggers, and the board should receive regular reporting on emerging issues, not just headline incidents. Companies also need written links between complaints, investigations, vendor oversight, and crisis response.

What does not work is “brand monitoring” without authority. If the team watching sentiment cannot trigger legal review, preserve evidence, or escalate facts to management, you do not have reputational risk management. You have a listening tool.

The same is true when companies confuse policy volume with control quality. A thick code of conduct will not save a company that has poor reporting lines, unclear incident ownership, or no threshold for escalation. That is why many boards now fold reputation into broader compliance officer responsibilities rather than isolating it as a communications topic.

What is reputational risk management

It is the discipline of spotting trust threats early, assigning ownership, validating facts quickly, and containing legal, operational, and stakeholder fallout before the issue defines the company for you.

The High Stakes of Reputational Damage in the U.S. and Canada

A reputational event becomes legally serious when it changes what the company must disclose, investigate, preserve, or remediate. That is where many boards misjudge the risk. They focus on whether the story is fair. Regulators and plaintiffs' counsel focus on whether the company's controls, statements, and response were adequate.

In the United States, public issuers should assess whether a reputational event connects to risk factor disclosure, management discussion, cyber disclosure, internal controls, or prior public statements. The governing sources are not “reputation rules” in isolation. They are the disclosure framework and anti-misleading statement rules that can pull reputation into securities exposure. For reference, boards and executives should review the SEC's Regulation S-K risk factor requirements and the SEC's cybersecurity disclosure guidance and rules.

In Canada, the analysis is similar in substance even if the paperwork differs. Reporting issuers should assess whether an incident changes material risk disclosure, continuous disclosure obligations, prior public statements, or governance representations. Directors should review the Canadian Securities Administrators' continuous disclosure guidance alongside company-specific disclosure controls.

U.S. vs. Canada reputational risk disclosure at a glance

| Aspect | United States (SEC Guidance) | Canada (CSA Guidance) |

|---|---|---|

| Risk factor disclosure | Considers whether reputation-linked issues are material business risks requiring discussion under Regulation S-K | Considers whether material business risks should be reflected in continuous disclosure documents |

| Prior statements | Reviews whether earlier statements are now incomplete or misleading in light of new facts | Reviews whether earlier disclosure remains accurate and not misleading |

| Governance lens | Focus on disclosure controls, escalation, board oversight, and management certifications | Focus on governance processes, materiality assessment, and continuous disclosure controls |

| Incident overlap | Reputational issues often overlap with cyber, misconduct, supply chain, or internal control failures | Reputational issues often overlap with operational, conduct, disclosure, or governance failures |

| Board implication | Directors should ask who knew what, when, and how escalation occurred | Directors should ask the same, with attention to materiality and disclosure timing |

Why this reaches fiduciary judgment

Directors do not need to chase every social flare-up. They do need a defensible process for deciding when a reputational issue is material enough to reach the board, external counsel, insurers, auditors, or regulators.

That means documenting decisions. If management decides not to escalate, there should be a reasoned record. If the company speaks publicly, legal should test whether the statement can be supported with known facts. If the event involves fraud, books and records issues, data handling, sanctions, or employee misconduct, the matter can also move quickly into the territory where white-collar crimes defense concerns become relevant.

A board's exposure usually comes less from the bad event itself and more from weak oversight, delayed escalation, or inaccurate public assurances.

A common cross-border mistake

A U.S. parent and Canadian subsidiary often assume one statement will work for both markets. It may not. The underlying facts may be shared, but employment law, privacy obligations, reporting lines, and regulator expectations can differ. Companies should prepare one fact base and then adapt the legal analysis by jurisdiction.

A Framework for Identifying Your Core Reputational Risks

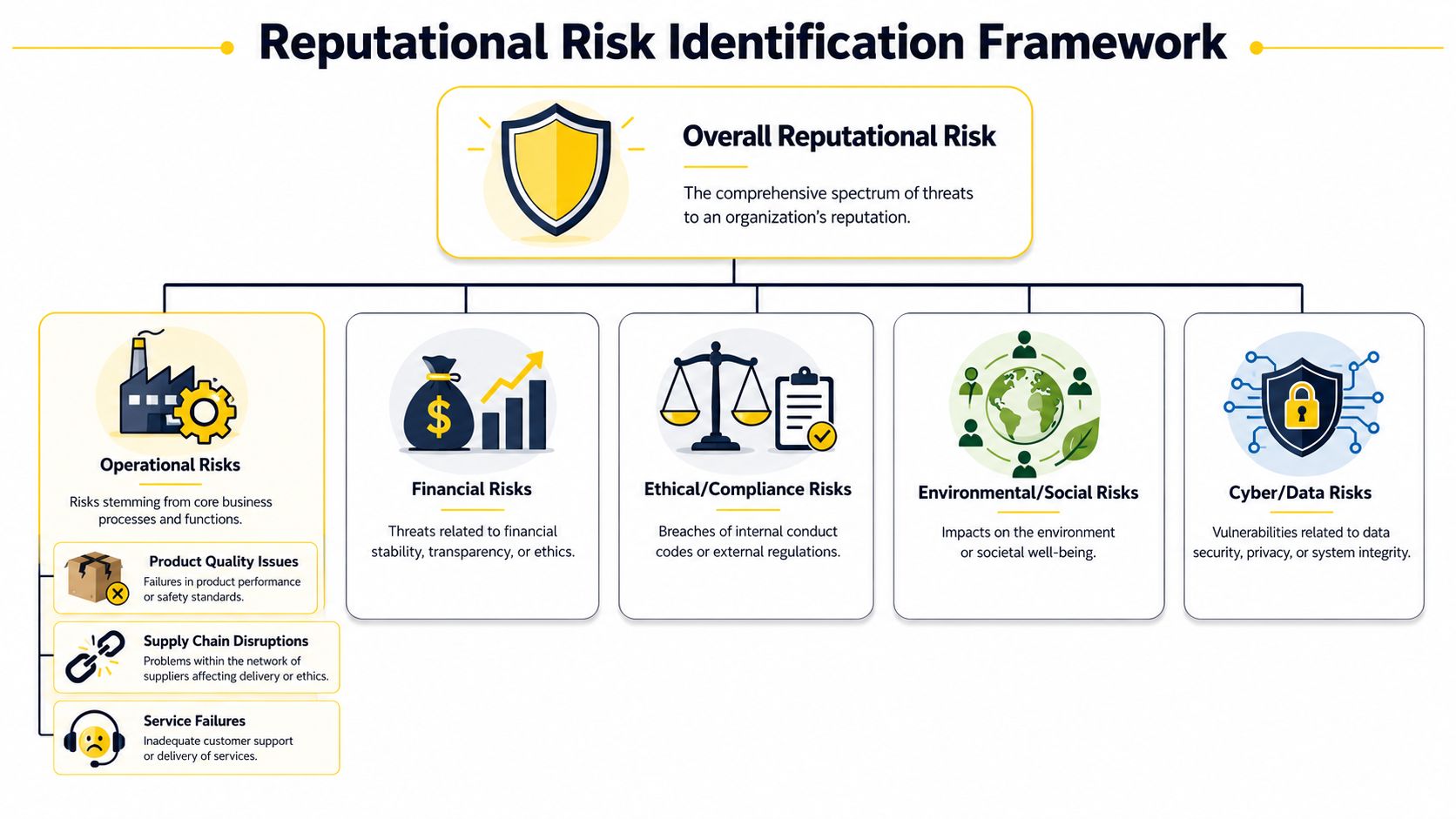

Most companies identify reputational risk too broadly to manage it. “Anything that could hurt the brand” sounds sensible, but it gives management no priority and no control design. A usable framework starts by asking where trust can break in your specific business model.

What are the most common sources of reputational risk

They usually fall into five categories:

- Operational failure: Product defects, service breakdowns, delivery failures, recalls, billing errors.

- Conduct and ethics: Harassment, retaliation, bribery concerns, conflicts of interest, false claims.

- Third-party contagion: Vendor misconduct, distributor behavior, supplier labor issues, contractor access failures.

- Cyber and data events: Security incidents, privacy complaints, ransomware, unauthorized access.

- Public narrative failures: Misleading statements, inconsistent messaging, mishandled investigations, slow correction of false information.

Boards should abandon the misconception that reputation is primarily an internal concern. Reputational harm is often transmitted through third parties. Mitratech's guidance recommends independent risk assessments of vendors completed within the past 12 months, annual reassessments, and continuous monitoring of adverse media and regulatory changes (Mitratech on reputational risk management). That is a network-risk model, not a branding model.

A practical assessment method

Start with your promises. What do customers, employees, investors, and regulators believe your company does well or safeguards carefully? Those promise points are your reputational fault lines.

Then map each promise against failure modes:

- List critical trust claims. “We protect data.” “We source responsibly.” “We comply across borders.”

- Match each claim to a control owner. Someone must own testing, evidence, and escalation.

- Identify the fastest path to public exposure. Employee post, regulator letter, customer complaint, leak, vendor issue.

- Score detectability. Can you spot the issue early, or only after it becomes public?

- Test response readiness. Can legal, operations, HR, and communications align quickly?

Two scenarios boards should recognize

A SaaS company relies on a cloud-based vendor for a customer-facing function. The vendor has broad system access. The company's own controls look clean, but the vendor suffers a breach and customers blame the SaaS company, not the vendor. The reputational issue is not just cybersecurity. It is vendor diligence, contract allocation, notification readiness, and accuracy of prior privacy statements.

A manufacturer promotes ethical sourcing but delegates supplier onboarding to procurement with limited legal review. Adverse media later reports poor labor practices in a second-tier supplier. The board may feel blindsided, but the weakness usually appeared earlier in due diligence design, audit rights, subcontractor visibility, and escalation gaps.

Board question: Which outside party could damage our reputation tomorrow, and what current evidence do we have that the risk is being monitored?

What boards often miss

They underweight intellectual property and information misuse. A former employee, channel partner, or contractor can create a reputational event by taking confidential information, posting internal materials, or alleging wrongdoing around disputed know-how. In cross-border businesses, that often overlaps with contract enforcement and trade secret misappropriation risk.

A good risk inventory is not exhaustive. It is decision-ready. If the list is too long to govern, management will ignore it until the next crisis.

Proactive Mitigation Through Strong Corporate Governance

The most effective reputational risk management program is boring by design. It relies on routine controls, clear reporting, and disciplined ownership. Companies that perform well in a crisis usually looked somewhat overprepared the month before.

A governance model directors can actually use

The OECD describes a reputational risk maturity model with four levels: Emerging, Progressing, Established, and Leading, and ties weak controls, fragmented reporting, and poor transparency to greater exposure, while continuous monitoring and clear accountability reduce it (OECD analysis on enhancing reputational risk management).

That model is useful because it gives boards a way to benchmark design quality without pretending every company needs the same architecture.

A practical board discussion sounds like this:

- Emerging: Issues are handled ad hoc. Ownership is unclear.

- Progressing: Policies exist, but escalation is inconsistent.

- Established: Reputation sits in ERM, with defined reporting and incident protocols.

- Leading: The company uses early-warning indicators, cross-functional testing, and board-level review.

The controls that matter most

Some controls are worth more than others. These are the ones I would press first.

- One accountable executive owner: Not shared ownership. Shared ownership often means no ownership.

- Board visibility: Regular reporting on trends, not just major incidents.

- Escalation triggers: Written thresholds for legal review, disclosure analysis, and crisis activation.

- Cross-border alignment: U.S. and Canadian teams should work from one incident fact base.

- Tabletop exercises: Test product, cyber, employee, and vendor scenarios.

- Evidence preservation: Keep records early, before narratives harden.

Weak companies usually miss one of two things. Either they have no escalation threshold, or they escalate everything and create noise. The answer is to define materiality indicators in plain language. Could this affect customers, regulators, counterparties, or prior public statements? If yes, legal should see it.

Governance is also structural

Some reputational failures start in basic company housekeeping. If authority lines are ambiguous, if officers are acting outside documented authority, or if board committees are unclear on reporting chains, the company creates avoidable credibility risk. Basic governance documents matter more than founders often think, including what are bylaws of a company and whether actual practice still matches them.

Mayo Law works with companies across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, so clients with U.S. ties coordinate legal work in one place rather than splitting governance, compliance, and incident response between separate firms.

What good prevention looks like in practice

A good program does not promise that no one will complain, leak, accuse, or misstate. It makes the company faster at answering three questions:

- What happened.

- Who needs to know.

- What must be done now to limit legal and commercial damage.

Good governance shortens the distance between fact discovery and responsible action.

If your board packet discusses strategy, cyber, human capital, and regulatory change but never addresses trust risk directly, the governance design is incomplete.

Building a Cross-Border Crisis Response Playbook

When a reputational incident goes live, speed matters, but uncontrolled speed makes the record worse. Companies need a prebuilt playbook because social media, AI-generated content, and misinformation can outrun internal verification.

The World Economic Forum's 2025 Global Risks Report identifies misinformation and disinformation among the top short-term global risks, and the same body of reporting notes that heavy social-platform news discovery increases the speed at which false narratives spread before facts are verified (SecurityScorecard summary of these risk trends). That is why old crisis manuals that focus mainly on messaging are no longer enough.

How do you respond to a reputational crisis

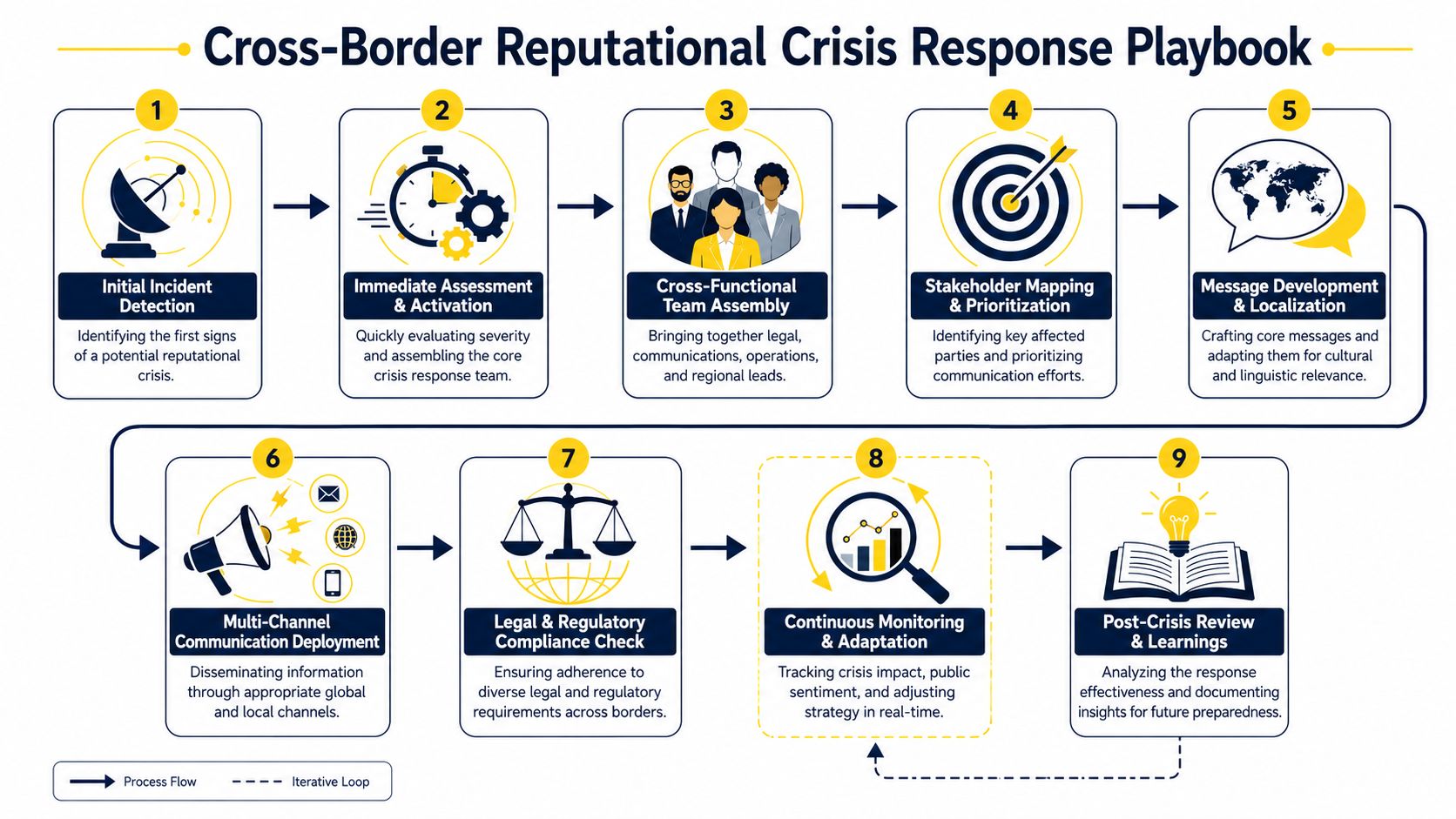

Use a sequence, not improvisation.

- Detect and classify the incident. Is the issue operational, legal, cyber, conduct-related, or false but viral?

- Activate the right team. Legal, communications, HR, operations, security, and local market leads.

- Freeze the facts. Preserve emails, chats, logs, screenshots, contracts, and decision records.

- Validate before speaking. Confirm what is known, unknown, and unverifiable.

- Map stakeholders. Customers, employees, regulators, lenders, counterparties, insurers, investors.

- Localize the response. One factual core, jurisdiction-specific legal review.

- Monitor narrative drift. Track whether the issue is evolving into a different allegation.

- Review and remediate. After the first wave, fix the control weakness.

A cross-border example

A consumer product company learns that a product distributed in both countries may have a safety defect. A social post in one market starts the fire. Retail partners in the other market begin asking questions before the internal investigation is complete.

The wrong move is to let country teams issue separate explanations based on incomplete facts. That creates inconsistency, screenshots, and credibility loss.

The better move is to stand up a shared incident room, assign one legal lead, one operations lead, and one communications coordinator, then issue holding statements that are accurate but narrow. If a recall, notice, regulator communication, or customer remediation becomes necessary, the company can adapt execution by market while preserving one fact record.

The legal pieces companies skip

Boards often remember media strategy and forget evidence. That is a mistake. If litigation, employment claims, regulatory review, or insurer notice may follow, preservation starts immediately.

Your playbook should also address:

- Privilege planning: Decide early what goes through counsel.

- Regulator pathways: Identify who assesses whether notice obligations apply.

- Third-party coordination: Vendors, distributors, and insurers must be contacted in a controlled sequence.

- AI-content protocol: Define how manipulated audio, fake screenshots, or synthetic statements are authenticated and rebutted.

- Cross-border customer messaging: Keep factual consistency even where legal wording differs.

For companies entering or operating across both markets, incident planning often sits alongside broader international business lawyer support because contract structure, market-entry design, and reporting lines affect what can be done quickly in a crisis.

In a live incident, the first goal is not to sound polished. It is to avoid saying something inaccurate that creates a second crisis.

Can you rely on a generic crisis template

Usually not. Templates help with checklists. They fail when they do not reflect your actual org chart, vendor structure, reporting obligations, and approval chain. A playbook should be tested against your real business, not an imagined one.

Frequently Asked Questions

Does reputational risk management belong with legal, compliance, or communications

It belongs to all three, but ownership should be clear. Legal usually defines escalation, privilege, disclosure risk, and preservation. Compliance addresses control design and monitoring. Communications manages outward messaging. The mistake is giving one function sole ownership. The better approach is one accountable executive owner with board visibility and written roles for each function.

Is reputational damage insurable

Sometimes parts of the underlying event are insurable, but companies should not assume “reputation” itself is covered in any broad way. Coverage questions usually depend on the triggering event, such as cyber, D&O, employment practices, crime, or product liability. Boards should review policy language, notice requirements, exclusions, and how public statements might affect coverage positions.

How often should a board review reputational risk

At minimum, it should appear in regular risk reporting, not only after a public incident. Boards should also review it when the company enters a new market, changes core vendors, faces a cyber event, updates public claims, or experiences an internal conduct issue. Frequency matters less than discipline. The board needs a recurring forum and clear escalation triggers.

What is the first step if our company has no formal program

Start with a risk inventory tied to your business promises and your main stakeholder groups. Then assign one executive owner, define escalation triggers, and test a single crisis scenario. Most companies do not need a complex framework on day one. They need clarity on who decides, who investigates, and who speaks when pressure arrives.

Who should approve public statements during a reputational event

Approval should be small and fast. In most companies, that means legal, the incident owner, communications, and one senior executive. Public companies may also need disclosure counsel and board involvement depending on materiality. Avoid broad comment chains. They slow decisions and increase the risk of inconsistent language that later becomes evidence.

Does this apply to private companies or only public issuers

It applies to both. Public companies face more formal disclosure analysis, but private companies face lender scrutiny, customer loss, employee attrition, investor concern, and regulator attention. In practice, private companies can be more exposed because they often have weaker reporting lines and less tested crisis procedures. The governance discipline is similar even when securities rules differ.

If your company operates across the U.S. and Canada, reputational risk management should be built into governance before the next incident tests it. Mayo Law advises on cross-border compliance, governance, investigations, and response planning for businesses that need one coordinated legal view across both markets.

How Mayo Law Can Help

Cross-border reputational issues rarely stay in one lane. They can involve governance, disclosure, internal investigations, employment concerns, vendor disputes, and regulator contact at the same time. Mayo Law serves clients across Toronto, the GTA, and on cross-border matters, including compliance planning and incident response support through its compliance counsel services. To discuss your matter, visit Mayo Law.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

![Yellow decorative banner with a maple leaf and city skyline; title reads 'Employment Immigration Attorney Guide for US-Canada Business'.] ,](https://mayo.law/wp-content/uploads/2026/06/employment-immigration-attorney-business-guide-1024x569.jpg "employment-immigration-attorney-business-guide - Mayo Law")