Published: June 20, 2026

Updated: June 20, 2026

Read time: 11 minutes

Your first term sheet lands in your inbox. You expected to focus on valuation, board seats, and closing timing. Instead, one line keeps pulling your attention back: the round will involve dilution, plus an employee option pool increase. You still own your shares, so why does this feel like you’re giving something up?

That reaction is normal. But for founders, what does it mean in real life? Will you still control the company? What happens if you raise again? How do SAFEs, notes, and option pools change the math? And if your company touches both Canada and the United States, which documents protect you?

At Mayo Law, we help founders in New York, Toronto, the GTA, and across the border handle business issues that don’t stay neatly in one jurisdiction. Equity dilution often looks simple at first. In practice, it sits at the center of financing strategy, shareholder rights, and future control.

Introduction

If you’re asking what is equity dilution, you’re probably trying to decide whether a financing offer is fair, whether a SAFE is going to surprise you later, and whether the documents in front of you match the business deal you thought you made.

That’s the right instinct. Dilution affects ownership percentage, voting power, exit economics, and bargaining strength in the next round. A founder can build a more valuable company and still own a smaller slice of it over time. Both things can be true at once.

The legal risk is that many founders only review the headline number. They don’t look closely at the cap table definitions, the option pool mechanics, the conversion language, or the rights different holders get after the round closes.

Practical rule: never assess dilution from the term sheet alone. You need the cap table, the financing documents, and the shareholder rights package together.

A clean explanation starts with one point: dilution is mostly about percentage ownership. Once that clicks, the rest of the conversation becomes easier.

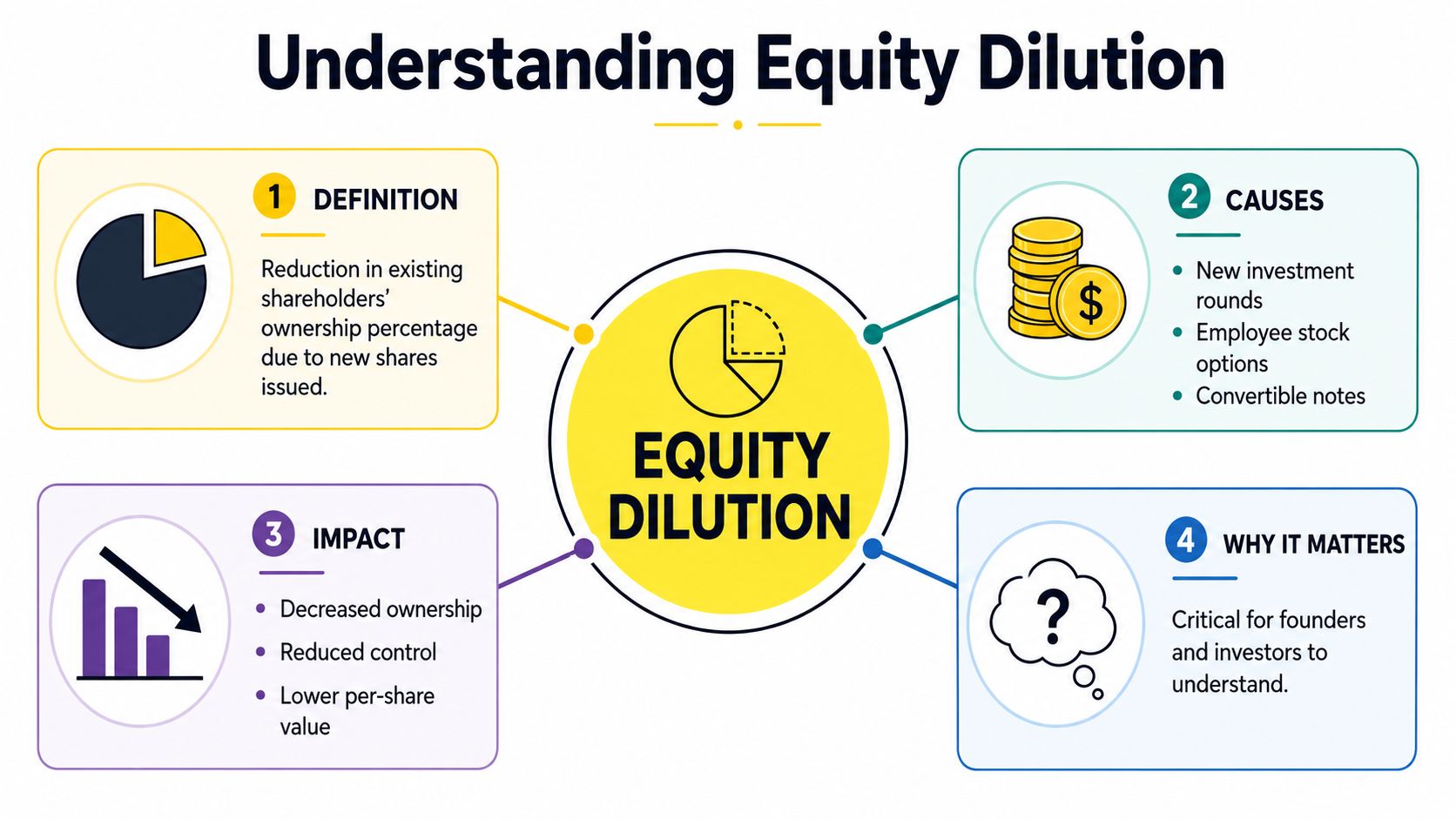

What Is Equity Dilution?

Equity dilution is the reduction in an existing owner’s percentage stake when a company issues new shares. Your share count might stay the same, but your percentage goes down because the company has increased the total number of shares outstanding, as explained in SVB’s overview of startup equity dilution.

The pizza analogy

Think of the company as a pizza cut into slices. If you own all the slices, you own all the pizza. If the company cuts the same pizza into more slices and gives some to new people, you still hold your original slices, but they represent a smaller percentage of the whole.

That’s why founders get confused. They hear “you still own your shares” and assume nothing important changed. But ownership rights often track the percentage, not just the raw number of shares.

The simplest cap table example

The math is straightforward:

- Founder shares owned: 1,000,000

- Total shares before issuance: 1,000,000

- Founder ownership before issuance: 100%

- New shares issued: 250,000

- Total shares after issuance: 1,250,000

- Founder ownership after issuance: 80%

You still own 1,000,000 shares. What changed is the denominator. That’s the whole engine of dilution.

Where founders usually get tripped up

Three points cause most of the confusion:

- Percentage vs. share count: you can keep the same number of shares and still be diluted.

- Value vs. control: dilution does not automatically mean your stake is worth less in absolute dollars.

- Common vs. preferred rights: two people can own equity in the same company but hold very different legal rights. If you want to understand that difference, read this guide on preferred stock.

Dilution is not always a sign that something went wrong. It often means the company issued new equity to raise capital, attract talent, or convert an earlier financing instrument.

The Math of Dilution in Realistic Cap Table Examples

A founder’s best defense is a cap table that you can read. The key question is always the same: what is my ownership percentage before and after this event?

Wikipedia’s summary captures the core mechanism well: dilution happens because the total share denominator increases, and that can also affect voting control and earnings per share if results don’t rise proportionally, as noted in its entry on stock dilution.

Example one with one founder and one new issuance

Start with a simple company:

| Stakeholder | Pre-Financing Shares | Pre-Financing % | Post-Financing Shares | Post-Financing % |

|---|---|---|---|---|

| Founder | 1,000,000 | 100% | 1,000,000 | 80% |

| New Investor | 0 | 0% | 250,000 | 20% |

| Total | 1,000,000 | 100% | 1,250,000 | 100% |

This example matters because it strips away valuation language and shows the bare mechanics. The founder didn't transfer shares to the investor. The company issued new shares.

Example two with more moving parts

A realistic startup cap table usually includes more than one founder and often an option pool. That's where people stop trusting their own math.

Here is a sample structure using the same logic:

| Stakeholder | Pre-Financing Shares | Pre-Financing % | Post-Financing Shares | Post-Financing % |

|---|---|---|---|---|

| Founder A | 600,000 | 60% | 600,000 | smaller percentage |

| Founder B | 400,000 | 40% | 400,000 | smaller percentage |

| Option Pool | 0 | 0% | new shares issued | percentage created |

| New Investor | 0 | 0% | new shares issued | percentage created |

| Total | 1,000,000 | 100% | increased total | 100% |

I'm keeping that second table qualitative on purpose. In practice, the exact result depends on the number of new shares issued, whether the option pool is created before or after the priced round, and whether any convertibles are included in the “fully diluted” number.

Why legal drafting changes the math

The danger isn't arithmetic. It's definitions.

A term sheet might refer to:

- Outstanding shares

- Fully diluted shares

- Reserved but unissued option pool shares

- Shares issuable on conversion

- Shares issuable on exercise

Those categories can produce different percentages depending on the deal language. Founders often think they agreed to one dilution outcome, then discover the financing documents define the cap table more broadly than expected.

If you can't point to the exact definition of “company capitalization” in the documents, you don't yet know your dilution.

That's also why stock compensation planning matters early. If your company is using options, this article on startup stock options helps frame the issue from the employee-equity side as well.

What Are the Common Causes of Equity Dilution?

Most dilution does not happen in one dramatic event. It happens through a series of ordinary company decisions.

CRV notes that industry guidance often places seed round founder dilution in the 15% to 25% range, with Series A rounds often creating another 15% to 25% of dilution. It also gives an example where founders' combined ownership moved from 85% to 70.8% after an employee option pool and an investor round, showing how multiple issuances stack together in real life, as discussed in CRV's dilution guide.

New financing rounds

This is the classic version. The company sells newly issued shares to investors in exchange for capital. Existing holders are diluted because the total outstanding share count rises.

The legal focus here is not just price. It's also board approval, shareholder approval thresholds, class rights, and whether any investors have participation rights in the new round.

Employee option pools

Founders often overlook this one because it doesn't feel like a financing event. But creating or expanding an option pool can dilute existing holders even before every option is granted or exercised, depending on how the deal documents define the capitalization.

That matters because investors often negotiate for an option pool to be in place before they invest. If the pool is added on a pre-money basis, founders typically feel more of the dilution than they expected.

Convertible instruments

SAFEs, convertible notes, warrants, and similar instruments can all lead to future share issuance. They often postpone the dilution discussion rather than eliminate it.

That delay causes problems because a founder may sign several instruments over time without seeing a single priced-round cap table showing the combined impact. When conversion finally happens, the cumulative dilution can be much larger than the founder assumed.

A practical way to think about timing

Instead of asking “will this dilute me,” ask:

- When does it convert or get issued

- How is the conversion price determined

- Which shares are counted in the denominator

- Who bears the dilution under the document wording

Those four questions usually reveal more than the headline financing label.

Consequences of Dilution for Founders Investors and Employees

Dilution matters because ownership percentage is tied to much more than economics. It can shift control, incentives, and future negotiating power.

Founders may lose control earlier than expected

A founder can still run day-to-day operations while holding a much smaller percentage than they originally planned. But if voting power follows share ownership, each issuance can reduce the founder's practical influence in board and shareholder decisions.

Founders often regret treating the first round as a one-off event. A small concession in one round can become a larger control issue after later rounds, pool increases, and conversions.

The question isn't only “how much am I giving up now.” It's “what does this leave me with after the next two financing events?”

Investors care about preserving their position

Early investors track later dilution because they don't want a meaningful stake to shrink without the chance to maintain it. That's why they negotiate for participation rights and anti-dilution protections in some circumstances.

Not all investor protections are equal, though. Some clauses are routine and balanced. Others can shift a great deal of economic pain onto founders and common holders if the company later raises at a lower price.

Employees often misunderstand option value

Employees usually focus on the number of options they've been granted. That's incomplete. They need to understand what percentage those options represent on a fully diluted basis and how later issuances may reduce that percentage.

Founders should care about this too. A poorly explained equity package creates disappointment and distrust later. If you're structuring founder and team equity early, this discussion of founder vesting is closely related because vesting and dilution work together in the long-term ownership picture.

Two common founder scenarios

- Scenario one: a founder accepts a round that seems modestly dilutive, then learns the option pool expansion was baked into the pre-money calculation.

- Scenario two: a founder signs several convertibles, assumes the next priced round will sort it out, then discovers the combined conversion meaningfully changes control.

Neither problem is exotic. Both show up in routine deals.

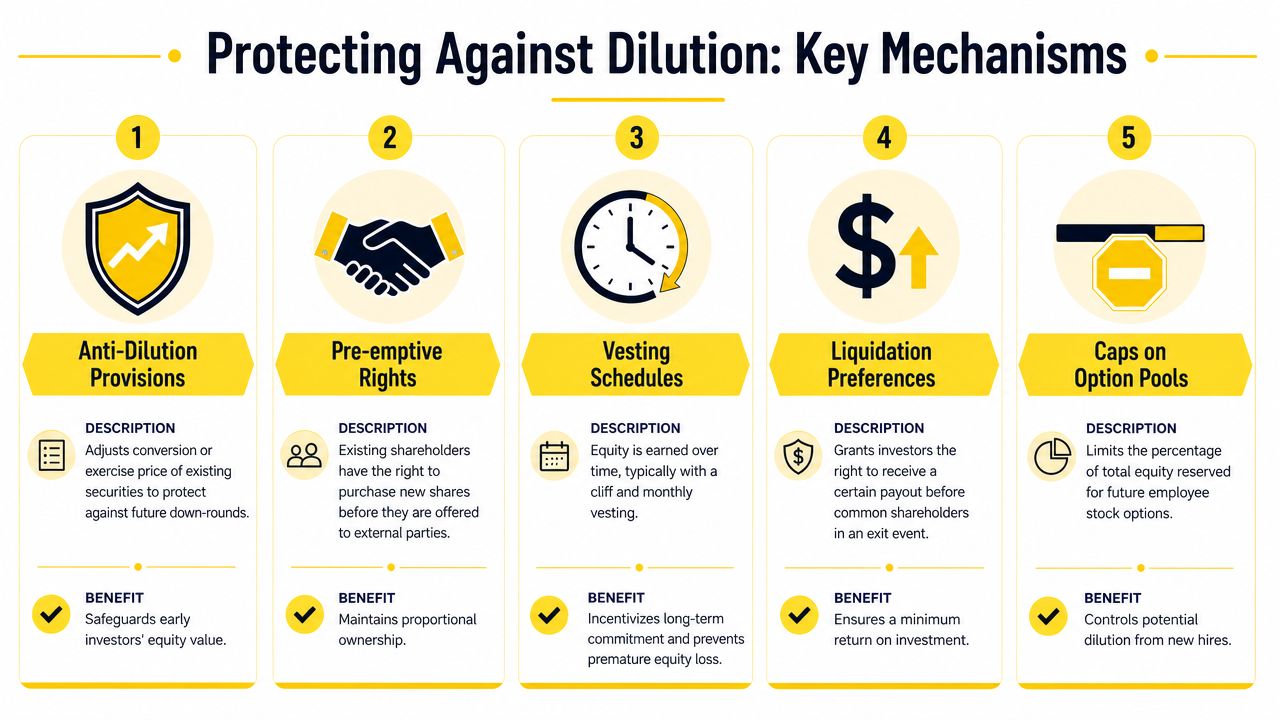

How Can You Protect Against Excessive Dilution?

You usually can't eliminate dilution if you're raising growth capital. You can, however, manage it with better documents and better modeling.

BDC points out that dilution can come from stock option exercises, convertible instruments, and new share issuance, and that the impact depends on valuation, conversion terms, and whether an option pool is expanded before or after the round. That's why scenario planning matters, as explained in BDC's article on equity dilution.

Preemptive rights

These rights let an existing shareholder buy part of a new issuance to maintain their percentage stake. For founders and early investors, they can be a practical way to avoid passive dilution in future rounds.

The key drafting issue is scope. The clause should define which issuances trigger the right, which are excluded, how notice works, and how long the holder has to decide.

Anti-dilution provisions

These clauses usually protect investors, not founders. They become especially important in a down round, when new shares are sold at a lower price than an earlier round.

You'll often hear about full ratchet and weighted average formulas. The legal and economic effect can differ sharply. Even when the term sounds familiar, you need to check the actual formula in the documents.

Rights of first refusal and transfer controls

These clauses don't directly stop dilution from new issuance, but they help control who can acquire equity and on what terms. That matters in closely held companies, especially where a founder group wants to avoid unexpected third-party ownership.

Option pool discipline

You should model option pool increases carefully. A large pool may be justified for hiring. But if the number is vague or inserted without a hiring plan, founders can absorb dilution without a clear business reason.

Document review matters more than labels

A clause called “standard” may still be expensive. A founder-friendly result depends on the interaction among the term sheet, share purchase agreement, investor rights agreement, voting agreement, and shareholder agreement.

If you're reviewing deal documents, the share issuance terms deserve close attention. This guide to stock purchase agreements for 2026 is a useful starting point for understanding where those protections and definitions usually sit.

Cross-Border Considerations for US-Canada Transactions

A founder signs a term sheet with a U.S. investor on Friday, then learns on Monday that the company's Canadian documents define share rights differently from the U.S. financing model. The ownership math may still look familiar. The legal result may not.

Securities law follows the holder, the issuer, and the deal structure

A share issuance that crosses the U.S.-Canada border can trigger securities rules in more than one place at the same time. If a Canadian corporation sells shares to U.S. investors, U.S. federal rules may matter alongside Canadian provincial requirements. If a Delaware company issues shares to Canadian buyers, the reverse can be true. Founders often start with filing and exemption guidance from the SEC and, for Ontario deals, the Ontario Securities Commission.

The key point is practical. Dilution is not only about how many new shares are issued. It is also about whether the issuance was valid, whether resale restrictions were handled properly, and whether the company used the right exemption in each jurisdiction. A cap table can say one thing while the legal paperwork says another.

The same percentage can carry different tax consequences

Cross-border structures add another layer. Two founders can each hold 20 percent on paper, yet face very different tax results depending on the entity, the share class, where they live, and how the shares were granted or converted. U.S. taxpayers often review federal tax treatment under IRS guidance. Canadian tax treatment can turn on separate rules and planning assumptions.

That is why quick fixes are risky.

For example, a company may issue a new class of shares to solve an investor concern, then discover later that the new class affects tax planning, employee equity treatment, or exit proceeds in ways no one modeled at signing.

Shareholder agreements do real work in cross-border deals

Founders often get into trouble. A U.S. term sheet may assume Delaware-style mechanics for approvals, preferred share rights, and conversion. A Canadian corporation may need those rights expressed through its articles, unanimous shareholder agreement, or other governing documents in a different way.

The clause title alone does not protect you. The clause has to fit the company's legal home.

Pre-emptive rights are a good example. In plain English, they give an existing holder the chance to buy enough of a new issuance to maintain their percentage. But the details matter. Who gets notice. How long they have to respond. Whether the right applies to all new shares or only certain financings. Whether the right is contractual, built into the governing documents, or limited by securities law exemptions. Across the border, those details can change both enforceability and deal timing.

If you want to compare how these rights usually appear in venture financings, this guide to the NVCA term sheet and related financing provisions is a useful reference point.

One cross-border mistake can distort the whole cap table

I often see companies mix U.S. financing language with Canadian corporate documents and assume the pieces will line up later. Sometimes they do. Sometimes they produce disputes over board approval thresholds, class votes, conversion triggers, transfer restrictions, or whether an investor had a valid right to participate in the next round.

A simple checklist helps catch that early:

- Which entity is issuing the shares

- Which jurisdiction's corporate law governs the share rights

- Which holders have notice, participation, consent, or veto rights

- Which documents control if the term sheet and shareholder agreement say different things

- What the cap table looks like immediately after closing, on both an issued and fully diluted basis

In cross-border financings, dilution works like water poured into a measuring cup. The volume change is easy to see. The legal container determines what counts, who has priority, and whether the measurement will hold up when tested.

Frequently Asked Questions

Is equity dilution always bad for founders?

No. Dilution can be a rational trade if the company is issuing shares to raise capital, recruit talent, or complete another strategic step that helps the business grow. The problem is not dilution by itself. The problem is accepting dilution you didn't understand, didn't model, or didn't document properly.

What is a fully diluted cap table?

A fully diluted cap table usually includes not only issued shares, but also shares that may be issued under options, warrants, convertibles, or reserved pools, depending on the document definitions. That's why two people can talk about ownership percentages and both sound right while using different assumptions. The legal definition in the financing documents controls.

How do warrants cause dilution?

A warrant can give the holder the right to buy shares in the future. If the warrant is exercised and new shares are issued, the total share count rises. Existing holders then own a smaller percentage of the company unless they also participate in a way that preserves their stake.

Are anti-dilution rights the same in Canada and the United States?

No. The business concept may be similar, but the drafting, market norms, securities law context, and enforcement issues can differ by jurisdiction and by the company's governing documents. Cross-border companies should not assume a clause lifted from one deal form will work the same way in another legal system.

Can a founder stop dilution completely?

Usually not, at least not if the company intends to issue equity over time. Most startups need some combination of financing, option grants, or convertible instruments. The realistic goal is to control dilution, price it properly, and protect core governance rights rather than pretending future issuances will never happen.

If you're raising capital, revising a cap table, or sorting out shareholder protections across the U.S. and Canada, a careful legal review early is usually cheaper than fixing a broken financing structure later. Mayo Law advises founders and companies on cross-border business matters, including the documents that shape ownership, control, and future fundraising.

How Mayo Law Can Help

Equity dilution issues usually surface when a company is already under pressure to close a financing, grant equity, or clean up a cap table. Mayo Law serves clients across Toronto, the GTA, and on cross-border matters. To discuss your situation, visit international business counsel.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles