You’re usually asking what is preferred stock at a very specific moment. A term sheet just arrived. An angel says they want “preferred.” Your accountant mentions dividends. Or you’re comparing a startup financing document to a publicly traded preferred share listed on an exchange and realizing those two things seem related, but not identical.

That confusion is normal. “Preferred stock” sounds simple, but in practice it covers two very different worlds: public market income securities and private company financing rights. If you miss that distinction, you can misunderstand control, downside protection, pricing, and even taxes.

At Mayo Law, we help founders, investors, and cross-border businesses in Toronto, the GTA, and across the border work through business structures that often have legal and commercial consequences in both Canada and the U.S. If you’re still sorting out your company’s formation documents, it also helps to understand what a certificate of incorporation is.

Published: June 14, 2026

Updated: June 14, 2026

Read time: 13 minutes

What Is Preferred Stock?

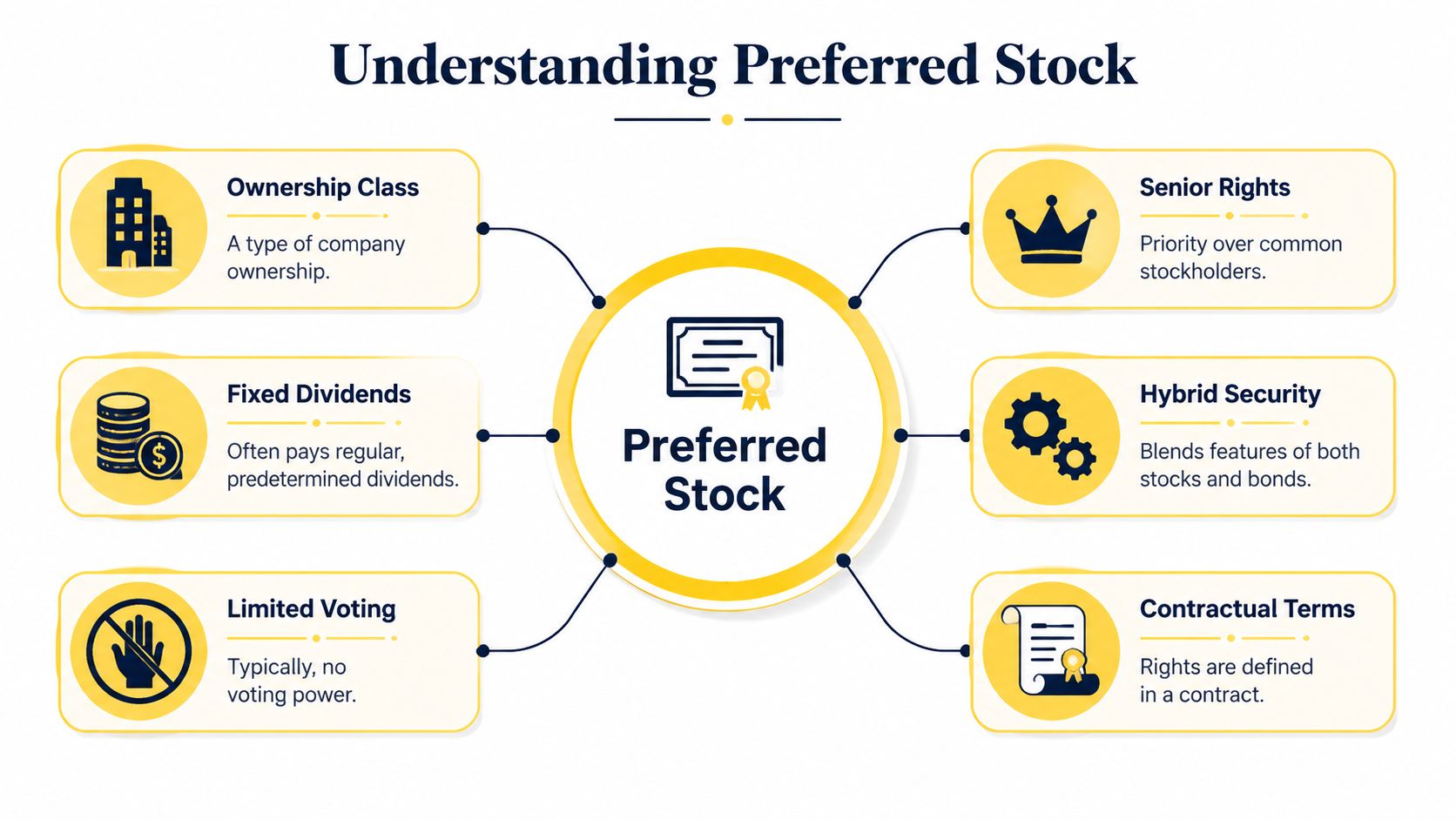

Preferred stock is a class of corporate ownership that usually gives its holder stronger economic rights than common stock, but fewer control rights than creditors. It often sits between debt and common equity because it can pay fixed dividends, carry priority on a sale or liquidation, and still remain an ownership interest rather than a loan.

A simple way to think about it is a VIP ticket. The holder usually gets into the payment line before common shareholders. But that ticket doesn’t usually hand over day-to-day control of the company, and it doesn’t outrank lenders.

That “middle position” is why lawyers and investors call preferred stock a hybrid security. It borrows some features from bonds, such as a stated dividend or par-based pricing in public markets. It also keeps equity features, such as possible conversion into common stock or a claim on company value if the business grows.

The word preferred matters because the preference is contractual. The rights usually don’t exist by magic or by label alone. They live in the company’s charter, financing documents, and the terms of the specific share class.

Preferred stock is less about a vague “better share” and more about a negotiated package of rights.

For a founder, that means preferred stock changes who gets paid first and who can block certain decisions. For an investor, it changes downside protection and potential upside.

Common Stock vs Preferred Stock A Direct Comparison

Most confusion disappears once you compare the two side by side. Common stock is the standard founder and employee equity typically envisioned. Preferred stock adds negotiated rights on top.

Preferred Stock vs. Common Stock at a Glance

| Feature | Preferred Stock | Common Stock |

|---|---|---|

| Dividend rights | Often has a stated dividend preference | Dividends come later, if declared |

| Liquidation priority | Usually paid before common holders | Paid after preferred holders |

| Voting rights | Often limited, but may include protective votes | Usually carries general voting rights |

| Conversion rights | May convert into common stock | Already common stock |

| Risk and upside profile | More downside protection, often capped or structured | More residual upside, more downside risk |

| Typical use | Investor protection or income-focused security | Founders, employees, long-term growth holders |

That's the legal comparison. The business comparison is even more useful.

Is preferred stock better than common stock?

It depends on what you want.

If you're a founder, common stock usually preserves the clearest long-term upside. You participate in the company's growth without creating a senior claim over your own cap table. But common stock is also the class that gets paid last.

If you're an investor, preferred stock often gives more protection. You may receive dividend rights, conversion rights, and a liquidation preference that improves your position if the company sells for less than everyone hoped.

A startup example makes this concrete. Suppose two people own the same percentage on paper. One holds common shares. The other holds preferred shares with a liquidation preference and conversion rights. If the company exits at a modest value, those two holders may receive very different outcomes.

Practical rule: Common stock is usually about growth and control. Preferred stock is usually about protection and negotiated economics.

That's why “which is better?” is the wrong question. The right question is: better for whom, and in what scenario?

In startup planning, this issue often sits beside option pools, founder vesting, and investor rights. If you're comparing equity tools more broadly, see how startup teams use stock options in a startup.

Key Rights and Features of Preferred Stock

The label “preferred” doesn't tell you enough. The actual value sits in the rights attached to the shares. In private deals, these rights are heavily negotiated. In public markets, they're usually standardized and priced into the security.

Dividends

Some preferred shares promise regular dividends. But “dividend” doesn't always mean “guaranteed cash in your account on schedule.”

A key distinction is cumulative versus non-cumulative preferred. According to this explanation of preferred stock features, cumulative preferreds legally require skipped dividends to accumulate and be paid later, while non-cumulative preferreds do not repay omitted dividends.

That difference matters a lot in a stressed company.

- Cumulative preferred: Missed dividends stack up. The company may need to clear that backlog before paying common holders.

- Non-cumulative preferred: If the board skips a dividend, the holder usually can't claim the skipped amount later.

- Founder takeaway: A dividend that sounds harmless in good times can become pressure on future financing or distributions.

In public market preferreds, dividends often function like income terms. In private startup deals, dividends may exist mostly on paper unless there's a sale, redemption, or other liquidity event.

Liquidation preference

This is the clause founders underestimate most often.

A liquidation preference tells you who gets paid first if the company is sold, wound up, or sometimes merged. Preferred holders usually recover their negotiated amount before common holders share in the remaining proceeds.

Take a simple scenario. A startup raises capital on preferred shares, then sells for a disappointing price. The preferred investor may receive their preference first, leaving much less for founders and employees than the headline sale price suggests.

Here's where nuance matters:

- Non-participating preferred: The holder usually chooses either the preference amount or the amount they'd receive by converting to common.

- Participating preferred: The holder may receive the preference first and then also participate with common in remaining proceeds.

- Caps: Some deals limit how much a participating preferred holder can receive.

If you only track ownership percentages and ignore liquidation preference, you can badly misread who gets paid on exit.

Conversion rights

Preferred stock often includes a path into common stock.

A convertible preferred lets the holder exchange preferred shares for common shares. That can be valuable when the company performs well and the common upside exceeds the fixed preference economics. The Achievable summary also notes that some preferreds are mandatory convertible, meaning they automatically convert on a preset date.

In venture financing, conversion usually matters at an exit or public offering. If the company becomes valuable enough, investors often convert because the common upside is better than holding onto the preference.

For founders, conversion rights are not just an investor perk. They shape the cap table you'll have later.

Voting rights and protective provisions

Many people hear that preferred stock “usually has no voting rights” and stop there. That's incomplete.

Preferred shares often do have limited voting rights, but those rights can be powerful. Instead of voting on every ordinary matter, preferred holders may get consent rights over major actions such as:

- issuing a new senior class of shares

- changing charter documents

- selling the company

- taking on significant debt

- changing board structure

- redeeming shares or paying certain distributions

These are often called protective provisions. They don't necessarily let the investor run the company day to day. They do let the investor stop the company from changing the bargain after the money is invested.

Anti-dilution protection

Anti-dilution clauses protect investors if the company later issues shares at a lower price.

In plain English, this can reprice the investor's conversion economics so their position doesn't suffer as much from a down round. Founders should read this carefully because the math can shift value unexpectedly.

Two practical points matter:

- Some formulas are harsher on founders than others.

- The clause can affect employee equity as well as founder ownership.

A founder-friendly term sheet often focuses on balancing investor protection with the company's ability to survive a rough financing market.

Call and redemption rights

In public markets, many preferreds are callable. As described in the same Achievable overview, that means the issuer can redeem them at par after a specified date, creating call risk and capping upside when rates decline.

This is easy to miss. A high stated dividend can look attractive, but if the issuer can call the shares once market conditions improve, the investor may lose the chance to keep that higher-income instrument.

In private companies, the rough cousin of a call feature is a redemption right or buyback right. That may let investors force the company to repurchase shares after a period, subject to legal and solvency limits. Founders need to treat that clause seriously. A redemption right can become real pressure if the company is mature but illiquid.

Don't read preferred stock by its label. Read it by payout order, conversion mechanics, veto rights, and exit triggers.

If these terms are going into a financing package, the operative language often sits across the charter, investor rights documents, and the share purchase paperwork. That's why deal teams usually review stock purchase agreements together with the cap table, not in isolation.

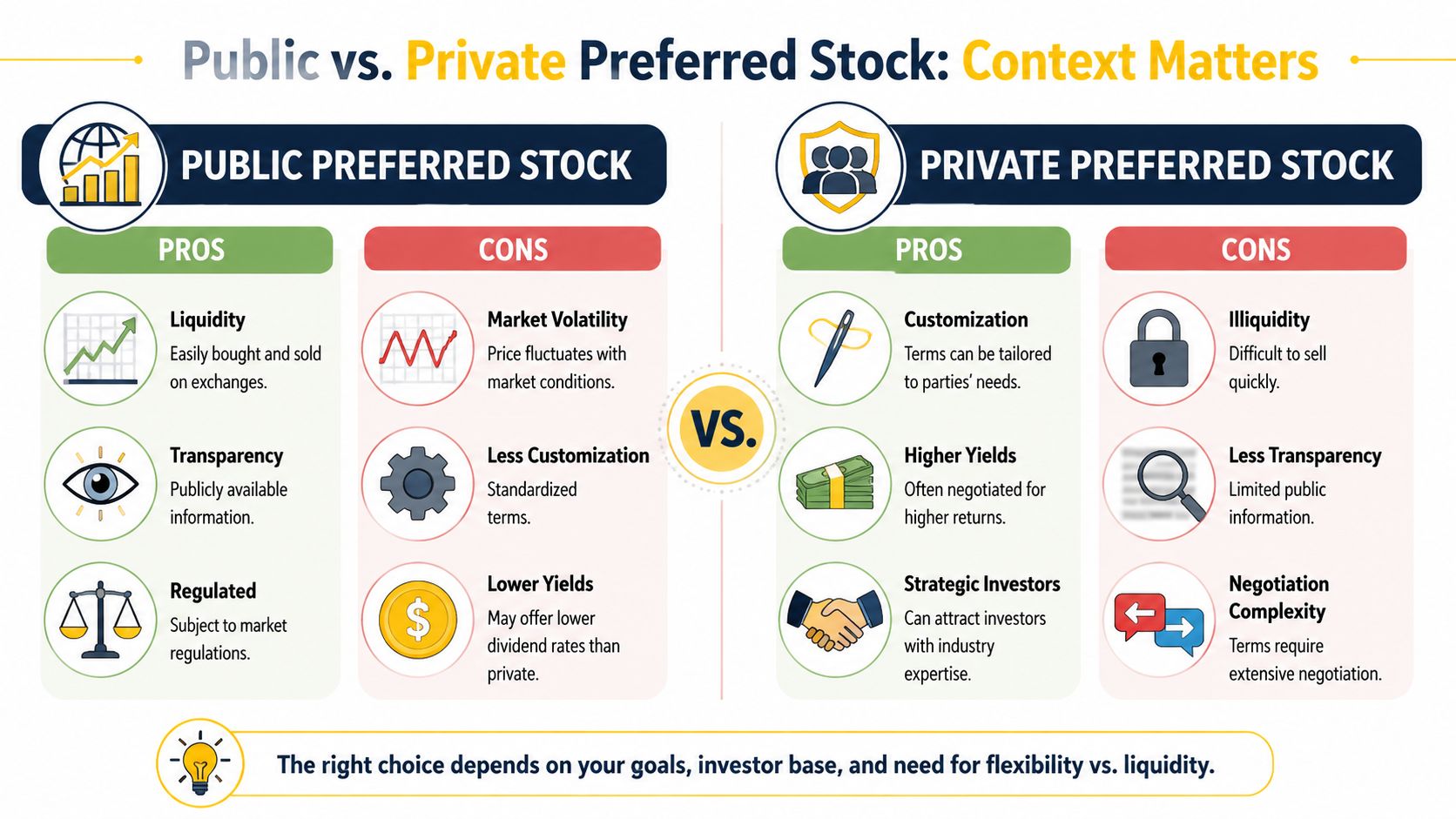

Public vs Private Preferred Stock Why the Context Matters

A founder hears “preferred stock” and assumes it means one thing. Then a bank investor talks about yield and call dates, while a VC talks about liquidation preference and board approval rights. Same label. Very different tool.

Public-market preferred stock is usually bought for income. Private-company preferred stock is usually negotiated for protection, priority, and influence over key company decisions.

Public preferred stock

In public markets, preferred shares often sit halfway between a bond and common stock. Investors usually care about the stated dividend, the issuer's credit quality, interest-rate sensitivity, whether the shares can be called, and how easily they trade.

The legal terms are often more standardized than in a startup financing. You are usually not negotiating board seats, veto rights, or bespoke conversion triggers. You are buying a market instrument that is priced mainly for cash flow and risk.

That framing matters for angel investors who also invest in public securities. The word “preferred” can suggest extra safety, but public preferreds still move with rates, issuer stress, and call features.

Private preferred stock

In a startup, preferred stock works more like a contract package wrapped around equity. Carta explains that private companies often issue preferred shares to investors such as VCs and angels, with rights like liquidation preferences, conversion rights, and buyback provisions, in Carta's comparison of common and preferred stock.

For founders, the question is not “What dividend does this pay?” Instead, the question is “What happens to control and exit proceeds if things go well, badly, or somewhere in between?”

A Series Seed or Series A preferred round can change:

- who gets paid first in a sale

- whether new financing can close without investor approval

- how painful a down round becomes

- how much room the company has to make hard decisions under pressure

That is why private preferred stock deserves line-by-line review. The economics and the control terms travel together.

Why the distinction changes decisions

If you buy public preferred through a brokerage account, you are usually underwriting income and market risk.

If you sign a venture term sheet, you are allocating downside, upside, and decision-making power.

Those are different jobs.

Founders in cross-border deals can get tripped up here. U.S. investors may use “preferred” as shorthand for a familiar VC package. Canadian founders may hear the same word and focus first on share terms under corporate law, tax treatment, or redemption mechanics. Neither side is wrong, but they may be solving for different risks.

That is the practical lesson. Do not ask only whether the security is “preferred.” Ask preferred for what purpose: income, downside protection, control, or some mix of the three.

If your financing may touch U.S. offering rules or a later public transaction, it also helps to understand related filing mechanics such as the SEC registration fee.

How Are Preferred Stock Dividends Taxed in the US and Canada

Tax is where broad internet advice becomes dangerous. The same preferred instrument can produce different tax results depending on the holder, the issuer, the account type, and whether the dividends qualify for special treatment.

U.S. tax treatment

In the U.S., preferred stock dividends may be taxed as qualified dividends if the legal requirements are met. But not every preferred dividend qualifies, and holding period rules matter. The IRS explains the general framework in IRS Publication 550 on investment income and expenses.

For founders and investors, the practical point is simple: don't assume “dividend” automatically means the best available rate. Review the issuer, your holding period, and whether the distribution is treated as a dividend for tax purposes.

If the preferred shares are part of a startup financing rather than a public income investment, the tax question may also involve conversion, redemption, or exit treatment rather than routine cash payments.

Canadian tax treatment

In Canada, dividends on preferred shares are often analyzed under the Canadian dividend rules, and some may qualify for treatment associated with eligible dividends depending on the issuer and structure. The Canada Revenue Agency provides the general dividend framework through its guidance on dividend tax credits and taxable amounts.

That still doesn't answer every real-world question. Cross-border holders may face withholding, foreign tax credit issues, or different treatment depending on whether they hold the shares personally or through a corporation.

Tax on preferred stock isn't just about the label on the certificate. It depends on who issued it, who holds it, and what event produced the payment.

What cross-border investors should watch

If you live in one country and hold preferred shares issued in the other, ask at least three questions early:

- What is the payment legally called? A dividend, redemption amount, and sale proceeds may be taxed differently.

- Is there withholding? Cross-border payments can trigger source-country withholding.

- Will a treaty or credit help? Relief may exist, but only if the structure and reporting line up.

This is one of those areas where legal and tax review should happen together, not one after the other.

Practical Considerations for Founders and Investors

A financing round can look excellent on the headline terms and still leave founders boxed in later. The same is true for investors. A preferred share can sound safe because it has a dividend or a preference, yet the outcome depends on what kind of preferred stock you are buying and what rights travel with it.

That distinction matters more than many basic explainers admit. In the public markets, preferred stock is often bought for income. In venture deals, preferred stock is usually bought for downside protection and control. Same label. Very different economic story.

For founders, the practical question is simple: what have you promised away besides price per share? For investors, the question is different: are you buying a yield instrument, or are you buying a negotiated position in the company?

If you're a founder reviewing a term sheet

Start with the clauses that affect outcomes in a sale or the next financing, not the clauses that sound familiar from the pitch deck.

Read the preferred terms in this order:

- Liquidation preference. This sets the payout order if the company is sold, wound up, or sometimes treated as sold under the documents.

- Protective provisions. These are approval rights over actions such as issuing a new senior class, changing charter documents, or selling the company.

- Conversion and anti-dilution. These determine how preferred turns into common and how pricing changes in a down round.

- Redemption rights. These can give investors a future exit lever if the company does not reach one on its own.

A term can be legally standard and still have a sharp business effect. For example:

“The holders of Preferred shall be entitled to receive, prior and in preference to any distribution to Common, an amount equal to the original purchase price plus any declared but unpaid dividends.”

Plain English: common shareholders get paid only after that amount is satisfied.

Another common clause says:

“So long as any Preferred remains outstanding, the Company shall not authorize a new class of senior securities without approval of the Preferred holders.”

That is a consent right. In practice, it can shape your next round because you may need investor approval before offering better terms to new money.

Founders often focus first on valuation because it is easy to compare. Rights are harder to compare, but they often decide who gets money, who gets a veto, and how much room management has left when conditions change. If you want a legal review that ties the financing documents back to cap table, governance, and fundraising strategy, work with a startup business attorney.

If you're an investor evaluating preferred stock

Begin by sorting the investment into the right bucket.

For public preferreds, the main questions are income, rate sensitivity, credit risk, and call risk. Schwab explains that preferred shares often trade more like fixed-income instruments than common equity, including exposure to interest-rate moves and the possibility that the issuer redeems the shares before the investor expected, as discussed in Schwab's overview of preferred stock as an income tool. If your thesis is yield, document terms still matter, but market behavior matters too.

For private preferreds, trading price is usually irrelevant because there is no active market. The work is in the documents. You are assessing the company, the cap table, and the rights package together.

Focus on a few points:

- Preference stack. Find out who is ahead of you and whether future investors can become senior to you.

- Participation or non-participation. This affects whether holders get their preference and then also share with common.

- Conversion mechanics. Check when conversion is optional, when it becomes automatic, and at what ratio.

- Board and consent rights. These determine how much influence you have if the company misses plan.

- Exit path. A term that looks protective in a large exit can produce tension in a modest sale.

A common founder surprise shows up when the company receives an acquisition offer that sounds respectable but is not high enough to clear the preference stack cleanly. On paper, everyone owns shares. In the payout waterfall, economics can be very uneven.

A common public-market investor surprise is different. The issuer keeps paying the dividend, but the security drops in market value because rates rise, credit concerns increase, or the shares are called at a time that caps the investor's upside.

The practical takeaway is straightforward. If you are looking at public preferreds, treat them partly like an income security with equity features. If you are looking at VC preferreds, treat them like a negotiated control and downside-protection package that sits on top of the common. That difference changes how you price risk, read the documents, and judge whether the deal is attractive.

Frequently Asked Questions

Does preferred stock usually have voting rights?

Preferred stock often has narrower voting rights than common stock. In a public company, many income-style preferred shares have little or no ordinary voting power unless the issuer misses dividends or a special matter affects that class directly.

In a startup financing, influence often sits in protective provisions rather than day-to-day voting. Those provisions can require preferred approval before the company amends its charter, creates a more senior class of shares, changes board structure, or approves a sale. For founders, the practical question is not just, "Do they vote?" It is, "Which decisions can they block?"

What does it cost a company to issue preferred stock?

The cost depends on the context. A private financing usually involves legal drafting, term negotiation, securities law compliance, tax review, cap table updates, and board and shareholder approvals. A public issuance can add exchange requirements, offering documents, and filing costs. In the U.S., the SEC publishes current filing fee information on the SEC fee rate advisory page.

The hidden cost is often time. If the share terms are heavily negotiated, management and counsel can spend significant time aligning economics, control rights, and closing mechanics.

How long does it take to create a preferred stock financing?

A straightforward seed or angel round can close fairly quickly if the company's charter is clean and the lead terms are settled early. A later-stage round usually takes longer because investor rights, existing preferences, tax points, and disclosure issues tend to be more detailed.

Cross-border deals often add another layer. The company may need to confirm how local corporate law, securities exemptions, and tax treatment fit together before documents can be finalized.

What happens to preferred stock in an acquisition?

Start with the contract. The outcome usually turns on liquidation preference, participation rights, and conversion mechanics.

Here is the practical version. If the sale price is modest, preferred holders may take their preference first, which can leave less for common. If the sale price is high enough, they may convert to common because that produces a better return. Some preferred stock allows participation, which means the holder can receive the preference and still share in the remaining proceeds. That is why two shareholders with the same percentage ownership on a cap table can receive very different amounts at closing.

Are public preferred shares and startup preferred shares regulated the same way?

No. Public preferred shares are generally issued into a standardized market with exchange rules, public disclosure obligations, and trading conventions. Private startup preferred shares are typically sold under private offering exemptions and documented through negotiated financing papers.

The legal setting matters because the product is serving a different function. Public preferred usually looks more like an income security with equity features. Startup preferred usually looks more like a package of downside protection and approval rights. In Ontario, securities regulation is overseen through the Ontario Securities Commission. In the U.S., public securities oversight sits with the U.S. Securities and Exchange Commission.

Why do public preferred shares often trade near a set issue amount?

Many public preferred shares are issued with a stated par or liquidation amount, often in standard increments such as $25 or $100. That amount acts as an anchor for how investors discuss price, yield, and call risk.

But "near par" does not mean "fixed at par." Market prices can move above or below that level as interest rates change, the issuer's credit profile changes, or a possible redemption date gets closer. For income-focused investors, par value helps frame the math. For founders looking at private company preferred, it usually has far less practical importance than liquidation preference, conversion rights, and consent terms.

If you're dealing with preferred stock in a financing round, an investment, or a cross-border structure, the right answer usually isn't in the label. It's in the rights attached to the shares and how those rights work under the governing documents and the law. Mayo Law advises on cross-border business matters involving corporate structuring, financing documents, and investor-facing agreements.

Preferred stock can be useful. It can also reshape control, payout order, and tax treatment in ways that are easy to miss on a quick read. If you're a founder or investor, the practical question is what this preferred stock lets someone do.

How Mayo Law Can Help

Preferred stock is often the point where economics and control start pulling in different directions. A founder may hear "preferred" and assume the issue is mainly dividend yield, which is often how public market investors use the term. In a private financing, the harder questions are usually who gets paid first, who can block a sale, who can force a vote, and how conversion rights work if the company grows or struggles.

Mayo Law helps founders, investors, and companies address those questions in practical terms. That can mean reviewing a term sheet before it hardens into binding documents, comparing common and preferred rights in a cap table, or checking whether a U.S. or Canadian structure changes tax, governance, or enforcement risk.

Cross-border deals add another layer. A share class that looks familiar on paper can operate differently once you factor in the governing corporate statute, shareholder agreements, securities rules, and the location of the company, founders, and investors. Mayo Law advises clients across Toronto, the GTA, and on cross-border matters involving financing documents, corporate structuring, and investor-facing agreements. To discuss your matter, visit international business counsel.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

- International business legal services

- Business immigration legal services

- Regulatory compliance legal services