Published: June 15, 2026

Updated: June 15, 2026

Read time: 11 minutes

You may already have the job offer, the transfer discussion, or the business plan. What usually causes stress isn't the idea of the move. It's the fear of missing one legal or tax issue that turns a good opportunity into a costly problem. If you're planning a move from Canada to USA, the visa is only part of the file.

At Mayo Law, we help people in Toronto, the GTA, and across the border handle this process with licensing in both Ontario and New York on a matter that often touches both sides of the border. The move is common, but it isn't one-size-fits-all. According to CBC's reporting on Statistics Canada data, 126,340 people moved from Canada to the U.S. in 2022, the highest level in about a decade. If you're dealing with consular logistics, it also helps to understand what an embassy does before you start booking appointments and collecting records.

What Are the Main Visa Options to Move From Canada to USA?

A Canadian software engineer accepts a U.S. offer, lines up movers, and assumes the visa choice is a filing detail. It is not. The wrong category can delay entry, limit what the person can do for the business, and create tax timing problems if the move happens before the legal status is settled.

The visa has to fit the facts, the timeline, and the longer plan. I look at all three together because a category that works for entry can still be the wrong choice if it blocks a later green card strategy, leaves a spouse without work authorization, or pushes a founder into a structure that does not hold up under inspection.

| Visa Type | Who It’s For | Key Requirement | Typical Processing |

|---|---|---|---|

| TN | Canadian professionals in listed occupations | Qualifying profession and job offer | Often handled at the border or pre-flight inspection |

| L-1 | Executives, managers, or specialized knowledge employees | Qualifying relationship between Canadian and U.S. company | Petition-based process, often used for transfers |

| E-2 | Treaty investors and certain essential employees | Real operating business and qualifying investment | Consular application with detailed source-of-funds review |

| H-1B | Specialty occupation workers | Qualifying role and employer sponsorship | Petition-based, often less predictable than TN or L-1 |

If your case involves work sponsorship, transfers, or investor planning, a US-Canada immigration lawyer should assess the route before documents are drafted. Category selection affects more than approval odds. It can affect tax residence timing, corporate setup, and how cleanly you can move assets or continue running a Canadian business after entry.

TN visa

The TN is often the fastest work option for a Canadian professional whose job and credentials fit the treaty list. For the right applicant, it is efficient and practical.

The trouble is fit. A title like "consultant," "operations lead," or "product manager" may sound fine in a hiring meeting but raise problems at inspection if the duties do not match a listed TN profession. Officers compare the degree, the résumé, the support letter, and the actual job. If those pieces do not line up, the file weakens fast.

I usually treat TN as a strong option for employees with a clear reporting line and a defined professional role. It is less reliable for founders, mixed business-development roles, and jobs that combine management with hands-on work in a way the treaty categories do not describe well.

Practical rule: Draft the job description for the treaty category you can prove, not the broad role the company uses internally.

L-1 visa

The L-1 is often the better choice for a genuine cross-border transfer. It is built for related companies, not for loosely connected businesses trying to create a transfer story after the fact.

This route can work well for executives, managers, and specialized knowledge employees who have already been working for the Canadian entity in a qualifying capacity. It is also common for owners opening or expanding a U.S. office. The legal test goes beyond ownership charts. Officers want a coherent business record showing control, operations, staffing, and a real need for the transferred person in the United States.

The trade-off is scrutiny. If the U.S. company exists only on paper, has no credible operating plan, or cannot show how the transferee will perform qualifying duties, the petition becomes hard to defend. For new office cases, timing matters because the company may get only a limited approval period and then need to prove the U.S. operation is functioning.

E-2 visa

The E-2 is a strong option for Canadian investors and certain employees of treaty-owned companies. It can be a good fit for founders who are putting real capital at risk in an active U.S. business.

This category is often underestimated. Approval does not turn on the investment amount alone. Officers look at whether the funds are committed, whether the business is more than marginal, and whether the source of funds is fully documented. A good E-2 file reads like a due diligence package. Corporate records, bank transfers, tax records, contracts, lease documents, and the business plan should all support the same story.

There is also a tax planning point many people miss. Funding a U.S. business, moving personally, and changing tax residency in the same period can trigger Canadian departure issues and U.S. reporting obligations much sooner than expected. The visa strategy should be set with that timing in mind.

H-1B visa

The H-1B can work for Canadians in specialty occupations, especially where the role does not fit the TN list or the employer is already committed to a longer-term sponsorship path.

For many Canadians, though, H-1B is not the first route worth pursuing if TN or L-1 is available. It usually involves tighter timing, more employer compliance, and less flexibility. The employer must be ready to support the role properly, pay the required wage, and maintain the file after approval. That is manageable for established companies. It is harder for early-stage businesses and founders trying to build while also sponsoring themselves.

What is the easiest visa to get for a Canadian to work in the US

For a Canadian professional with a qualifying offer and a role that clearly matches the treaty list, the TN is often the most direct option.

Direct does not mean simple in every case. I have seen borderline TN applications fail because the employer letter used broad business language instead of duties tied to the profession, or because the applicant's degree supported one role while the company offered another. The easier case is the one prepared with the border interview in mind, not the one assembled after the move date is already booked.

Your Application Roadmap From Start to Finish

A Canadian accepts a U.S. job, gives notice, books movers, and assumes the visa piece will catch up. That is where avoidable problems start. A strong application plan does more than get an approval. It protects your start date, your tax timeline, and the rest of the move.

The order matters. First, confirm the right category based on the facts of the role, the employer, and your background. Next, build the filing record so the job description, credentials, corporate documents, and prior immigration history all say the same thing. Then prepare for the officer interview or border inspection, if the category requires one. After that, deal with medicals and civil documents where applicable. Last, plan for entry and the compliance steps that begin once you are in the United States.

For work-based matters, I usually have clients work through five checkpoints:

- Choose the route that fits the facts

- Draft the petition or support package with matching evidence

- Prepare for inspection, interview, or follow-up questions

- Time medicals and personal records properly where required

- Handle entry and post-entry compliance without gaps

That final checkpoint gets ignored too often. Approval is not the end of the process. I have seen cases approved on paper, then complicated by a poor border presentation, inconsistent answers, or bad timing around payroll, housing, and family travel.

What usually goes wrong

The file is often weakest in ordinary places.

- Forms do not match supporting records. A title on the form differs from the employer letter. Dates differ from prior filings. Ownership percentages shift between corporate records.

- The role is described too broadly. That creates problems at the exact moment an officer wants a clear professional fit.

- Evidence arrives late or in the wrong format. The underlying case may be workable, but the package does not show it well.

- The move is planned before the immigration calendar is settled. Resignations, home closings, school enrollment, and cross-border tax steps get set too early.

Bring the story your documents can prove, not the version you hope an officer will infer.

If you need support with petition drafting or employer-sponsored filings, employment immigration counsel can help structure the case before it reaches review.

How long does it take to move to the US from Canada

The timeline depends on the category and on how clean the facts are. A border-processed work category can move quickly if the role, credentials, and support letter line up. A petition-based case usually takes longer. Permanent residence filings and in-country status processes take longer still, and they create more opportunities for delay if family records, prior entries, or employer documents need correction.

The practical rule is simple. Do not lock in resignation dates, property sales, school changes, or business transfers until the immigration path is chosen and the application package is ready to file. That approach reduces legal risk, and it also helps avoid the tax and compliance mistakes that often begin when people treat the visa as the only moving part.

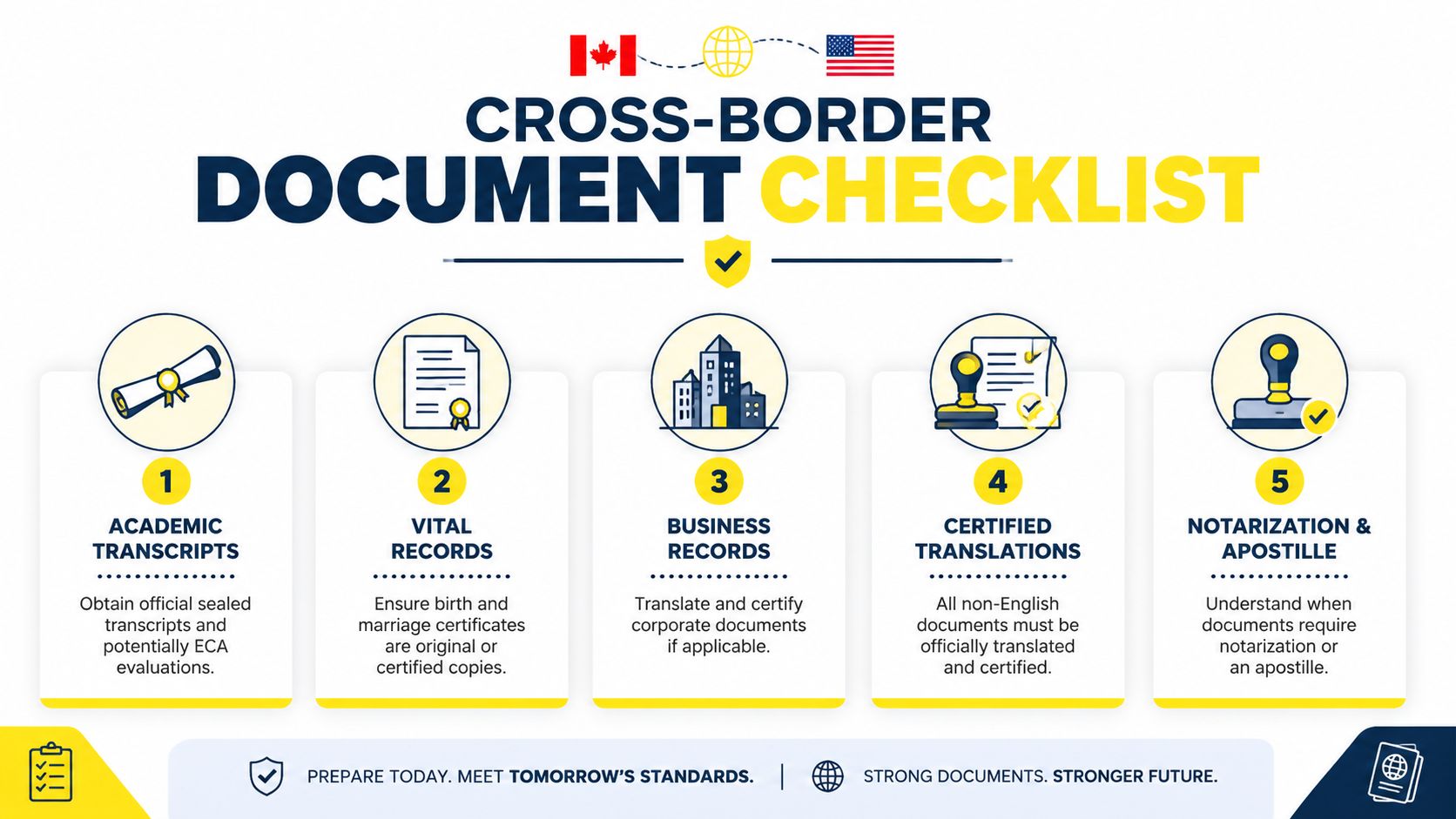

Preparing Your Documents for Cross-Border Scrutiny

A file can look perfectly acceptable in Canada and still fail under U.S. review because the records do not match, the copy quality is poor, or the signing formalities are wrong. I see this often with otherwise approvable cases. The problem is not the underlying facts. The problem is that the documents do not prove those facts cleanly.

Start by checking consistency across the full file. Names, dates, job titles, ownership percentages, and addresses should line up across passports, diplomas, corporate records, prior immigration filings, and civil documents. Small discrepancies create avoidable questions. At the border or in a petition review, those questions can slow a case down or shift attention to credibility.

Some records need more than a plain copy. Degrees may need transcripts or credential support. Birth and marriage certificates may need certified copies and, in some situations, translation. Corporate records for L-1 or E-2 cases often need organized minute books, share issuances, resolutions, and proof that the Canadian and U.S. entities relate to each other in the way the application says they do.

Documents that routinely need closer review include:

- Academic records used to support TN or H-1B qualification analysis

- Corporate records for L-1 and E-2 filings

- Civil status documents for spouses and children

- Translations for any non-English content

- Signature pages used in immigration, banking, and cross-border corporate matters

The weak point is usually not the headline document. It is the supporting record behind it.

A common example is the founder who has a real business and a legitimate expansion plan, but the corporate paperwork was handled informally for years. The share register says one thing, the resolutions suggest another, and the organizational chart was created after the fact. An officer may start to question the qualifying relationship, even where the business itself is genuine.

I also see professionals with the right degree and the right work history, but the record set is incomplete. The diploma is available, but not the transcript. The passport uses one version of the name, the degree uses another, and the employer letter introduces a third variation. Those are fixable issues if caught early.

For notarization and document handling, Ontario notary services can help with cross-border execution, certified copies, and signature formalities before they turn into filing problems.

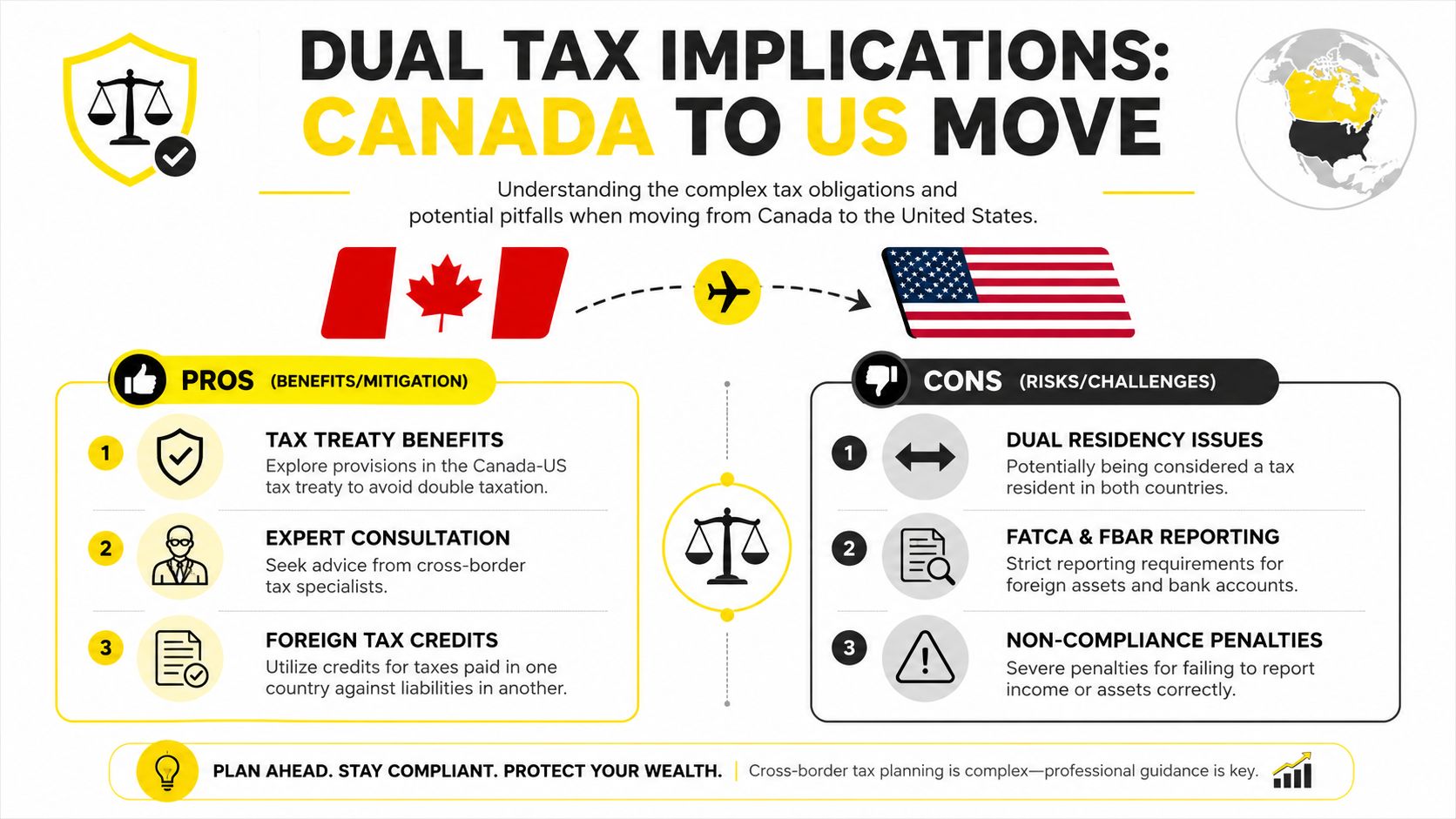

The Tax and Compliance Trap Most Canadians Miss

A common pattern looks like this. The visa is approved, the mover signs a U.S. lease, opens new bank accounts, and starts work. Months later, the actual problem appears. The Canadian departure return was not planned properly, the first-year U.S. return does not line up with the Canadian filing position, and an account that seemed harmless creates avoidable reporting trouble.

For many Canadians, the expensive part of the move is not the immigration filing. It is the tax and compliance work that should have been done before the departure date.

A move to the U.S. can trigger a Canadian deemed disposition. On departure from Canadian tax residency, Canada may treat certain capital assets as if they were sold at fair market value, even though no actual sale took place. That can create immediate tax reporting on unrealized gains.

That rule catches people off guard because the move feels administrative. It is not. The departure date can become a tax event, and once that date passes, the planning options usually get narrower.

What deemed disposition means in plain English

The practical question is simple. What do you own on the day you stop being a Canadian tax resident, and what is each asset worth on that date?

That review often includes:

- Non-registered investment accounts with accrued gains

- Private company shares

- Interests in family businesses or holding companies

- Real estate outside the principal residence analysis

- Trust interests or other less obvious ownership positions

The work is not just valuation. It is coordination. The Canadian departure return, the opening U.S. tax year, brokerage records, and residency position should all tell the same story.

I have seen clients focus heavily on obtaining U.S. status and leave tax records for later. Later usually means rebuilding account values, tracing residency dates, and explaining inconsistent filings after the fact. That is harder, slower, and more expensive than doing the work before the move.

Do I need to pay taxes in both Canada and US after moving

Often, yes, at least in the first year. The first year is usually the most technical because both countries may have a claim to part of the timeline.

Residence, source of income, payroll setup, investment income, and account reporting all matter. The Canada-U.S. tax treaty can reduce double taxation in many cases, but it does not fix missed elections, poor recordkeeping, or a departure date that was never documented properly.

That is the point many relocation guides miss. A treaty helps allocate taxing rights. It does not clean up a file that was assembled backwards.

TFSA and RRSP planning

Registered accounts do not all behave the same way after a move.

- TFSAs often become inefficient or problematic once the holder is U.S. tax resident, and they should be reviewed before departure

- RRSPs are usually more workable, but they still require proper reporting and planning

- Principal residence timing can affect Canadian tax treatment, so sale timing should be reviewed before the move date if a sale is being considered

Business owners need an even wider review. A move can shift not only personal residency, but also management location, signing authority, payroll obligations, and filing exposure for both entities and individuals. On business-owner files, that matters even more when immigration strategy, corporate restructuring, and beneficial ownership reporting requirements all overlap.

Employee transfer versus founder move

The tax profile of an employee transfer is usually narrower. The main issues are residency timing, compensation, payroll withholding, account review, and making sure employer reporting matches the immigration plan.

A founder move is usually more complicated. The founder may be changing personal residence while also moving management functions, opening or using a U.S. entity, and creating new reporting duties tied to ownership and control. That can affect where the company is managed, how intercompany payments are handled, and which records need to exist before the move happens.

These files go wrong when each advisor looks at only one slice of the problem. Immigration, tax, and corporate compliance should be planned as one sequence, with the move date as the anchor.

Moving Your Business or Starting a New US Venture

A common fact pattern looks fine on the surface. A Canadian founder forms a Delaware or Florida company, opens a U.S. bank account, starts pitching customers, and books a flight south. Six months later, the visa case is under pressure, the Canadian company still has decision-making centered in Canada, and nobody has mapped the tax cost of shifting operations or ownership. That is how a business move turns into an expensive cleanup exercise.

The better approach is to decide early whether this is an employee transfer into a real U.S. operation or a founder-led expansion that needs a new entity, new governance, and a tax plan that matches the immigration strategy.

If you are transferring an employee

Employee transfers work best when the business facts were in place before the transfer request. Officers and tax authorities both look for substance. They want to see a genuine corporate relationship, real job duties, and a U.S. operation that can support the role being described.

Review these points before filing or relocating:

- Ownership and control of the Canadian and U.S. entities

- The employee's role abroad and intended role in the U.S.

- Who supervises the employee after entry

- Whether the U.S. company has premises, revenue, contracts, or staff

- Payroll setup, state registration, and I-9 onboarding readiness

The weak files usually have the same problem. The documents say "U.S. expansion," but the U.S. company exists only on paper. That can hurt the visa case and create tax questions about where management sits and which company is carrying the business activity.

If you are moving as a founder

A founder move carries more legal and tax friction because the person and the business are often moving at the same time. If the founder remains the decision-maker for the Canadian company while building the U.S. company, the move can affect corporate residence issues, intercompany pricing, payroll, and reporting tied to ownership.

Start with the operating facts, not the visa form.

A practical founder checklist includes:

- Choosing the right state and entity type for the business model

- Getting EIN, banking, accounting, and payment systems in place

- Documenting capitalization and source of funds

- Setting up contracts, office space, or another credible operating footprint

- Preparing a hiring, sales, or service-delivery plan that matches the immigration filing

- Reviewing whether the move changes control, signing authority, or tax residency positions

The business record has to make sense from every angle. If you are applying under E-2, the investment trail and operating plan need to be credible. If you are using L-1, the ownership structure, managerial role, and relationship between entities need to hold up under close review. In both cases, sloppiness on the corporate side often creates trouble long after the border admission or visa approval.

I often tell founders the same thing. A U.S. company is not just a visa vehicle. It is a taxpaying, reportable business with state law duties, banking scrutiny, and records that need to match what was filed with immigration. If that work is done in the right order, the move is easier to defend and cheaper to maintain.

Frequently Asked Questions

How much does it cost to move from Canada to the US

Costs split into two buckets. The visible costs are filing fees, legal fees, travel, shipping, and housing deposits. The less visible costs are often larger: pre-move tax planning, investment account cleanup, corporate restructuring, and fixing mistakes made after the move date.

I do not quote a flat number without the facts. A TN employee with clean paperwork is a different file from a founder relocating with a Canadian corporation, stock holdings, and family members. Build your budget around the full move, not just the visa application.

Can I keep my Canadian bank accounts

Usually, yes.

The primary issue is reporting and tax treatment. Once U.S. residency starts, the account may trigger U.S. disclosure rules, and some Canadian accounts or funds stop being tax-efficient from a U.S. perspective. I regularly see clients focus on keeping the account open and miss the more important question: whether the account should still be held in the same form after the move.

Update your residency status with the institution, review any registered or non-registered investment holdings, and do it before your departure date if possible.

How long can I stay in the US as a visitor before I move

Visitor entry is for temporary visits. It does not authorize employment, and it is a poor fit for someone who is effectively relocating in stages.

The practical risk is at the border. If an officer sees a one-way moving pattern, job-related activity, or documents suggesting you are setting up residence without the right status, the conversation changes quickly. If you are entering as a visitor before a later move, keep the purpose of that trip narrow, temporary, and well documented.

What happens to my Canadian credit score

Your Canadian credit file does not usually follow you into the U.S. in a way that solves day-to-day problems. Landlords, lenders, and utilities often want a U.S. credit history.

Start early if you can. Ask your bank about cross-border banking products, credit card options, and what identification and immigration documents they will need. That planning can make the first few months in the U.S. much easier.

Which matters more, the visa or the tax planning

They matter at different stages, and both can become expensive in different ways.

A visa issue can delay or stop the move. A tax issue can surface months later, after accounts, investments, or a business structure have already created filing exposure. For Canadians, the common trap is treating the move as an immigration file and only later discovering departure tax issues, deemed disposition consequences, U.S. reporting obligations, or conflicts between personal residence and corporate control.

The better approach is to line up immigration timing, tax residency analysis, account review, and business records before the move date. That is how the move stays defensible and manageable after you arrive.

Conclusion

A successful move from Canada to the USA isn't just an immigration project. It's a coordinated legal, tax, and documentation exercise. The people who handle it well usually start earlier than they think they need to, especially on tax residency, account review, and business records. If you already have an offer, a transfer plan, or a U.S. launch in motion, now is the time to line up the file before small errors become expensive ones.

If you're planning a cross-border move and want the legal and tax issues reviewed together, Mayo Law works on U.S.-Canada immigration, business, and compliance matters for individuals, founders, and employers.

How Mayo Law Can Help

Cross-border moves fail in predictable places. A visa is filed without reviewing Canadian departure tax exposure. A founder incorporates in the U.S. before cleaning up share records in Canada. An employee starts work stateside while payroll, residency, and account reporting are still set up for the old structure.

Mayo Law helps clients line up those moving parts before they create avoidable cost. That work often includes immigration strategy, timing around Canadian and U.S. tax residency, document review for border and consular filings, and business structuring questions for founders and employers.

The practical benefit is coordination. One plan. Fewer surprises.

Clients usually need help deciding not just which application to file, but when to file, what to fix first, and which tax or corporate steps should happen before the move date. That is where legal judgment matters most. Timing errors can trigger penalties, filing problems, or a tax result that is hard to reverse once the move is underway.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles