You’re building product, chasing customers, and trying not to waste cash. Then a legal issue lands on your desk that isn’t really a Google problem. It’s a founder equity split, a contractor who wrote core code, a customer pushing its own paper, or a U.S. investor asking what entity you formed and why.

That’s usually the moment founders start asking whether they need a startup business attorney now, or whether legal work can wait until the company is “real.” The hard truth is that some legal tasks can wait, and some absolutely should not. The mistake is treating all legal work as equally urgent, or equally optional.

At Mayo Law, we help founders in Toronto, the GTA, and across the border handle business issues that often touch both Canada and the United States. If your team, investors, IP, or customers span both countries, the right legal decisions early can prevent expensive cleanup later.

Published: June 1, 2026

Updated: June 1, 2026

Read time: 14 minutes

What Does a Startup Business Attorney Do?

A startup business attorney is a lawyer who helps founders make early legal decisions that affect ownership, financing, contracts, hiring, compliance, and exit value. The job isn’t just filing incorporation papers. It’s building legal structure around the business so investors, customers, and buyers can rely on what the company says it owns and how it operates.

A general business lawyer may be perfectly capable on ordinary commercial matters. A startup lawyer, though, usually sees the same pressure points repeatedly. Founder departures. Dirty cap tables. Missing IP assignments. Early financing documents that didn’t match the actual deal. Terms of service copied from another company. Those are not rare edge cases.

In the United States, the broader business lawyers and attorneys industry was estimated at $191.8 billion in 2024, with about 277,000 businesses in 2025 and projected 1.2% CAGR over 2020 to 2025 according to IBISWorld’s business lawyers and attorneys industry data. That matters because startup legal work sits inside a very large professional market built around formation, contracts, compliance, and transactions. It isn’t an administrative afterthought.

The proactive side of the job

Good startup counsel does preventive work before the problem becomes visible. That usually includes:

- Entity choices: corporation, LLC, or another structure based on funding, tax, and governance goals

- Founder arrangements: who owns what, vesting, departures, decision rights, and transfer limits

- IP ownership: ensuring the company owns code, branding, inventions, and work product

- Core contracts: customer paper, vendor terms, contractor agreements, NDAs, and employment documents

- Governance documents: bylaws, resolutions, and records that support later diligence

If you’re fuzzy on corporate housekeeping, then documents like company bylaws stop being theory and start becoming fundraising infrastructure.

Practical rule: If the issue affects ownership, control, or IP title, handle it early. Those are the areas that tend to get more expensive, not cheaper, with time.

The reactive side of the job

A startup attorney also solves live business problems. A customer sends procurement terms. A founder moves to another country. A former contractor claims rights in code. A new investor asks for cleanup before wiring funds. A regulator asks questions about privacy or marketing.

That work is still legal, but it’s also operational. The lawyer isn’t there just to say no. The lawyer is there to help you close the deal without creating damage somewhere else.

What founders often misunderstand

Founders often think legal work starts when outside money arrives. In practice, many of the highest-risk issues arise before the first institutional investor appears. By the time diligence starts, the legal work is no longer just planning. It becomes repair.

When to Hire Your First Startup Attorney

The right question isn’t “Do startups need a lawyer?” The better question is when is legal spending worth it.

Independent legal-access guidance highlights that founders often want cost-sensitive answers on whether counsel is necessary pre-incorporation, especially where the highest-risk issues are ownership splits, IP assignment, cap table hygiene, contractor classification, and cross-border tax or entity choices. Those issues can be hard to unwind later, as reflected in LAFLA’s small business program guidance.

Before incorporation

Founders often find themselves most tempted to save money. Sometimes that’s reasonable. If you’re still testing an idea alone and haven’t written meaningful code, taken money, or signed real contracts, you may not need full legal buildout yet.

But pre-incorporation is not a free zone.

You should usually pause and get legal advice if any of these are true:

- You have co-founders: equity promises made casually are hard to reinterpret later

- Someone is building core IP: code, designs, or data assets need clear ownership

- You’re using contractors: contractor work does not automatically equal company ownership

- You’re crossing borders: a Canadian founder using a U.S. entity, or the reverse, can create tax and governance issues

- You’re raising even informal money: “friends and family” money still needs structure

A common failure pattern is simple. Two founders agree on a split over text. One leaves after a few months. No vesting. No repurchase rights. No documented IP assignment. The business survives, but the legal risk sits there for years.

At incorporation

This is usually the first real legal trigger.

You don’t want to pick an entity by copying what another founder did on social media. The right structure depends on your financing path, ownership plan, future hires, and where the people and business activity are.

For U.S.-Canada startups, incorporation decisions can create problems in both countries. Founders often assume they can “fix it later” if they choose the wrong entity or wrong jurisdiction. Sometimes they can. Often they can only fix it by spending more and disrupting cap table, tax, or governance planning.

Founders should think of incorporation as architecture, not paperwork. Cheap architecture can become expensive demolition.

Before your first hire or contractor

Hiring is another point where DIY habits create avoidable risk.

Founders often pull a template offer letter and move on. However, the issues are broader:

- who owns work product

- what confidentiality obligations apply

- whether the person is properly classified

- whether the company can restrict use of confidential information

- how equity or options are documented

This matters even more if a contractor is building your product before launch. If your company can’t show clean assignment of rights, that issue tends to surface at the worst time.

Before seeking outside investment

Investors care about traction, but they also care about legal reliability. If the company can’t show who owns the shares, who approved the issuance, whether IP sits in the company, and whether earlier agreements were properly documented, financing gets slower and more expensive.

That doesn’t mean every startup needs a full legal team before a seed round. It means you want your core house in order before the first serious diligence request arrives.

U.S.-Canada triggers that justify earlier advice

Cross-border startups need counsel earlier than purely domestic ones. That’s because a routine question in one country can create a second issue in the other.

Typical triggers include:

| Situation | Why it matters early |

|---|---|

| Canadian founder forming a U.S. company | Entity and tax consequences may not line up with founder assumptions |

| U.S. founder hiring in Canada | Employment, contractor, and payroll treatment differ |

| Team split across both countries | IP ownership and governing law need consistency |

| U.S. market entry by a Canadian startup | Contracts, privacy, and immigration may overlap |

| Key founder or executive relocating | Immigration planning can affect corporate timing |

If your startup has one foot in each country, legal timing matters more than legal volume. You don't always need more documents. You need the right documents earlier.

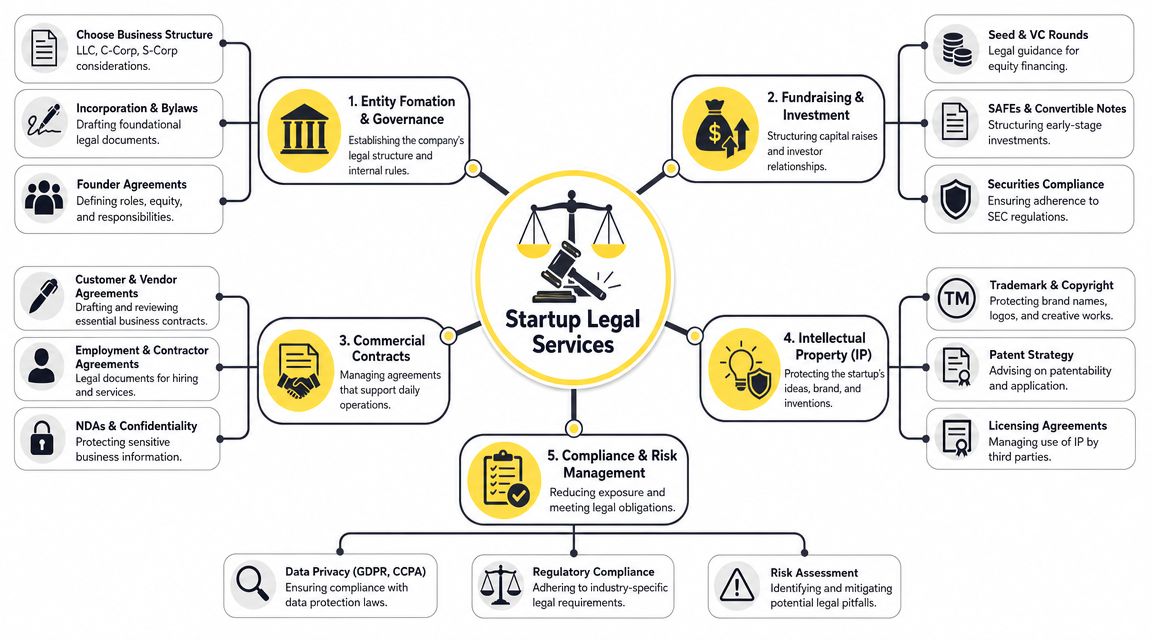

Key Legal Services Your Startup Will Need

A startup does not need every legal service at once. It does need the right legal work before a mistake becomes expensive to reverse.

For most founders, the spending question is simple. Which issues create a real risk to ownership, revenue, financing, or cross-border operations if you wait another three to six months? That is where legal budget should go first.

Entity formation and governance

Formation documents are cheap compared with fixing cap table problems later.

This work covers the company structure, founder approvals, share issuances, board or shareholder consents, and recordkeeping. Founders often treat these as paperwork. Buyers, investors, and later counsel treat them as proof. If the records do not match what everyone thought happened, the company may need consents, corrective issuances, or tax review before a deal can close.

For U.S.-Canada startups, governance errors also travel badly across borders. A Canadian founder in a Delaware company may assume an informal agreement is enough. It usually is not.

Intellectual property protection

IP is usually the first area where DIY legal work creates a six-figure problem.

If the company cannot show a clean chain of title to its code, brand, content, product designs, or data rights, investors discount value or ask for cleanup before funding. Acquirers do the same. In practice, that means delays, a weaker bargaining position in negotiations, and legal bills that are much higher than the cost of getting assignments and development terms right at the start.

The risk is highest when work was created before incorporation, by contractors, through foreign affiliates, or by a team split between the U.S. and Canada. Ownership does not automatically end up where founders expect it to.

If your product includes licensed software, white-labeled tools, or shared technical assets, technology licensing agreements should be reviewed before the first major customer contract. That is usually the point when scope restrictions, sublicensing limits, and ownership carve-outs start to matter in dollars, not theory.

The practical question is narrow. What does the company own outright, what is it licensed to use, and what can it legally sell to customers?

Contracts and commercial agreements

Contracts shape margin and risk.

A startup with poor customer paper can accidentally promise custom work, broad indemnities, aggressive service levels, or data commitments the product cannot support. A weak vendor agreement can leave the company exposed if a key provider fails, raises prices, mishandles data, or claims rights in work product.

Early-stage companies usually need a small set of usable documents, drafted for how the business sells and delivers:

- Customer agreement for SaaS, services, pilots, or implementation work

- Vendor agreement where third parties support infrastructure, development, or data processing

- NDA and confidentiality terms that fit the actual sales and hiring process

- Contractor and advisor agreements with clear deliverables, confidentiality, and IP assignment

This is not about having more paper. It is about having paper that matches the business model.

Fundraising and securities compliance

The legal spend here should track the financing instrument and the number of people involved.

A simple founder loan or a small friends-and-family round usually needs less work than a priced equity round with multiple investors and side letters. But even an informal raise can create securities issues, disclosure risk, and cap table problems if documents are incomplete or terms are copied from another company.

Counsel adds value here by cleaning up authorizations, checking prior issuances, aligning investor documents, and spotting terms that look harmless but affect control or dilution later. Founders who defer this work often pay for it during diligence, when the timing is worst and the negotiating power is lowest. If you want to confirm current U.S. securities rules, the U.S. Securities and Exchange Commission is the primary reference point.

Employment and contractor matters

Many founders overspend on formation and underspend on hiring documents. That is backwards.

A contractor agreement with no invention assignment can put product ownership at risk. An offer letter copied from a U.S. template can create problems if the hire works in Canada. Equity promises made in Slack or email can become disputes about what was granted, when it vested, and who approved it.

The legal priority here is straightforward. Match the document to the relationship. If someone functions like an employee, treat that issue seriously. If someone is building core product, protect ownership and confidentiality before work starts.

Regulatory compliance and privacy

Some compliance work can wait. Some cannot.

If the company handles personal information, operates in fintech, health, AI, or other regulated fields, or sells across multiple jurisdictions, legal review belongs early in the budget. Privacy policies, data terms, marketing claims, and onboarding flows often create obligations before the startup has internal systems to meet them. For U.S.-Canada companies, this gets more complicated because customer data, employee data, and vendor access may involve both countries at the same time.

The practical decision is whether the legal issue blocks revenue, creates penalty exposure, or will surface in enterprise diligence. If the answer is yes, deferral is usually false economy.

Disputes and founder fallout

Founders rarely ask for dispute planning until a relationship is already failing.

A good startup attorney addresses that risk in the original documents. Vesting terms, exit mechanics, confidentiality obligations, decision rights, and dispute provisions give the company options if a founder leaves, a contractor claims ownership, or a commercial relationship breaks down. Those clauses do not prevent every conflict. They do reduce the odds that a business problem turns into a lawsuit.

If legal budget is tight, spend it first on the issues that are hardest to unwind later: IP ownership, equity records, commercial contracts tied to revenue, and any cross-border employment or compliance issue. Those are the areas where a short delay can become a costly repair project.

Understanding Startup Legal Costs and Pricing

Founders don't just worry about legal cost. They worry about unpredictable legal cost. That concern is legitimate.

The most useful pricing conversation is not “What's your hourly rate?” It's “For this stage of company, what work is fixed, what work is variable, and what events will increase cost?”

Why startup legal work often costs more than founders expect

Legal advice is a skilled service. In the U.S., the Bureau of Labor Statistics reported a median annual wage of $151,160 for lawyers in May 2024, with employment projected to grow 4% from 2024 to 2034 and about 31,500 openings per year on average. Clio's 2025 legal profession data also reported more than 1.37 million lawyers in the United States, with New York home to 190,015 lawyers and California to 181,048, according to Clio's lawyer statistics summary. That helps explain why specialized startup counsel in major business hubs often commands premium rates.

You're not paying only for time. You're paying for judgment on issues that can affect ownership, financing, and exit readiness.

Common pricing models

Here's how startup legal pricing usually works in practice:

| Pricing model | Best for | Watch for |

|---|---|---|

| Hourly | Negotiations, disputes, open-ended advisory work | Scope creep if the task isn’t defined |

| Flat fee | Incorporation, basic founder documents, trademark filings | What’s excluded from the package |

| Monthly retainer | Ongoing outside general counsel support | Whether unused time rolls over |

| Deferred or staged fees | Some early-stage financing contexts | Trigger dates and repayment terms |

Questions founders should ask before signing

- What exactly is included? Ask for deliverables, not labels.

- What usually increases the bill? Opposing counsel changes, investor revisions, and cross-border tax input often do.

- Who will do the work? Founders should know whether they'll deal with a partner, associate, or a mixed team.

- What assumptions are built into the quote? Many “formation packages” assume a simple cap table and no cross-border issues.

If you're comparing incorporation options, practical cost questions often connect back to process. Founders sorting through early setup issues may also find it helpful to understand how to incorporate a business in Ontario before they compare legal quotes.

A low quote can still be expensive if it leaves out the one issue that later blocks financing.

What works and what doesn't

What works is scoped legal work tied to a business milestone. Incorporation. Founder cleanup. First enterprise contract. Seed round prep.

What doesn't work is vague “general startup support” with no defined outputs. That's where founders lose confidence and lawyers end up reacting instead of planning.

For early-stage companies, legal budgeting is easiest when you treat counsel like any other strategic vendor. Define the job, define the assumptions, and define the trigger for the next spend.

How to Find and Hire the Right Attorney

You are about to sign your first real enterprise customer, and the other side asks for proof that the company owns its code, has authority to enter the contract, and can invoice from the right entity. If your co-founder is in Toronto, your contractor is in California, and the parent company is still undecided, hiring the wrong lawyer costs more than the legal bill. It can delay revenue, force document cleanup under pressure, and expose problems that should have been fixed before anyone started diligence.

The right attorney helps you decide what must be done now, what can wait, and what is cheap to fix today but expensive to repair after a financing round, acquisition review, or cross-border tax restructure.

Five things to test in the first call

Startup fluency

Ask what they handle every month for early-stage companies. Founder equity, IP assignment, advisor grants, SAFEs or notes, customer contracts, and board approvals should not sound exotic to startup counsel. A lawyer can be excellent for owner-operated businesses and still be a poor fit for venture-backed or cross-border startup work.

Industry understanding

The legal work should match the business model. SaaS companies usually need clean IP ownership, data terms, and contract flow. Consumer brands often hit marketing, product, and supply chain issues earlier. Health, fintech, and regulated products have another layer of approvals and risk allocation. You are not paying for a lecture on your industry. You are paying for faster issue spotting.

Cross-border competence

For U.S.-Canada startups, this is often where founders either save money or waste it. Ask how the lawyer handles Canadian founders using a Delaware company, U.S. hires working for a Canadian entity, or IP built in one country and commercialized in the other. If the answer is “we'll figure that out later,” expect duplicated work, tax input added late, and documents that need to be redone. Founders comparing those structures should look for an international business lawyer who can explain the trade-offs in plain business terms.

Pricing discipline

Good startup counsel can rank issues. They should be able to say, “Fix IP ownership this month. Clean up the cap table before fundraising. Defer the full privacy overhaul until you have the right data volume or customer profile.” If every issue is presented at the same level of urgency, budgeting gets harder and legal advice becomes less useful.

Communication style

Founders need clear recommendations, not a memo that avoids taking a position. Ask how they usually deliver advice. A short email with options, cost ranges, and a recommended path is often more useful than a long analysis with no conclusion.

Questions worth asking

Use the first meeting to test judgment, not just credentials.

- What legal issue would you check first if you expected us to raise money in the next 12 months?

- Which documents do you want to see before giving advice?

- What can wait until we hit revenue, headcount, or fundraising milestones?

- Where do U.S.-Canada startups usually spend legal fees too early?

- What is the one issue you would not let us handle ourselves?

- If another specialist is needed, tax, employment, immigration, privacy, who makes that call and when?

Those answers tell you whether the lawyer understands sequencing. That matters. A founder who spends a few thousand dollars early to paper IP assignments and founder equity usually avoids a much larger cleanup bill later. The opposite is also true. Deferring the wrong issue can hold up diligence, diminish their bargaining power, or force awkward disclosures when investors are already reviewing the company.

Mayo Law works with businesses across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, which can help founders with U.S. ties coordinate business counsel more efficiently at an early stage.

Red flags founders should take seriously

Some problems show up in the first conversation.

- No questions about ownership or IP. For a startup, that is often the first diligence file anyone will request.

- No effort to understand the cap table. If equity is already messy, every future step gets harder.

- Advice without jurisdiction questions. U.S. and Canadian facts change the answer.

- Vague scope and vague billing. That usually turns a modest project into an open-ended one.

- Purely reactive advice. Startups need counsel who can spot the next issue before it becomes expensive.

The best attorney for an early-stage company is rarely the one with the broadest pitch. It is the one who can say, with reasons, where legal spend protects enterprise value and where deferral is still safe.

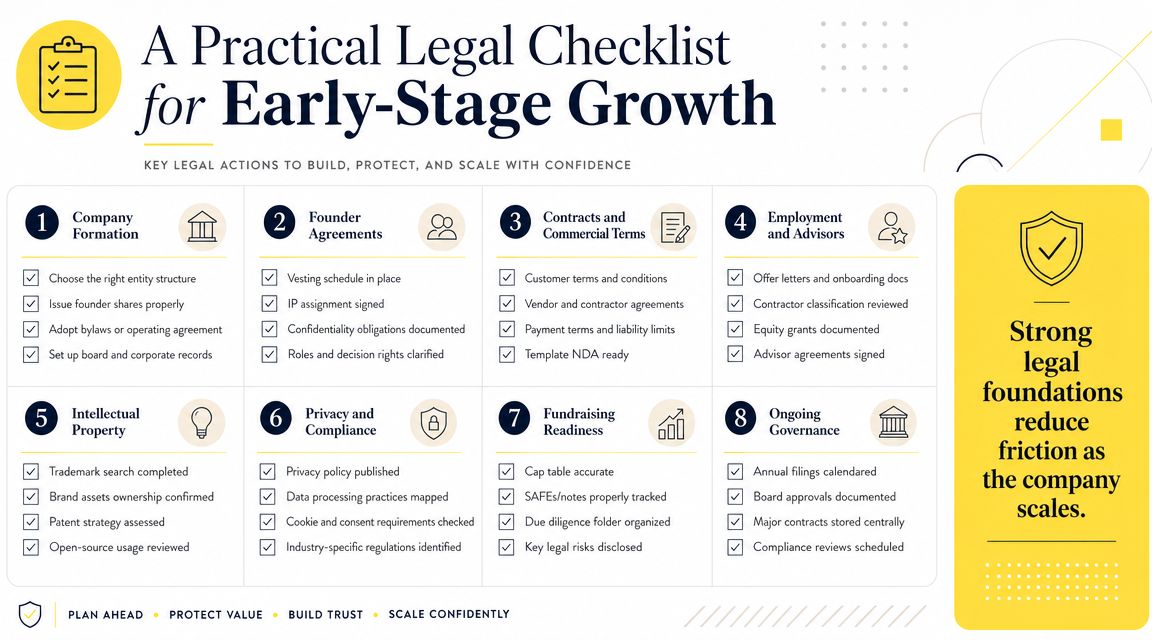

A Practical Legal Checklist for Early-Stage Growth

Founders usually need a checklist more than a lecture. The sequence below is the one that tends to matter most in practice.

Stage one formation

Use this stage to lock down ownership and structure.

- Choose the right entity: base it on funding path, governance, and where the business operates

- Sign founder agreements: cover roles, equity, vesting, decision-making, and exits

- Issue equity properly: don't rely on informal promises

- Assign IP to the company: founders, employees, and contractors should all be covered

- Adopt governance documents: resolutions, consents, and internal records matter later

If equity is being sold or transferred among founders or early participants, documents such as stock purchase agreements need to match the actual ownership deal, not a recycled template from another company.

Stage two operations

At this stage, the startup begins to function as a company, not just a project.

A practical operating file should include a standard customer agreement, vendor terms where needed, confidentiality provisions, hiring templates, and a basic privacy framework that matches the product and sales process. Not every company needs the same stack. Every company needs internal consistency.

Early-stage legal work should make routine activity repeatable. If every new customer or hire requires reinvention, the legal setup is incomplete.

Stage three growth and hiring

Once headcount and revenue start moving, small drafting choices become system problems.

Check these items:

- Employment and contractor templates: update them before scaling usage

- Equity documentation: make sure promises and paperwork match

- Data and security commitments: align sales language with actual practices

- Commercial review process: decide who can approve non-standard terms

- Authority rules: define who can sign what on behalf of the company

A startup with ten ad hoc contract variants and no approval rule creates its own legal friction.

Stage four fundraising or exit preparation

This is the cleanup stage that works best when it's light, not massive.

Review:

| Item | Why it matters |

|---|---|

| Cap table hygiene | Investors and buyers need clear ownership records |

| IP chain of title | Core assets must sit with the company |

| Signed founder and contractor papers | Missing documents slow diligence |

| Board and shareholder approvals | Issuances and major actions need support |

| Key commercial contracts | Revenue assumptions depend on enforceable terms |

Two anonymized examples show the difference.

A software startup waited until a financing process to collect contractor IP assignments. One contractor had disappeared, one wanted payment to sign, and one had worked through another entity. The company still raised money, but not on the original timing.

Another founder team documented vesting, assignments, and approvals early. Their legal diligence wasn't perfect, but it was coherent. The financing process stayed focused on business terms instead of ownership repair.

For most startups, this checklist maps closely to the core legal scope identified by startup counsel guidance: formation, contracts, IP, employment agreements, and compliance. Those are the areas that reduce liability and improve investor readiness.

If you're building across Canada and the United States, legal timing matters as much as legal substance. A startup that gets ownership, IP, and cross-border structure right early usually has more room to move later. Mayo Law advises founders on business, compliance, immigration, and cross-border legal issues that often overlap in early-stage growth.

Frequently Asked Questions

What is a startup business attorney?

A startup business attorney is a lawyer who helps founders with the legal work most likely to affect ownership, financing, contracts, hiring, compliance, and exit value. That usually includes entity formation, founder arrangements, IP assignment, commercial contracts, and fundraising preparation. The role is less about filing forms and more about preventing business-critical mistakes.

Do I need a startup business attorney before I incorporate?

Sometimes yes. If you have co-founders, contractors building core product, informal equity promises, or a U.S.-Canada structure question, getting legal advice before incorporation is often money well spent. If you're still testing an idea alone and haven't created meaningful assets or obligations, some work can wait. The key is whether delay creates ownership or IP risk.

How much does a startup business attorney cost?

There isn't one standard price because cost depends on scope, urgency, and complexity. Founders usually see hourly billing, flat fees for defined projects, monthly retainers for ongoing support, or staged arrangements in limited contexts. The most useful question isn't just price. It's what the quote includes, what assumptions it makes, and what events will increase the bill.

How long does startup legal setup usually take?

Simple formation and core founder documents can move quickly if the facts are clean and everyone signs promptly. Timing gets longer when there are multiple founders, prior side projects, existing contractors, foreign ownership issues, or pending investor deadlines. The delay usually comes from gathering facts and fixing inconsistencies, not from drafting alone.

Can one lawyer handle both U.S. and Canada startup issues?

Sometimes one lawyer or one coordinated firm can handle a substantial part of the work, especially where the lawyer is licensed or works across both systems. In other cases, tax, employment, or securities questions may still require additional local input. What matters is coordination. Cross-border startups get into trouble when each advisor sees only one country and no one owns the whole picture.

What's the biggest legal risk for early-stage founders?

It's usually not the thing founders expect. The biggest risks are often unclear equity ownership, missing IP assignments, poor contractor documentation, and inconsistent corporate records. Those problems don't always hurt immediately. They show up when a founder leaves, an investor starts diligence, or a buyer asks the company to prove it owns what it's selling.

Conclusion

If you're trying to decide whether legal spend is premature, don't treat the answer as all or nothing. Some startup legal work can wait. The parts tied to ownership, IP, cross-border structure, and financing readiness usually should not. The right startup business attorney helps you spend at the right moments, on the right issues, before a fix becomes a negotiation.

How Mayo Law Can Help

A common call comes after the preventable mistake. A Canadian founder signs a contractor in the U.S. without clear IP assignment language, then a financing diligence request exposes the gap. Another team incorporates on one side of the border, hires on the other, and learns too late that tax, employment, and immigration questions do not stay neatly separated.

Mayo Law advises startups on the points where legal cost usually has the highest payoff early on: entity structure, founder and contractor agreements, IP ownership, commercial contracts, cross-border expansion, and U.S.-Canada coordination. The focus is practical. What needs to be done now, what can wait, and what becomes more expensive if deferred.

That matters most for founders operating across Canada and the U.S., where one business decision can trigger legal issues in multiple jurisdictions at once.

If your startup is weighing whether to spend on legal help now or postpone it, Mayo Law can help you assess the risk, scope the work, and prioritize the items that protect ownership, financing readiness, and your ability to keep operating without avoidable legal cleanup later.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

Founders dealing with U.S.-Canada hiring, founder relocation, or compliance usually face the same question that comes up throughout this article. Which legal issue can wait, and which one gets expensive if you guess wrong?

These articles cover adjacent problems that tend to justify earlier legal spend because the downside of delay is high.

- E-2 visa lawyer

- Compliance legal services