Published: June 24, 2026

Updated: June 24, 2026

Read time: 11 minutes

A financing gap often appears at the worst possible moment. A company is ready to buy a competitor, launch in the other country, or close an asset-backed deal, but the senior lender will not extend more credit and the founders do not want to give up more equity than the deal justifies. Mezzanine financing often fills that gap.

In U.S.-Canada transactions, the structure deserves more care than many sponsors expect. The documents may be governed by New York law, the borrower may be a Canadian entity, the collateral package may involve shares rather than hard assets, and enforcement expectations can look different depending on which side of the border is involved. For businesses setting up cross-border deals, contracts, and financing terms, the legal framework should be addressed early through experienced international business counsel.

The practical question is whether mezzanine debt fits your cash flow, control concerns, senior lender restrictions, and enforcement risk in both countries. Used with discipline, it can close a real capital shortfall without immediate dilution. Used casually, it can become expensive capital that narrows flexibility and increases the risk of losing control if the deal underperforms.

What Is a Mezzanine Loan?

A mezzanine loan is a hybrid form of capital that blends debt and equity features. Technically, it is subordinate debt financing secured by a pledge of the borrower’s direct or indirect equity interest in the entity that owns the asset, rather than a lien on the physical property itself, as described in Cornell Law’s overview of mezzanine financing. It often gets compared to instruments discussed in preferred stock terms.

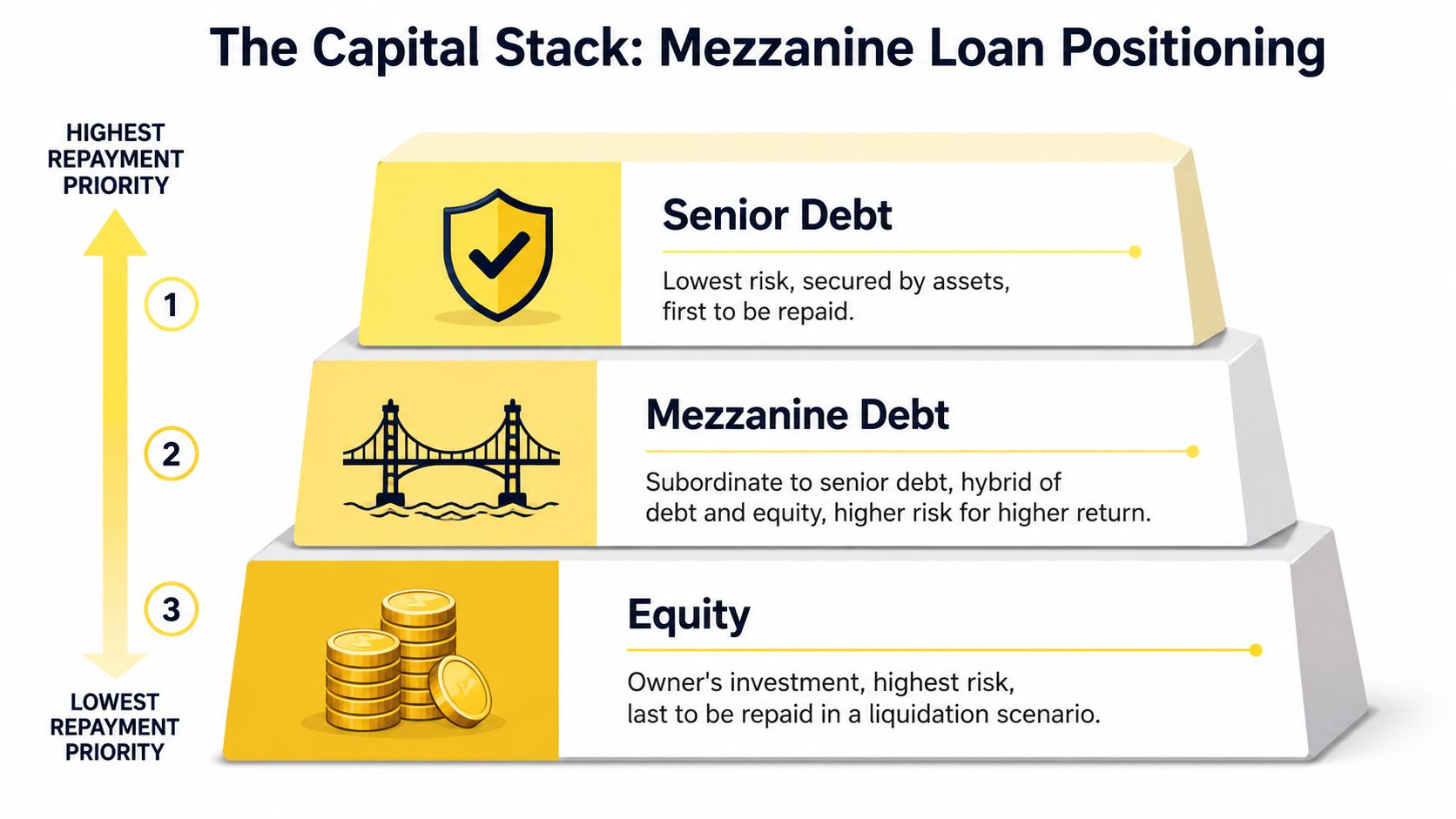

Where Mezzanine Loans Sit in the Capital Stack

When lawyers and lenders talk about the capital stack, they mean the order in which money sits in a deal and the order in which parties get paid if things go wrong. Mezzanine debt sits between senior debt and equity. That middle position is the entire point.

Why this position matters

Senior lenders get paid first. Equity holders get paid last. Mezzanine lenders sit in between, which means they take more risk than the bank but less than the owners. That risk explains the pricing and the lender protections that usually come with the deal.

According to Crestmont Capital’s explanation of mezzanine financing, mezzanine loan interest rates typically range from 12% to 20% annually, while traditional senior bank loans often carry rates of 6% to 9%. The same source notes that mezzanine instruments frequently account for 10% to 20% of a deal’s total capital structure in debt-financed buyouts.

What the stack looks like in practice

A useful mental model is a waterfall.

- Senior debt first: The bank or senior secured lender gets paid before everyone else.

- Mezzanine next: The mezz lender gets paid only after senior debt is satisfied.

- Preferred or common equity last: Owners and investors take the residual value, if any remains.

This ranking becomes very real in distress. Because mezzanine debt is subordinate, the lender may recover little or nothing if the asset value only covers senior debt.

Practical rule: If a transaction only works when everything goes right, mezzanine debt usually adds more fragility than value.

Why founders and CFOs should care

This isn’t just a lender issue. The capital stack affects your covenants, your flexibility, and your downside. A cheaper senior loan may come with tighter advance limits. A mezzanine layer may close the gap, but it can also add consent rights, reporting burdens, and equity-linked economics that feel a lot like partial dilution.

For many cross-border companies, mezzanine financing is attractive because it preserves ownership better than a pure equity raise. But it doesn’t preserve control for free.

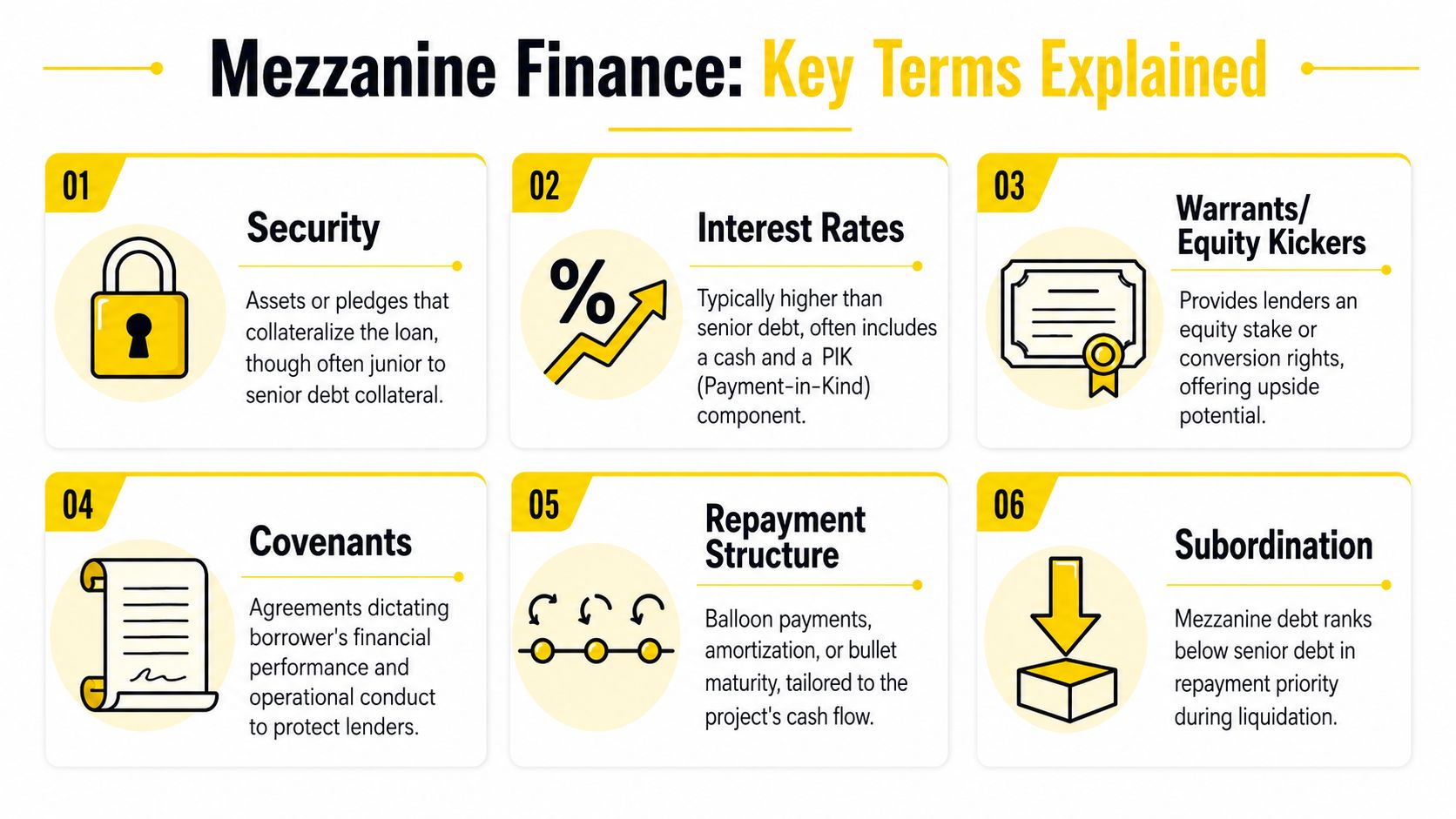

Key Economic and Legal Terms of Mezzanine Finance

The legal documents matter as much as the pricing. A borrower can agree to a workable coupon and still end up boxed in by security mechanics, consent rights, or intercreditor restrictions.

Security

A mezzanine loan is typically secured by an equity pledge, not by a direct mortgage or lien on the property itself. In plain English, the lender takes security over the shares, membership interests, or similar ownership interests in the entity that owns the asset or operating business.

That distinction changes the enforcement path. The lender doesn’t immediately foreclose on the building, project, or business assets in the same way a senior secured creditor might. Instead, the lender enforces against the ownership layer and tries to take control of the entity.

For founders, that means a default can become a control event faster than they expect. For lenders, it means the collateral package must be documented with precision.

Intercreditor agreements

An intercreditor agreement governs the relationship between the senior lender and the mezzanine lender. It addresses priority, notice rights, cure rights, standstill periods, and what each lender can or can’t do after a default.

This document is not boilerplate. The verified data notes that mezzanine structures commonly require a mandatory intercreditor agreement between the senior lender and the mezzanine lender, and that such agreements are often a prerequisite in some government-backed financing contexts. If the intercreditor terms are weak, the mezzanine lender may have very little practical power. If they’re too aggressive, the senior lender may block the entire structure.

The negotiation often turns less on theory and more on who gets to act first, who gets notice, and who can stop a sale.

Interest and PIK

Mezzanine financing is often interest-only, with no amortization before maturity. According to Prudential Private Capital’s discussion of mezzanine financing, these loans often extend up to 7–8 years and frequently combine cash interest with Paid-in-Kind (PIK) interest, which gets added to principal instead of being paid currently.

That matters because PIK can make early cash flow easier while increasing the amount owed later. A company may think it’s buying breathing room, but it’s also compounding the final problem if performance doesn’t improve before maturity.

Covenants

Covenants are the promises and restrictions in the loan documents. Some are financial. Others are operational. They may limit additional borrowing, distributions, asset sales, affiliate transactions, management changes, or expansion into new markets without consent.

In practice, mezzanine covenants can become a governance issue. A founder may still own the equity on paper but need lender approval for decisions that would otherwise be routine.

Warrants and equity kickers

Mezzanine lenders often want more than a coupon. The verified data allows this point clearly: lender return can include an equity kicker, such as warrants or a conversion feature, in addition to current cash coupon and possible PIK interest. That lets the lender share in upside if the business performs well.

This is why mezzanine debt is often described as a hybrid. Economically, it can function as expensive debt or cheap equity, depending on the deal mechanics and whether the lender’s upside rights become valuable.

Repayment structure

Most mezzanine debt is built around a later maturity and a larger repayment event at the end, not steady principal paydown. That can work well in an acquisition, recapitalization, or expansion plan where value is expected to increase before refinancing or exit.

It works badly when management hasn’t mapped a realistic takeout. If you can’t identify the probable source of repayment at maturity, the structure is already under stress.

For companies negotiating investor documents alongside debt documents, it’s worth understanding how these rights interact with other financing papers such as an NVCA term sheet.

Mezzanine Loans vs Senior Debt vs Equity

Founders usually compare mezzanine debt against two alternatives. Borrow more from the bank, or raise more equity. In reality, those options produce very different control, pricing, and enforcement outcomes.

Financing comparison

| Feature | Senior Debt | Mezzanine Loan | Equity |

|---|---|---|---|

| Priority of repayment | First in line | Behind senior debt, ahead of equity | Last in line |

| Cost | Lower than mezzanine | Higher than senior debt | No contractual interest, but owners give up upside |

| Security | Direct security over assets is common | Usually secured by pledged equity interests | Ownership interest rather than debt security |

| Lender or investor upside | Limited to agreed loan economics | Coupon plus possible PIK and equity kicker | Full upside tied to business performance |

| Impact on founder control | Can restrict operations through covenants | Can restrict operations and create path to control on default | Dilutes ownership and voting power |

When mezzanine is the least bad option

Mezzanine debt can make sense when senior debt has reached its limit and the owners don't want to issue more equity at the current valuation. In that setting, mezzanine fills the gap while postponing a larger ownership give-up.

The trade is simple. You preserve more equity today, but you accept a higher cost of capital and stricter legal terms.

When equity is still the cleaner answer

If the company needs a long runway, uncertain execution time, or major strategic flexibility, equity may still be safer. It doesn't create a maturity wall. It also doesn't create default risk in the same way debt does.

That said, equity can be the more expensive choice in a strong-performing business, especially if the valuation is low when the capital is raised. That's why many founders spend time studying equity dilution in financing rounds before deciding whether mezzanine debt is worth the pressure.

US-Canada Cross-Border Mezzanine Loan Considerations

Most online explanations are U.S.-centric. That's a problem if your borrower, holding company, lender group, assets, or guarantors sit on both sides of the border.

According to BDC's glossary note on mezzanine financing, 78% of SMEs expanding between the U.S. and Canada face complexity in structuring cross-border financing. That tracks with practice. A U.S. template rarely drops cleanly into a Canadian structure.

Security and perfection

In the United States, lenders often focus on UCC-based perfection and enforcement concepts. In Canada, the analysis usually shifts to provincial personal property security regimes and corporate law mechanics around the pledged interests. If the ownership chain spans both jurisdictions, counsel needs to confirm exactly which entity's equity is being pledged and under which regime perfection happens.

A common mistake is assuming that “shares are shares” and the same filing logic applies everywhere. It doesn't.

Tax treatment and cash flow planning

Cross-border mezzanine debt also raises tax issues around interest deductibility, withholding, and treatment of PIK accruals. The verified data specifically notes divergent rules under Canada's Income Tax Act and the U.S. Internal Revenue Code. Founders shouldn't let those issues wait until year-end.

For baseline government materials, cross-border businesses usually need to review the IRS and the Government of Canada tax resources.

Enforcement risk across borders

The hard part of a distressed mezzanine deal isn't just the paper. It's enforcement. If the collateral package points to equity in one country and the operating assets sit in another, disputes over notice, governance, recognition, and creditor priority can become more expensive very quickly.

A cross-border mezzanine structure should be built for enforcement on day one, not merely for closing day.

Businesses that also use U.S. tax-driven structures sometimes need the financing documents reviewed alongside planning around items such as the Section 250 deduction, because financing terms can affect how the broader structure works in practice.

When to Use a Mezzanine Loan and Key Risks to Manage

The best use cases share one trait. The company has a real path to increased value or a defined exit, but senior debt alone won't carry the transaction.

Scenario one

A Canadian founder wants to acquire a smaller U.S. competitor. The senior lender is willing to lend, but not enough to cover the full purchase price and integration budget. The founder doesn't want to bring in a new equity investor before proving the combined business can scale.

Mezzanine debt can work here because it closes the acquisition gap without immediate common equity dilution. It works only if the post-closing business can support interest payments and refinance later.

Scenario two

A U.S.-based real estate sponsor with Canadian investors needs additional capital above the mortgage level but below a fresh equity round. The sponsor expects a refinance or sale after stabilization.

This is another classic mezzanine use case. The mistake is treating it like “just more debt.” It isn't. The security package, intercreditor terms, and default remedies can alter who controls the project if the business plan slips.

The risks people underestimate

The headline risk is pricing, but that isn't the most dangerous part.

- Control risk: Warrants, conversion rights, and default remedies can shift practical control away from the founders.

- Covenant risk: A loan that looks flexible in the summary may become restrictive in the full documents.

- Exit risk: If there's no realistic refinancing or sale path, maturity becomes a pressure point.

- Enforcement risk: Distress can produce long, expensive fights over who can seize what.

The verified data states that 42% of mezzanine loan defaults in 2024–2025 involved complex foreclosure delays due to unsecured equity pledges and ambiguous LLC governance structures, and that the process can take 18–24 months, according to this SEC filing reference. That should change how borrowers think about “default.” It may not be quick, but it can still be significantly disruptive.

Mayo Law works with founders, investors, and operators across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, so clients with U.S. ties coordinate their legal work in one place rather than juggling two firms.

Frequently Asked Questions

What are typical interest rates for mezzanine loans?

Mezzanine loan interest rates typically range from 12% to 20% annually. According to the verified data from Crestmont Capital, lender return often includes a current cash coupon, often 10% to 14%, plus possible PIK interest and an equity kicker such as warrants or a conversion feature. The exact mix matters more than the stated headline rate.

How long does it take to secure mezzanine financing?

It depends on the deal structure, diligence quality, senior lender cooperation, and whether there is a cross-border element. In practice, the timetable is usually driven by document negotiation, financial diligence, and intercreditor issues. If the borrower has a multi-entity structure in both countries, timing often stretches because security and tax review need to line up.

Can a mezzanine loan be repaid early?

Sometimes, but don't assume flexibility. Many mezzanine lenders negotiate protections against early repayment because they underwrite a target return, not just short-term interest. The key questions are whether prepayment is permitted, when it is permitted, and what premium or make-whole style economics apply under the agreement.

What happens if my business defaults on a mezzanine loan?

The lender's remedy is usually tied to the pledged equity interests, not direct foreclosure on the operating asset itself. That can mean a fight over ownership control of the borrowing entity. In practical terms, default can trigger loss of control, litigation over governance rights, business disruption, and pressure from both the senior lender and mezzanine lender at the same time.

Do I need a lawyer to negotiate a mezzanine loan?

If the loan is material to your business, yes. Mezzanine debt documents combine debt terms, equity-style upside, and layered enforcement mechanics. Cross-border transactions add another level because one country's template often misses the other country's perfection, tax, or governance issues. Cheap forms are expensive when they fail at closing or default.

If you're weighing mezzanine debt for a U.S.-Canada deal, legal structure usually determines whether the financing remains a useful bridge or turns into a control problem later. A careful review of the capital stack, intercreditor terms, and cross-border enforcement path can prevent expensive surprises before closing. For a practical review of your transaction, contact Mayo Law.

Mezzanine debt can solve a real financing gap when senior debt stops short and an equity raise feels too costly. But the definition of a mezzanine loan only gets you so far. The key work is in the structure, the documents, and the default mechanics. If your business operates across the U.S. and Canada, that detail matters even more because the wrong template can create risk on both sides of the border.

How Mayo Law Can Help

Mezzanine financing gets harder once a deal crosses the U.S.-Canada border. The documents may look familiar, but the enforcement path, security package, entity structure, and tax treatment often do not line up cleanly from one side of the border to the other.

Mayo Law advises founders, CFOs, and deal teams on how mezzanine terms will work in practice before they sign. That includes reviewing the borrower and holdco structure, negotiating lender documents, checking intercreditor provisions against the senior facility, and identifying cross-border issues that can create delay, cost, or control problems later.

If your company is considering mezzanine debt in a U.S.-Canada transaction, Mayo Law can help you assess the structure, allocate risk, and close with clearer expectations about what happens if the deal performs well, or if it does not.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.