You’ve built a solid construction business in Toronto. Then a project in Buffalo lands on your desk that’s too large to bid alone, too attractive to ignore, and too risky to approach with a thin template agreement. That’s where construction joint ventures stop being an abstract business concept and become a practical growth tool.

At Mayo Law’s international business practice, we help businesses in Toronto, the GTA, and across the border handle transactions that span Ontario and New York on a process that often touches both sides of the border. If you’re looking at your first US-Canada project, the core work isn’t just finding a partner. It’s deciding who controls the job, who carries which risk, how profits are split when contributions aren’t equal, and how tax and compliance will work when two legal systems apply.

Published: June 26, 2026

Updated: June 26, 2026

Read time: 11 minutes

Introduction

A cross-border project usually starts with a simple commercial problem. You have enough skill to do the work, but not enough bonding capacity, manpower, local licensing coverage, or owner-facing track record to carry the bid alone. A joint venture can solve that problem, but it can also create a new one if the parties never settle control, money, and exit rights with precision.

That’s why the first question isn’t whether to partner. It’s what kind of partnership you’re creating and whether the legal structure fits the project.

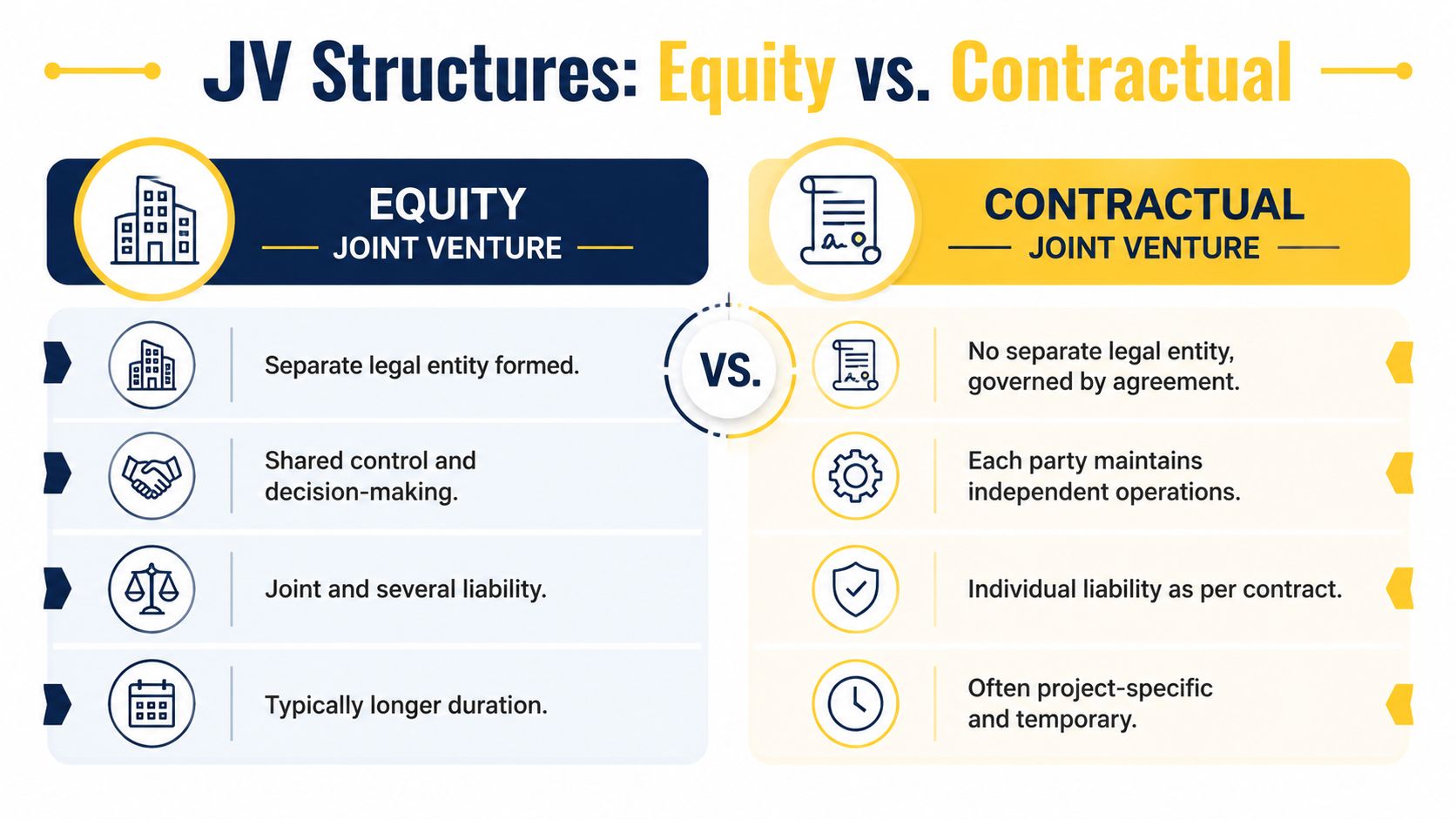

JV Structures Compared Equity vs Contractual

| Feature | Equity JV (e.g., LLC/Corporation) | Contractual JV (Unincorporated) |

|---|---|---|

| Legal status | Separate legal entity | No separate entity |

| Liability profile | Corporate shield can protect participants from direct liability exposure | Liability is driven by the contract and applicable law |

| Governance | Formal governance through entity documents and JV agreement | Governance lives almost entirely in the JV agreement |

| Administrative load | Higher | Lower |

| Best fit | Larger, longer, higher-risk projects | Project-specific arrangements needing speed and flexibility |

| Tax treatment | Depends on jurisdiction and entity form | Often driven by direct allocation to participants |

| Market perception | Can look more institutional to owners and lenders | Often faster to assemble for a defined bid or job |

The choice between an incorporated or contractual JV primarily dictates liability and governance. An incorporated JV, such as an LLC, offers a protective corporate shield that suits higher-risk projects, while a contractual JV depends heavily on the written agreement to define rights, authority, confidentiality, non-compete obligations, and internal remedies, as discussed by Stone Crosby on construction joint ventures.

When an equity JV makes more sense

If the project is long, capital-heavy, design-build, or exposed to meaningful claims risk, an incorporated vehicle is usually easier to govern. The parties can appoint managers, define reserved matters, and create a clean operating framework that separates project activity from day-to-day operations.

That structure also forces discipline. Board approvals, contribution schedules, and entity-level records tend to make disputes easier to diagnose because the paper trail is better.

Practical rule: If the project could materially affect your company's balance sheet, don't treat the structure as an afterthought.

When a contractual JV is the better tool

A contractual JV can work well when the project has a defined scope, the parties want speed, and each participant will largely keep its own operations, people, and systems. It avoids setting up a separate company, but that simplicity is deceptive. The drafting burden moves into the agreement itself.

In practice, contractual JVs fail when owners assume flexibility means informality. It doesn't. It means the contract has to do more work.

Governance decides whether the structure works

A bad equity JV still fails. A good contractual JV can still succeed. The difference is usually governance, not labels. Stone Crosby notes that failure often stems from a mismatch in objectives rather than financing limits, which is why authority thresholds and exit planning matter so much.

For design-build work, documents such as ConsensusDocs 499 give parties a benchmark instead of forcing them to draft everything from zero. That doesn't replace legal judgment, but it does create a starting point.

If ownership economics are part of the discussion, the same discipline used in equity dilution planning applies here. Control, contributions, and future upside need to line up on paper before the project starts.

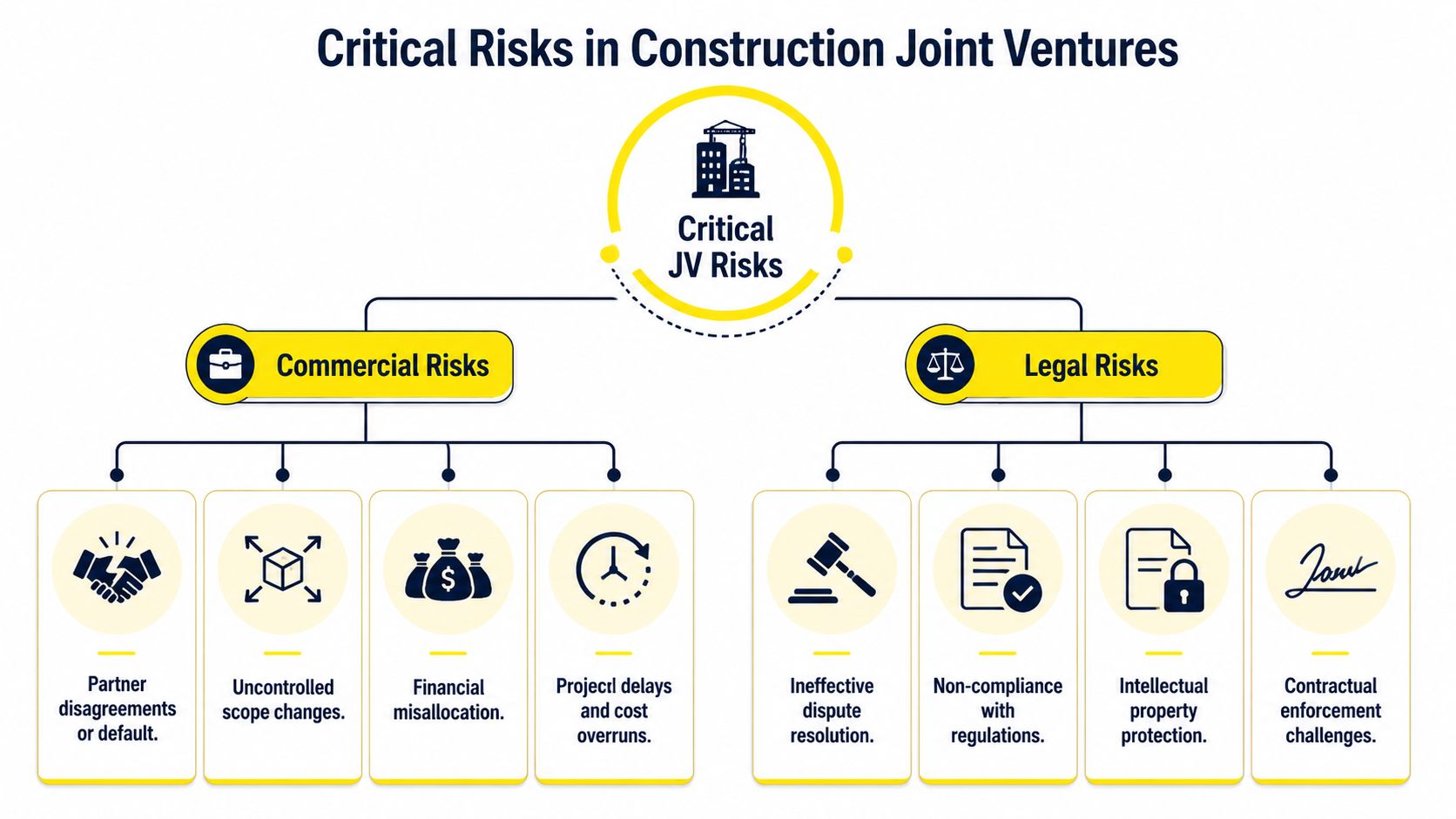

Key Commercial and Legal Issues in JVs

A contractor based in Ontario wins access to a U.S. project only because a local partner can front bonding support, deal with the owner, and carry the licensing risk on the ground. The Canadian party expects a fair share of upside because it is supplying the specialty crews that will make the schedule work. The U.S. party expects tighter control because its balance sheet and local relationships are exposed first. That tension sits at the center of many construction JVs, especially in cross-border deals that are not structured 50/50.

Allocation of risk and liability

Construction SMEs often focus on the profit split first. The harder question is who is carrying project risk.

One partner may provide equipment and field staff. Another may contribute local licensing coverage, owner access, bonding capacity, or parent support undertakings. Those contributions are different in kind, so equal economics often produce unequal pain later. Projul's guide to construction joint ventures notes that asymmetrical participation is common, and that matches what shows up in live deals.

The agreement should say, in plain terms, how each category of risk is allocated:

- cost overruns within a partner-controlled work package

- delay exposure caused by one partner's procurement or staffing failure

- liquidated damages that flow from joint management decisions

- warranty callbacks tied to self-performed work

- third-party claims that arise from design, safety, or site supervision

If those buckets are left vague, the parties end up arguing about fairness after the money is gone.

What is the main risk in a joint venture?

The main risk is not the existence of disagreement. It is a structure that lets disagreement shut the project down.

In non-50/50 deals, the weaker drafting usually appears around authority. Who can sign a change order. Who can settle a subcontractor claim. Who controls the schedule update that becomes the basis for a notice to the owner. Who decides whether to fund a shortfall now and argue about allocation later. Projul's discussion of construction joint venture agreements points to the same problem in a different way: uneven contributions and mismatched expectations drive failure when the parties never converted commercial assumptions into operating rules.

A deadlock clause matters. So do reserved matters, escalation steps, and cash call mechanics.

For U.S.-Canada projects, add one more layer. The party with local licensing, tax registrations, or labor familiarity will often demand more control than its profit percentage suggests. That is not overreaching by definition. It may reflect real exposure. The mistake is leaving that control informal.

Unclear authority turns an overrun into an internal claim before the owner dispute is even resolved.

Performance guarantees and bonding

Bonding support changes the economics of the deal, even when it does not show up neatly in the profit split.

If one party is providing indemnity backing, using its surety relationship, or putting its balance sheet behind performance, the JV agreement should state what that support is worth and how it is repaid or compensated. I often see parties treat bond support as a side assumption. Then a claim hits, the surety starts asking questions, and the partner that carried the paper realizes it accepted enterprise-level exposure for project-level return.

That issue gets sharper in cross-border work. A Canadian contractor joining a U.S. public project may be commercially indispensable on execution but still rely heavily on the U.S. partner for bonding, local prequalification, and owner-facing compliance. If the U.S. partner bears those obligations, the internal allocation should reflect it.

Insurance and project controls

Insurance should be negotiated with the same care as the commercial split. It is not back-office language.

The parties need clear answers on:

- who is a named insured and who is an additional insured

- which policy responds first for site injury, property damage, and professional exposure

- how deductibles and self-insured retentions are shared

- whether the JV carries project-specific coverage or relies on each partner's program

- who has authority to report, defend, and settle claims

Cross-border teams miss this point regularly. A Toronto contractor may assume its existing coverage extends cleanly into New York or Michigan. Sometimes it does. Sometimes exclusions, admitted carrier rules, wrap-up requirements, or professional liability gaps create a problem that only appears after a claim is made.

The same discipline applies to internal risk allocation. If the parties want to cap certain categories of exposure between themselves, they should build that into the contract early using well-drafted liability limitation provisions, not try to improvise after a default notice or coverage dispute.

Two practical scenarios

A Canadian concrete contractor joins a U.S. civil firm on a public infrastructure package. The Canadian side supplies specialty crews, equipment, and production know-how. The U.S. side handles permits, owner communications, local labor issues, and bonding support. An equal profit split may sound cooperative, but it will not hold if one side is carrying most management decisions and balance-sheet exposure. The better approach is to match economics to actual burden, then write detailed adjustment rules for owner-caused changes, partner-caused overruns, and unreimbursed general conditions.

A second scenario is more common than parties admit. One partner controls the project controls system, cost coding, and monthly reporting because it has the stronger back-office platform. The other partner accepts that arrangement without testing definitions for overhead, home-office charges, equipment rates, and contingency drawdowns. The dispute appears late, during final reconciliation, when neither side agrees on what the numbers were measuring in the first place.

Weak definitions cause expensive fights. In a cross-border JV, they also create tax and reporting problems if the books used for internal allocations do not line up with how the parties must report revenue, expenses, or permanent establishment risk in the United States and Canada.

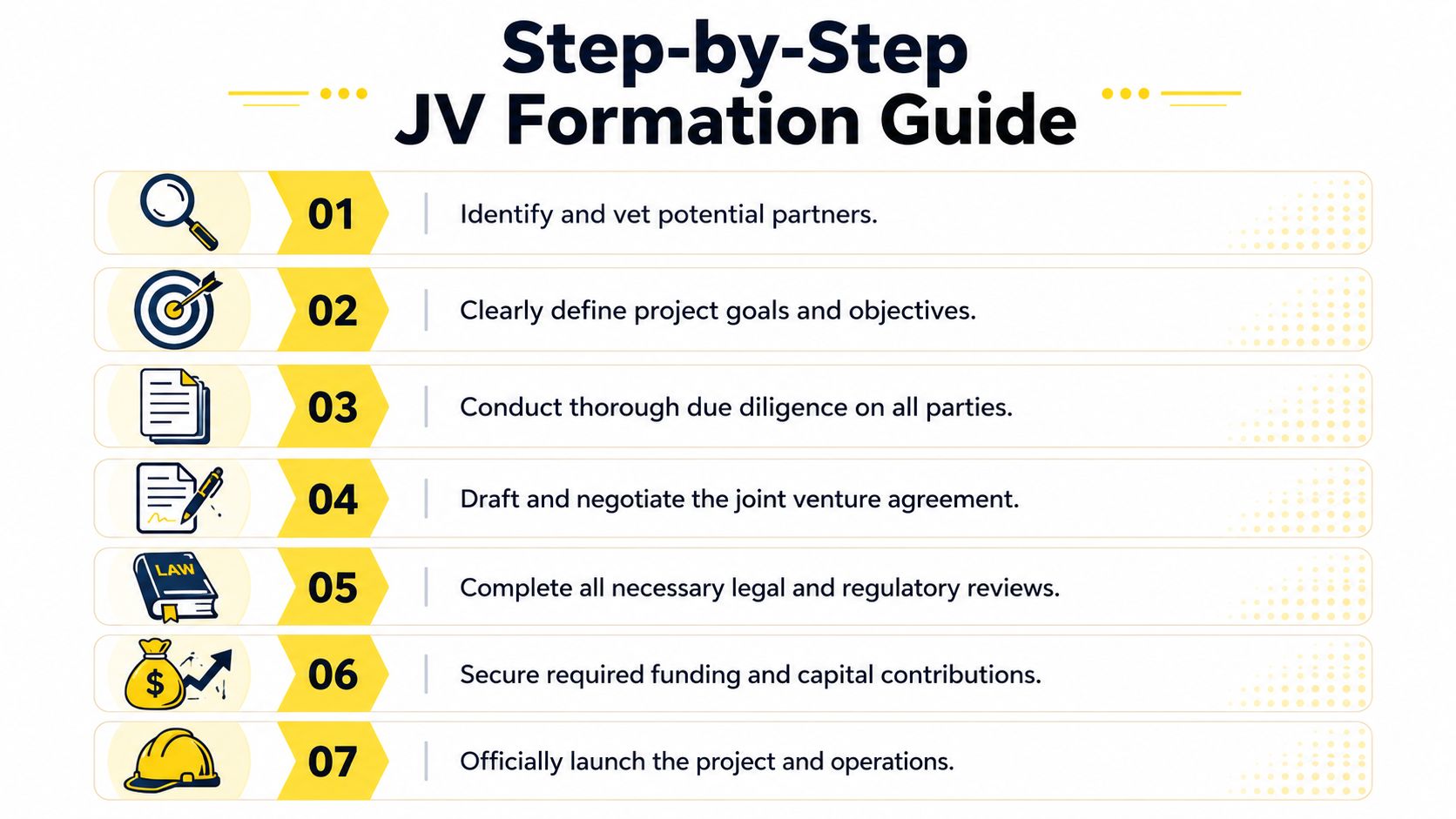

How to Form a Construction Joint Venture Step by Step

A common first mistake happens before the bid is submitted. Two contractors agree on the opportunity, divide the work in broad terms, and leave the legal structure for later. By the time the owner asks for clarifications on bonding, authority, or who carries a delay claim, the parties are already negotiating under pressure.

Start earlier than that. A construction JV should be built in the same order as the project itself: partner review, scope allocation, governance, entity choice, then contract drafting that matches how the job will run.

Step 1. Vet the partner beyond the pitch

Review the items that create trouble after award, not just the qualifications package. Check litigation history, claim history, safety performance, licensing status, financial strength, and bonding history. Confirm who will lead the project on the ground. The legal entity signing the JV agreement is only part of the risk. The proposed project manager, controller, and superintendent often matter more.

For a U.S.-Canada deal, verify cross-border capability at this stage. Can the Canadian party work in the relevant U.S. state without licensing problems? Can the U.S. party perform in Canada without creating registration, payroll, or tax issues it has not priced? If the answer is unclear, the bid model is incomplete.

Ask for sample monthly reports before you sign anything. If the parties cannot agree on cost codes, backup, and change-order tracking at the start, they usually will not agree on final account treatment later.

Step 2. Define project scope and contributions

Set out each contribution with enough detail that a project accountant and a project manager would read it the same way. That includes:

- Capital, including timing and consequences for late contributions

- Bonding support, indemnity exposure, collateral, and reimbursement rules

- Personnel, including named key roles and replacement rights

- Equipment, rates, maintenance responsibility, and idle-time treatment

- Work packages, with clear responsibility lines

- Local access, including permits, supplier relationships, union knowledge, and labor channels

The viability of many non-50/50 JVs, or their tendency to generate disputes, often hinges on the specific structure. If one party brings the owner relationship, local licensing, and most of the bonding capacity, while the other brings specialty means and methods or production crews, equal economics may not make sense. The profit split, management fee, and loss allocation should match actual burden and actual exposure.

As noted earlier, industry practice treats JVs as a practical way to combine bonding capacity, local presence, and technical capability on larger jobs. That makes the contribution schedule more than a business summary. It becomes the foundation for profit allocation, decision rights, and default remedies.

Step 3. Set governance before the bid goes in

Authority should be tied to real project decisions. State which matters require unanimous consent, which require a board or management committee vote, and which the managing venturer can decide alone.

Be specific. Bid revisions, subcontract awards, payment applications, claims notices, settlements, design changes, schedule recovery measures, and contingency draws should each have their own approval threshold. A single sentence saying the managing partner handles "day-to-day operations" is too vague for a live construction dispute.

One warning sign comes up often. If the parties keep postponing authority questions because they "trust each other," they are relying on goodwill where they need procedure.

What are the key clauses in a joint venture agreement?

The clauses that matter in practice are scope, contributions, profit and loss allocation, management authority, cost coding, reporting, subcontracting authority, confidentiality, dispute resolution, default remedies, and exit rights. Strong agreements also deal with deadlock, parent guarantees, intellectual property, insurance coordination, and what happens if one party must cure the other party's default to protect the owner contract.

Step 4. Decide whether to incorporate

Choose the structure based on the job, not on habit. A purely contractual JV can work well for a single project with clearly divided scopes and limited outside financing. A separate corporation often makes sense where the owner expects a single contracting vehicle, the project will run for years, financing is more complex, or the parties want cleaner separation of project assets and liabilities.

For an Ontario participant considering a project company, the mechanics overlap with Ontario business incorporation steps. Cross-border projects add another layer. The Canadian and U.S. formation choices need to line up with tax reporting, licensing, authority to contract, payroll setup, and the owner's procurement requirements.

Do not assume incorporation solves allocation problems. It changes the wrapper. The hard work is still in the shareholder terms, management rights, funding obligations, and exit mechanics.

Step 5. Draft for the job you will actually run

The agreement should read like the project operating manual. If procurement is centralized, say who signs purchase orders and who approves vendor selection. If one partner controls scheduling and the other controls estimating or self-perform work, define the handoff points, reporting rights, and consequences of late or inaccurate inputs.

Spell out the mechanics for change orders, backcharges, home-office overhead, equipment rates, and contingency use. In cross-border JVs, I also want the documents to identify who handles tax registrations, payroll withholding, customs or temporary import issues for equipment, and the books of account that will govern internal allocations.

A good JV agreement answers the Tuesday afternoon question. The owner wants a response by 5 p.m., costs are moving, and the partners disagree. The document should tell the team who decides, who pays first, and how the adjustment is reconciled later.

Navigating US-Canada Regulatory and Tax Traps

The first real problem in a US-Canada construction JV often shows up before the first invoice. A U.S. contractor prices the job assuming the Canadian side will deal with GST/HST, payroll, and local registrations. The Canadian partner assumes the U.S. side has cleared immigration, customs, and internal tax treatment for cross-border staff and equipment. Both assumptions can be wrong, and the gap usually surfaces after the bid is in and the margin is already committed.

How are joint ventures taxed in Canada?

For Canadian tax purposes, a construction JV is often treated as a flow-through arrangement rather than a taxpayer at the venture level. The co-venturers generally report their own share of income and expenses through their existing entities, as described in Dexado's overview of Canadian construction joint venture taxation. That structure can work well for a cross-border project, but only if the JV agreement and the books allocate revenue, costs, holdbacks, equipment charges, and overhead the same way the tax reporting does.

Canada also has a point many U.S. contractors miss. The Joint Venture (GST/HST) Regulations identify construction of real property as a prescribed JV activity, including related development and tendering work, under Justice Canada's regulations page. That matters because GST/HST administration in a JV can be handled differently from a simple subcontracting arrangement, and the election mechanics should be reviewed early with tax advisers on both sides of the border.

The U.S. side adds another layer. A Canadian flow-through treatment does not guarantee the same result for U.S. federal or state purposes. If one venturer is using a U.S. corporation and the other is using a Canadian corporation or limited partnership, the same project cash can be characterized differently in each country. That is where double reporting risk starts.

The Canadian legal form issue

A Canadian JV is usually a contract, not a separate statutory person. Jahan Law's discussion of joint venture agreements explains that distinction well. In practice, that means liability, signing authority, profit allocation, and management control come from the documents and the parties' conduct, not from a default corporate wrapper.

For non-50/50 deals, this point matters even more. One partner may put up bonding capacity, parent support, or local licensing infrastructure, while the other brings specialized crews, equipment, or owner relationships. The profit split may be 60/40 or 70/30, but the risk split is often not symmetrical. If the agreement does not say who carries tax filings, audit defense, reassessments, denied input credits, or permanent establishment exposure, those disputes tend to get argued after the cost is already incurred.

Anti-bribery, compliance, and workforce mobility

Cross-border public and infrastructure work can trigger anti-bribery review, customs controls, labor mobility questions, and document formalities before mobilization. The JV should use one compliance protocol for gifts, third-party intermediaries, expense approvals, and record retention. If one venturer follows stricter internal controls than the other, adopt the stricter standard across the project.

Immigration is rarely just an HR issue. Superintendents, commissioning staff, and field engineers may be cleared to enter a country for meetings but not to perform hands-on project work. The current rules should be checked through USCIS and the Government of Canada immigration portal. Equipment movement can create a second problem if tools, vehicles, or temporary imports cross the border without the right customs planning.

Practical traps that deserve attention in the term sheet

- Tax reporting mismatch: Canada treats the arrangement one way, while U.S. tax advisers book the same economics differently.

- Permanent establishment risk: A U.S. participant may create Canadian tax filing exposure through site activity, employees, or management presence.

- GST/HST administration errors: The parties assume one venturer will handle filings or elections, but the documents do not assign the job clearly.

- Withholding and payroll mistakes: Employees work in the other country before payroll registrations and source deductions are set up.

- Authority mismatch: The owner relies on the lead venturer, but the JV agreement limits who can bind the participants.

- Customs and immigration delay: Key personnel or equipment cannot get on site when needed.

- Asymmetrical downside: The minority venturer has limited control but still carries uncapped indemnity or tax exposure.

If the deal economics depend on U.S. entity choice, cross-border income characterization, or where profits are recognized, review those issues against the Section 250 deduction rules for international business income before the JV structure is locked in.

How Do You Prevent and Resolve JV Disputes

The best dispute clause is drafted when everyone still likes each other. After default notices start flying, the parties won't negotiate cleanly.

Build a dispute ladder

For cross-border construction work, a multi-step process usually works better than a single jump to litigation. A practical sequence is:

- Project-level negotiation within a short fixed window

- Executive escalation to named senior decision-makers

- Mediation with a neutral who understands project delivery

- Arbitration or court if the dispute still blocks performance

Mediation is often the right first formal step because the parties usually need to keep building while the issue is being sorted out. Arbitration can be useful for technical confidentiality and enforceability, but it's still expensive and still adversarial.

Put time limits in the clause. Without deadlines, escalation clauses become delay tools.

Draft for the common triggers

Most JV disputes come from a short list of triggers:

- Cost overruns tied to disputed responsibility

- Quality disputes on divided scopes

- Schedule slippage and who caused it

- Change order strategy with the owner

- Cash flow strain after delayed payment

- Default by one partner

Deadlock clauses matter here. So do step-in rights, buy-sell rights, cure periods, and interim authority rules so the project can keep moving while the argument is pushed upward.

Choose the forum carefully

A Toronto contractor on a New York job may prefer New York law and seat. A Canadian-heavy contractual JV for work north of the border may not. There is no universal answer. The point is to choose consciously.

If arbitration is the preferred route, parties should think through governing law, seat, interim relief, confidentiality, and enforcement from the outset. For a broader overview of process design, arbitration in Canada and enforcement issues is a useful starting point.

Frequently Asked Questions

What is the difference between a joint venture and a partnership in Canada?

In Canada, a joint venture is not legally recognized as a separate entity like a partnership. That means the parties rely primarily on contract to define contributions, management, and liability allocation. A partnership usually carries a more established legal framework and agency concepts between partners. With a JV, you should assume the agreement must answer the operational questions in detail.

How much does it cost to set up a construction joint venture?

The legal cost depends on the structure, project size, jurisdiction count, tax planning needs, and whether financing, bonding, or immigration issues sit in the background. There isn't a responsible flat estimate for every deal. If a separate entity is being formed, filing costs and procedures should be confirmed through official sources such as Ontario business registration information or the relevant U.S. state filing office.

How long does it take to form a construction JV?

The timeline depends on how aligned the parties already are. A straightforward contractual JV can move faster than an incorporated structure, but even then, due diligence, insurance review, tax planning, and authority mapping take time. Cross-border deals usually slow down when owners leave immigration, tax, or signing formalities until the final week.

Can a foreign company join a Canadian or U.S. construction JV?

Yes, but that doesn't mean it can start work. Foreign participation raises entity qualification, tax registration, local licensing, employment, and immigration questions. The practical issue is rarely whether the foreign company can sign. It's whether it can perform, invoice, staff, insure, and comply lawfully in the jurisdiction where the project sits.

What happens if my JV partner becomes insolvent?

That risk should be addressed before contract award. A good agreement will define default, notice, cure rights, step-in rights, project continuity measures, and how the solvent party can protect the owner relationship and complete the work. If insolvency isn't addressed directly, the surviving partner may be forced to improvise under pressure while also dealing with owner demands and unpaid subcontractors.

If you're weighing a construction JV for a US-Canada project, a careful structure at the start is usually cheaper than cleaning up a failed alliance mid-project. Mayo Law advises on cross-border business arrangements, contracts, compliance, and related disputes for companies operating between Ontario and New York.

A first international JV doesn't need to be overly complicated, but it does need to be deliberate. The structure, the paper, and the operating rules should match the project you're pursuing. If they don't, the problems usually appear at the worst possible moment: after award, during execution, and under deadline.

How Mayo Law Can Help

A US contractor and a Canadian contractor can agree on the bid split in an afternoon and still spend months fighting over who controls change orders, who carries payroll tax risk, or who is left exposed if the project loses money. That is usually a structuring problem, not a relationship problem.

Mayo Law helps construction companies set up cross-border joint ventures so the legal documents match the actual agreement the parties have made. That includes choosing between an equity JV and a contractual JV, documenting uneven profit and loss allocations, assigning signing authority, aligning insurance and indemnity terms, and dealing with the tax and regulatory friction that appears when work, people, and invoicing cross the US-Canada border.

For a first international JV, the practical question is rarely whether the parties can work together. It is whether the structure will hold once the owner issues directions, the schedule tightens, and one partner is carrying more execution risk than its ownership percentage suggests. That is the point where careful drafting pays for itself.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

If you are structuring a cross-border construction JV, the adjacent issues usually do not sit in one lane. Tax, licensing, site access, labor mobility, and compliance tend to move together, especially where one partner contributes capacity and the other carries more project risk for a larger share of the upside.

These related resources cover the supporting pieces: