Published: June 3, 2026

Updated: June 3, 2026

Read time: 11 minutes

A CFO is closing a financing on a tight timeline, the board wants a clean budget, and someone asks a basic question late in the process: what is the SEC registration fee for this filing, and when does it have to be paid? In our practice, that question often comes up only after the filing strategy is already in motion. By then, the fee issue is no longer administrative. It affects timing, disclosure, and who needs to fix the filing if the numbers or payment mechanics are wrong.

That matters even more in cross-border deals. We see Canadian issuers and other foreign companies assume the fee is a small U.S. filing charge that can be handled at the end. In reality, the amount depends on the filing type, the aggregate value being registered, the SEC's current rate, and whether an exemption or transaction structure changes the result. For a founder or finance lead, the practical question is not only "what is the rate?" It is "what should we budget, what triggers the fee, and where can we reduce avoidable cost without creating a compliance problem?"

This guide answers that from a working lawyer's perspective. It is written for CFOs, founders, and legal teams who need a usable framework, especially if a Canadian company is accessing U.S. markets or combining a domestic financing with cross-border expansion planning. If you are still putting the broader legal setup together, our startup business attorney services are often where that planning starts.

The goal is straightforward. Get the fee calculation right, understand the current payment workflow, and spot planning opportunities early enough to use available exemptions and timing strategies.

What Is the SEC Registration Fee?

The SEC registration fee is a charge tied to certain securities registrations and related transactions. It is generally calculated from the aggregate offering amount using the SEC's current fee rate, rather than as a flat filing charge. That's why the answer depends on what you're filing, when you're filing, and how much securities value is being registered.

A lot of confusion comes from outdated explainers. The SEC recalculates the rate annually, and recent rule changes also changed how fee information is filed and paid. As noted in this discussion of SEC fee-rule modernization and EDGAR/Pay.gov workflow changes, checks and money orders are no longer accepted, and structured fee exhibits are now part of the operational reality.

If your team is still treating this as a static admin line item, that's usually where mistakes start. The legal issue is not only the math. It's also whether the filing type triggers a fee, whether the fee table is prepared correctly, and whether payment is made through the current SEC workflow.

For founders who are still sorting out basic entity documents before a financing, it also helps to understand how corporate formation documents fit into the larger offering process. A useful starting point is this overview of what a certificate of incorporation is.

Does every SEC filing have a registration fee?

No. A common misconception is that every SEC filing triggers a fee. The SEC generally ties fees to securities registrations, tender offers, mergers, and certain repurchases, while routine reports such as Forms 10-Q and 8-K typically do not require a registration fee, as explained in this overview of SEC filing fee categories.

Practical rule: Start with the transaction, not the form name alone. Teams often ask, “Is there a fee for this filing?” The better question is, “What transaction is this filing trying to accomplish?”

How to Calculate the SEC Registration Fee in 2026

For fiscal year 2026, the SEC set the fee rate for Section 6(b) registrations at $138.10 per $1,000,000, or 0.00013810, according to the SEC's fiscal 2026 fee-rate advisory. The mechanics are simple: multiply the aggregate offering amount by the current rate.

That means the core formula is:

- Aggregate offering amount × 0.00013810

- Or, stated another way, $138.10 for each $1,000,000 registered

Here are practical examples using the fiscal 2026 rate.

| Total Offering Amount | Calculation | Estimated SEC Fee |

|---|---|---|

| $10 million | $10,000,000 × 0.00013810 | $1,381 |

| $50 million | $50,000,000 × 0.00013810 | $6,905 |

| $100 million | $100,000,000 × 0.00013810 | $13,810 |

The math itself is not the hard part. What matters is making sure you are using the correct rate for the filing date and the correct amount being registered.

Why timing matters

This fee moves. It is not fixed. In an earlier annual adjustment, the SEC registration fee rate moved from $110.20 per million dollars to $147.60 per million dollars effective October 1, 2023, a change described as nearly 34%. On a $100 million registration, that changed the fee from about $11,020 to about $14,760, as summarized in this analysis of the 2023 SEC fee increase.

That example is useful because it shows why stale templates and old budgeting assumptions cause avoidable errors. If your board approved a transaction budget using a prior fiscal year rate, your final numbers may need adjustment before filing.

How often does the SEC registration fee change?

The SEC recalculates the registration fee rate annually. In practice, finance and legal teams need to pay close attention to the effective date of the new fiscal year rate, because a filing prepared under one assumption can become inaccurate if it is submitted after the updated rate takes effect.

In our practice, this comes up often in cross-border deals that slip by a few days while comments are cleared or board approvals are finalized. The fee issue looks minor until the filing date moves across the annual reset.

Where companies get tripped up

A few recurring errors show up repeatedly:

- Using last year's rate: Someone copies a prior fee table without checking the effective date.

- Using the wrong offering amount: The number in the budget deck isn't always the number that belongs in the registration statement.

- Treating it like a legal flat fee: It isn't. The fee scales with the transaction.

- Forgetting offsets or structure issues: The basic formula is straightforward, but the actual filing may involve nuances that need review.

If the deal documents are still being negotiated, coordination matters. That is particularly true when the fee assumptions connect to share issuance mechanics in your transaction documents, including stock purchase agreements.

The formula is mechanical. The judgment call is everything around the formula.

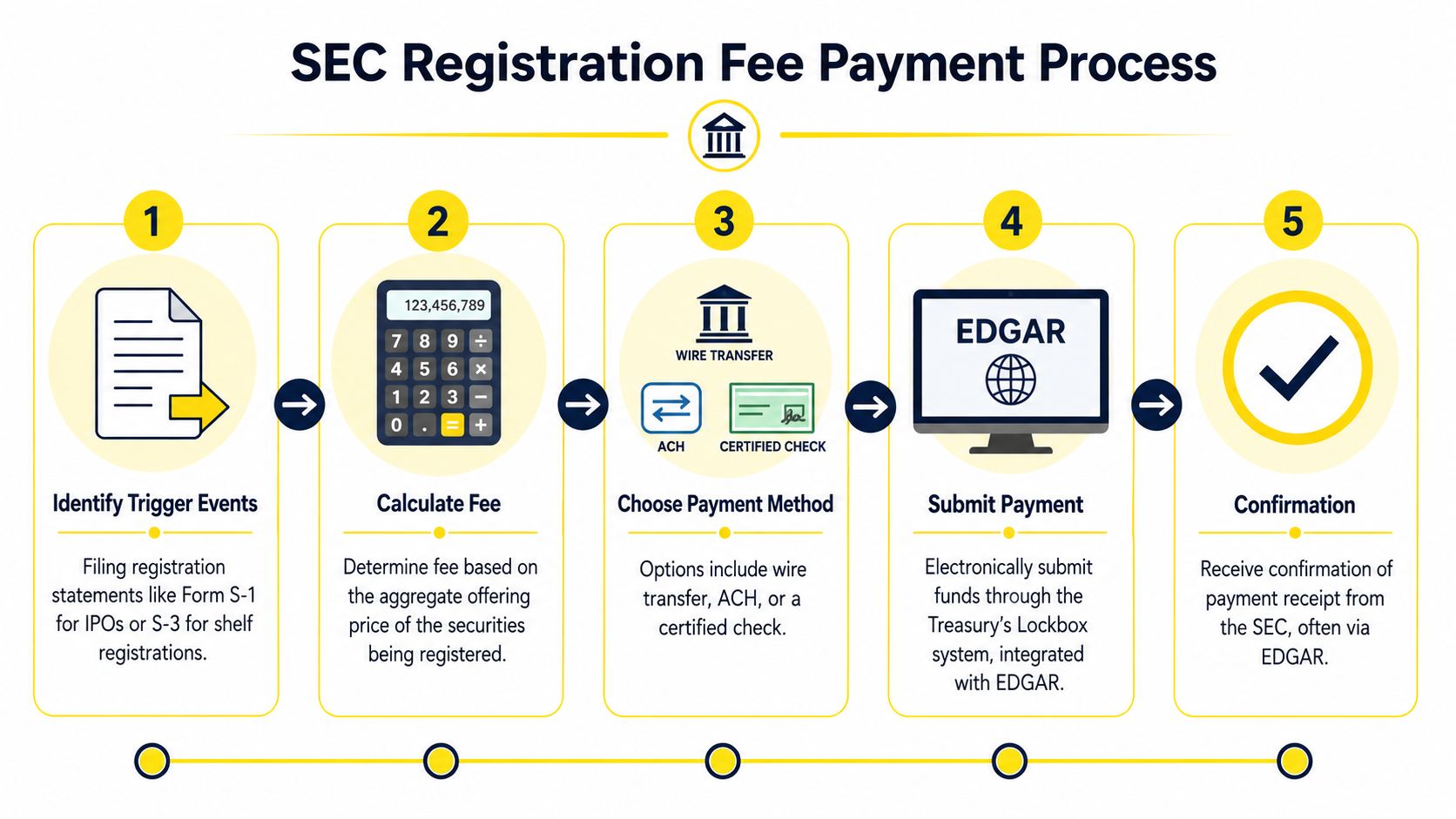

When and How to Pay the Registration Fee

A common problem looks like this. The registration statement is ready, management has signed off, the filing agent is standing by, and someone asks whether the SEC fee has been funded and submitted. If that answer is unclear, the filing is not ready.

For CFOs and founders, the fee is part of closing mechanics, not a clerical afterthought. In our practice, this issue shows up most often in public offerings, resale registration statements, business combination filings, tender offers, and some issuer repurchase filings. Cross-border teams are especially prone to timing gaps because treasury, U.S. counsel, Canadian counsel, and the filing agent may all assume someone else owns the last step.

Transactions that commonly trigger the fee

The practical question is whether the filing creates a fee obligation under the SEC rules applicable to that transaction. Common examples include:

- Registered offerings: IPOs, follow-on offerings, and many resale registration statements

- Mergers and acquisitions: Certain registration and transaction filings require fee analysis

- Tender offers and some proxy-related filings: Fee treatment can differ by structure

- Certain repurchases: Some Exchange Act filings carry filing-fee consequences

The legal analysis should happen early, before the filing date is set internally. A filing calendar built on the assumption that payment can be sorted out at the end creates avoidable risk.

How payment works now

The SEC's current process runs through EDGAR and Pay.gov. Companies generally pay by ACH, debit card, or credit card. Old internal checklists are often the problem here. We still see finance teams working from procedures built around methods the SEC no longer accepts.

A workable internal process usually has five parts:

- Identify the filing that triggers the fee

- Confirm the amount that belongs in the fee table

- Prepare the filing so the fee disclosure matches the transaction terms

- Coordinate the payment method and account access in EDGAR/Pay.gov

- Confirm acceptance, not just submission

Ownership matters. Legal may calculate the fee, but finance usually controls cash movement and payment credentials. Someone inside the company should be accountable for both sides lining up. For many issuers, that responsibility sits with the legal or finance lead handling compliance officer responsibilities for SEC-facing processes.

Timing issues that delay filings

The fee is usually handled at the time of filing for the relevant transaction. Companies should budget for it and treat it as part of filing readiness.

The mistakes are predictable. Treasury approval is pending. The Pay.gov access is with one employee who is traveling. Outside counsel has the final fee table, but finance funded a different amount based on an earlier draft. For foreign private issuers and Canadian companies entering the U.S. market, these gaps are more common because the people approving the filing may sit in one country while the payment mechanics are handled in another.

The fix is simple, but it requires discipline. Assign one internal owner, confirm the fee amount against the final filing version, test payment access before filing day, and build enough time for cross-border approvals. That is how companies avoid a preventable delay that has nothing to do with disclosure quality.

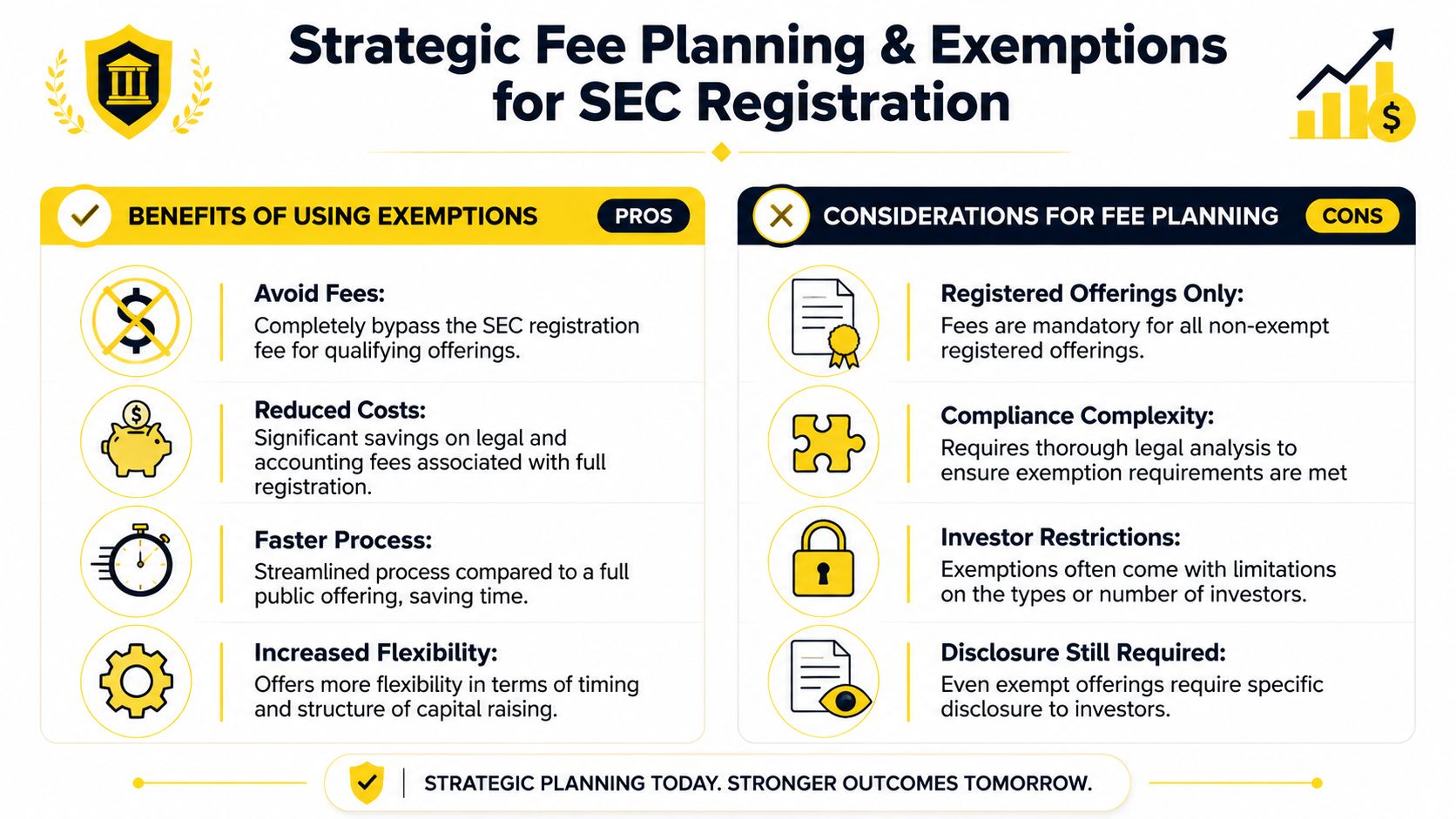

Common Exemptions and Strategic Fee Planning

A CFO approves a U.S. financing budget based on the headline filing costs, then learns late in the process that the company could have structured part of the deal on an exempt basis and reduced the immediate SEC fee burden. We see that problem often in cross-border transactions, especially where Canadian management, U.S. counsel, and finance are making decisions on different timelines.

The practical point is simple. The SEC registration fee applies to registered offerings and certain transaction filings. It does not apply to every capital raise, and that creates real room for planning if the structure is analyzed early enough.

Registered versus exempt capital raising

An exempt private placement may avoid Securities Act registration for the offering itself. In that case, the SEC registration fee may not be part of the initial raise at all. A registered offering is different. Once the company chooses that route, the fee becomes part of the filing design, the budget, and often the timetable.

That choice should be made at the structuring stage, not after the first draft registration statement is already circulating. By that point, the legal and commercial assumptions are usually harder to change without cost, delay, or both.

What works in practice

In our practice, the best planning usually comes from asking a narrower set of questions before launch:

- Is this financing actually required to be registered, or is an exemption available for the initial sale?

- If the company starts with an exempt round, will a later resale registration create a separate fee event?

- Is the company filing a shelf that front-loads fee planning, or using a transaction-specific filing tied to one deal?

- Does the expected filing date change the fee budget enough to matter for board approval or cash planning?

Those questions matter because related filings often produce different fee results. A private financing, a resale registration, a shelf registration, and a later takedown can each need separate analysis. Teams get into trouble when they assume one answer carries across the full life of the transaction.

Where planning goes wrong

The recurring mistakes are predictable. Some issuers assume every SEC-facing filing carries a registration fee. Others assume that once one fee has been paid, future related filings are covered automatically. Neither approach is reliable.

The better approach is to map the capital plan against the actual filing sequence. For a founder, that affects dilution planning and deal timing. For a CFO, it affects cash forecasting, board materials, and whether the U.S. leg of the transaction is being budgeted with enough precision.

Cross-border issuers need even more discipline here. A Canadian company may be balancing home-country financing rules, U.S. resale expectations, and investor requests for liquidity on different schedules. Those factors can push the company toward a registered path earlier than management originally expected.

Good fee planning starts before the filing set is drafted. Once the filing path is fixed, the cost options are narrower.

Cross-border strategic choices

For Canadian and other foreign issuers, fee planning is rarely just a math exercise. Investor location, the likelihood of a follow-on U.S. raise, resale expectations, and home-country disclosure timing all shape whether an exempt or registered route makes better sense.

We see this in practice with companies that begin with a private round to control cost and timing, then later register resales or access the U.S. public market through a broader filing strategy. That can be sensible. It also means the fee analysis should be done as part of the financing plan, not treated as a last-minute EDGAR item.

Nuances for Canadian and Foreign Issuers

A Canadian company can approve a financing in Canadian dollars on Monday, circulate a U.S. registration draft on Wednesday, and discover on Friday that the fee assumptions, form choice, and filing mechanics were never aligned. We see this regularly in cross-border deals. The SEC fee itself is straightforward. The cross-border execution often is not.

The filing route matters

Canadian and other foreign issuers need to choose the U.S. filing route early because the form selection affects timing, internal workstreams, and fee planning. Eligible Canadian issuers may use the Multijurisdictional Disclosure System, often through Form F-10. Other foreign private issuers may file on Form F-1 or another form that fits the transaction and issuer status.

That choice does not change the basic rule that registered securities filings can trigger an SEC fee. It does change how quickly the team can prepare the filing, what disclosure needs to be reconciled across jurisdictions, and whether the company is forcing U.S. registration into a timetable built around home-country requirements.

In our practice, problems usually start when U.S. counsel, Canadian counsel, finance, and the filing agent work one after another instead of from the same transaction calendar. A fee issue that looks minor in draft form can delay a launch if the wrong offering amount, form, or exhibit data is carried through the filing set.

Currency and board-level budgeting

Foreign issuers also need a disciplined process for currency conversion. The SEC fee is paid in U.S. dollars. Many board approvals, investor discussions, and internal forecasts for Canadian companies are still prepared in Canadian dollars. If no one is responsible for the conversion methodology and cutoff date, the filing math and the budget can drift apart.

That matters most when timing slips. A delayed filing can change the exchange-rate assumptions used in the company's internal model and alter the actual fee expected at submission. For a CFO, this is not just a legal detail. It affects offering proceeds, transaction costs, and how accurately management briefs the board.

Structured fee exhibits are now an execution issue

Foreign issuers also need to treat the SEC's structured fee exhibit requirements and iXBRL tagging process as part of deal execution, not as a clerical step at the end. The fee table has to match the filing data, the form mechanics, and the payment process. If the inputs are inconsistent, the team can end up correcting avoidable errors under deadline pressure.

This is especially common for startups and growth-stage companies entering both markets at once. If your structure is still being set up on both sides of the border, our guide to starting a business in both Canada and the U.S. gives the broader legal framework. For SEC fee planning, the practical point is narrower. Build the U.S. filing timeline, form choice, currency method, and fee exhibit process into the financing plan before the registration statement is near filing.

Frequently Asked Questions

What happens if I overpay or underpay the SEC fee?

An overpayment and an underpayment create different problems. Overpayment may require a refund or credit process, while underpayment can create a deficiency that delays the filing or requires corrective action. In practice, issuers should not assume these issues are purely administrative. If the filing is time-sensitive, even a small fee mismatch can become a closing problem.

Is the SEC registration fee tax-deductible?

Tax treatment depends on the transaction context and applicable accounting and tax advice. For many issuers, this fee is treated more like a transaction or capital-raising cost than an ordinary operating expense, but the right answer depends on the deal and jurisdiction. Your securities lawyer and tax advisor should align on treatment before the transaction closes.

Can the fee be offset by previous payments?

Sometimes prior payments, withdrawn filings, or transaction restructuring raise offset questions. The answer is highly filing-specific. This is one of those areas where a simple formula is not enough. Before assuming a previous payment can be credited forward, have counsel review the exact filing history, transaction continuity, and current SEC fee table requirements.

What is the penalty for late payment?

The immediate consequence is usually practical rather than punitive in the abstract. If the fee is required for the filing, late or incorrect payment can interfere with acceptance, delay timing, and trigger extra SEC-facing cleanup. For an issuer trying to launch a deal on a specific window, that operational disruption is often the primary cost.

Do foreign private issuers follow different fee rules?

Foreign private issuers often use different registration forms, but they are not outside the filing-fee framework. The important questions are still the same: what transaction is being filed, what amount is being registered, what rate applies on the filing date, and how will the issuer support the structured fee information in EDGAR.

If you're planning a U.S. securities filing, merger, or cross-border capital raise, the legal answer usually isn't just the current rate. It's whether the fee applies at all, how the filing should be structured, and who is managing the payment and disclosure workflow under deadline. Mayo Law advises founders, SMEs, and cross-border businesses on U.S.-Canada business, compliance, and transaction issues.

How Mayo Law Can Help

Cross-border financings often create two separate problems at once: securities compliance and coordination across jurisdictions. Mayo Law helps businesses assess whether a U.S. filing triggers a registration fee, how to structure the process, and how to avoid preventable execution mistakes when U.S. and Canadian teams are both involved. To discuss your matter, visit cross-border international business counsel.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

- Cross-border international business services

- Regulatory compliance services

- Business immigration services