Published: June 18, 2026

Updated: June 18, 2026

Read time: 12 minutes

A Canadian founder gets a U.S. lead investor's term sheet on Friday afternoon. The price looks acceptable. The investor calls it “standard NVCA.” By Monday, the key questions start. Does the company stay Canadian or reincorporate in Delaware? Will the option plan still work for Canadian employees? Do the preferred share rights fit under the company's existing articles? How much board control is being given up?

That is the point where founders often learn that “standard” does not mean simple.

An NVCA term sheet gives U.S. investors and counsel a familiar starting form. For a Canadian company, though, the document often needs legal and tax adjustment before anyone should treat it as plug and play. Terms that look routine in a Delaware financing can affect shareholder approvals, security design, withholding, exchange controls, and closing steps differently north of the border.

The practical job is to separate three categories early. First, the economic deal. Second, control rights. Third, the cross-border changes needed to make those terms work in a Canadian company without creating avoidable tax or governance problems. Founders who do that early usually spend less on document turns and make fewer concessions by accident.

Start with the company's basics. If the articles, share classes, or prior shareholder approvals are not in order, the financing documents become harder and more expensive to paper. For background on the core formation document, see this guide to a certificate of incorporation.

For Canadian founders receiving a U.S. NVCA term sheet, the first checklist is usually straightforward: corporate structure, share terms, option plan treatment, board composition, tax treatment for U.S. and Canadian holders, securities law exemptions, and whether a Delaware flip is warranted. Those are the pressure points that shape influence on both sides long before the long-form documents arrive.

What Is an NVCA Term Sheet?

An NVCA term sheet is a standardized, usually non-binding venture financing template that sets out the core business terms of a proposed investment before the parties spend time and money drafting definitive documents. It gives founders and investors a common starting point on economics, governance, and investor protections.

That standardization matters. The NVCA's Enhanced Model Term Sheet v2.0 was released as a free download on the NVCA model documents page, and NVCA said the documents were revised to reflect evolving market norms and recent legal changes. Paul Hastings described that update as the third version of the NVCA term sheet form, which underscores that the document has been revised over time rather than frozen in place (NVCA release).

In practice, founders should treat the term sheet as the blueprint for the rest of the financing. If you agree to a point here, it often carries forward into the stock purchase agreement, investor rights agreement, voting agreement, and charter amendments.

Practical rule: If a term feels vague in the term sheet, it usually becomes expensive in the long-form documents.

It's also worth separating the company-law basics from the financing terms. If you're still sorting out foundational corporate records, start with the company's formation documents, including the certificate of incorporation. A financing term sheet assumes that base structure is already in order.

Dissecting the Core Economic Terms

The economic terms decide who gets what, when, and in what order. Founders often focus on valuation first because it's the easiest number to compare. That's understandable, but incomplete. A strong headline valuation can be offset by investor-favourable preference rights, anti-dilution protection, or pricing mechanics that change the actual outcome.

Valuation and price per share

There are two basic valuation questions. Is the quoted number pre-money or post-money? And what share count is being used to calculate it?

Those aren't technical side notes. They change dilution. If the option pool is expanded before the financing closes, founders usually absorb more of that dilution. If it's counted differently, the same valuation headline can produce a different ownership result.

A useful way to think about it is a pie. Valuation tells you how large the pie is assumed to be. The price per share tells you how that pie is sliced. The fully diluted capitalization table tells you who is standing in line for a slice.

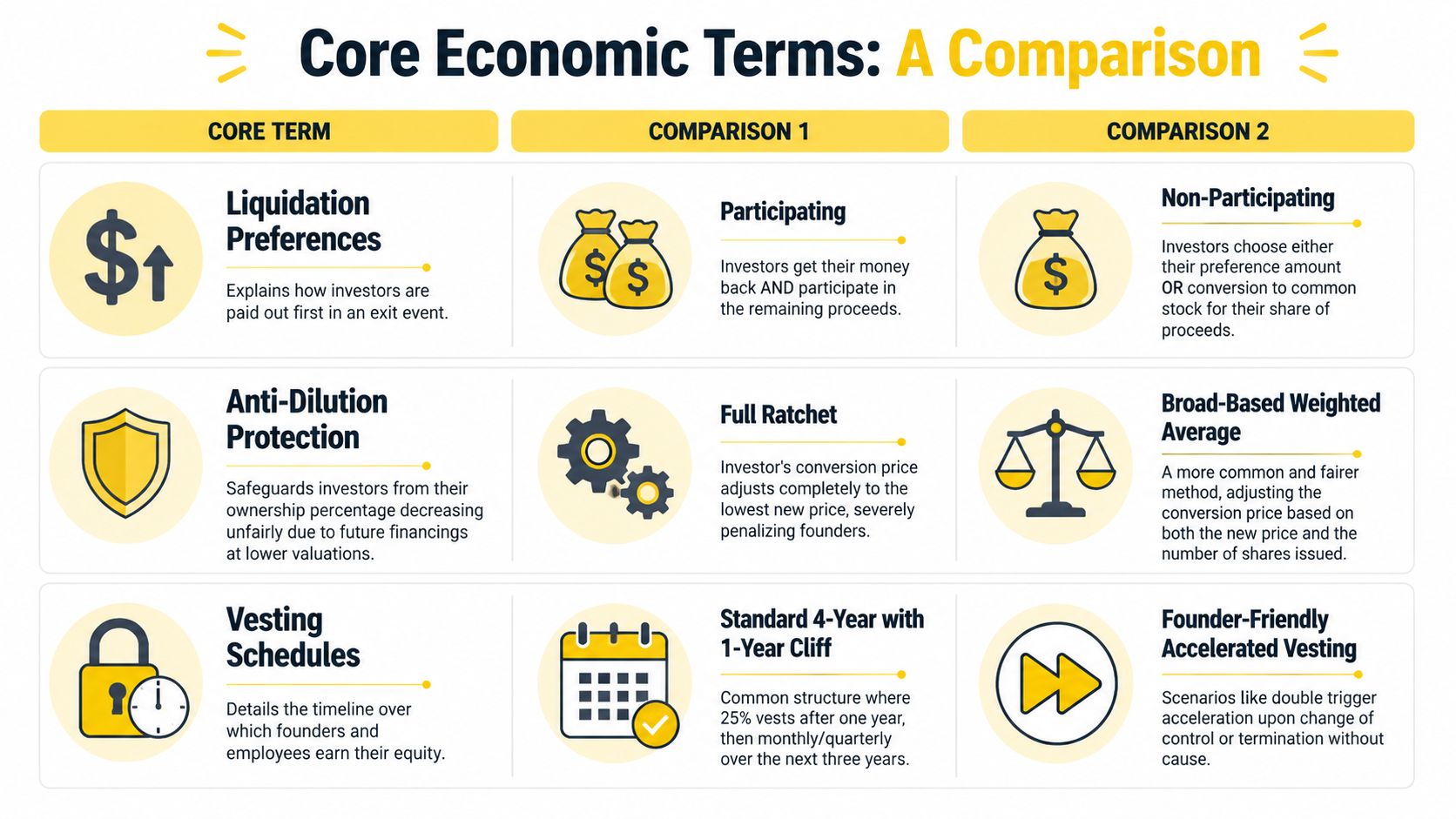

Liquidation preference

Liquidation preference determines who gets paid first if the company is sold, wound up, or goes through another exit event covered by the deal documents.

A founder-friendly version is usually 1x non-participating preferred. That means the investor generally chooses one lane. Either take back the original investment amount first, or convert into common and share pro rata with everyone else. A more investor-friendly structure is participating preferred, where the investor first gets the preference and then also participates in the remaining proceeds.

Participating preferred can make a middling exit feel much worse for founders than the headline valuation suggested.

This is one of the clearest examples of why valuation alone doesn't tell you the deal economics.

Anti-dilution protection

Anti-dilution rights protect investors if the company later sells shares at a lower price. The key question is the adjustment formula.

Full ratchet is usually hard on founders and existing common holders because it resets the investor conversion price to the new lower price, regardless of how many shares the company issues. Broad-based weighted average is more balanced because it takes into account both the lower price and the number of shares issued in the down round.

That distinction matters in bad markets. If the company needs bridge capital, the anti-dilution formula can shift a lot of downside onto founders and employees.

Why these terms must be read together

Economic terms work as a package, not as isolated clauses.

- Valuation affects initial ownership.

- Option pool treatment affects founder dilution before closing.

- Liquidation preference affects exit distributions.

- Anti-dilution affects future dilution if the next round is weaker.

- Price per share ties the whole structure together.

A founder can accept a fair valuation and still give away too much economics elsewhere. That's why I usually tell clients to mark up the term sheet while looking at the cap table and an exit waterfall side by side, not in separate conversations. Once the deal moves into the definitive stock purchase agreements, changing the economic architecture is harder.

Understanding Key Control Provisions

The investor isn't just buying economics. The investor is buying influence over how the company is run. The three control points that matter most are board composition, protective provisions, and voting rights.

Board composition

Board seats shape the company before any formal vote happens. A board with founder control feels different from a board with one founder seat, one investor seat, and one independent acceptable to both sides. The paper may say everyone owes duties to the corporation, which is true, but the lived reality is that board makeup affects hiring, budgets, acquisitions, and future financings.

A founder should ask two practical questions. Who appoints each seat? And what happens if a founder stops being an employee or if the investor sells part of the position?

Protective provisions

Protective provisions are investor consent rights over major actions. They often cover issuing new shares, changing share rights, taking on significant debt, selling the company, changing board size, paying dividends, or amending constating documents.

These rights are where a “minority” investor can still block important steps.

A term sheet can leave founders with day-to-day operating control but still require investor approval for the decisions that matter most.

Consider a common scenario. The company is missing revenue targets and wants a short-term debt facility to extend runway. Management thinks it's ordinary course financing. The term sheet, however, gives preferred holders a veto over debt above a modest threshold. The investor refuses unless the company also agrees to tighter reporting and a board observer. The founder hasn't lost formal control of the business, but the company can't take a material financing step without investor consent.

Voting rights

Voting rights answer a different question. Do the preferred shares vote with common on an as-converted basis, or do investors also get separate class votes on certain matters?

That separate class vote can matter more than the board seat. If a transaction needs approval of preferred voting as a separate class, investors can block it even when a majority of all shareholders support it.

If your company is Canadian, these rights also need to fit within the corporation's governing documents and local statute. The high-level concept may be familiar, but the mechanics need to be adapted to your articles and shareholder approval framework. If you need a refresher on the internal rules that sit underneath those approvals, review the role of company bylaws.

Investor vs Founder Levers in a Negotiation

Negotiation works better when founders stop treating every term as moral and start treating terms as trade-offs. Investors are trying to reduce downside, preserve governance influence, and protect follow-on rights. Founders are trying to preserve upside, keep operational flexibility, and avoid future financing traps.

A clean way to approach the discussion is to compare each ask with a realistic counter.

Key term negotiation levers

| Term | Investor-Friendly Position (Initial Ask) | Founder-Friendly Position (Target Counter) |

|---|---|---|

| Liquidation preference | Participating preferred, broad exit coverage | 1x non-participating, clear deemed liquidation limits |

| Anti-dilution | Full ratchet | Broad-based weighted average |

| Board control | Investor seat plus strong approval rights | Balanced board, narrow reserved matters |

| Protective provisions | Long list covering many operating decisions | Limited list for fundamental changes only |

| Pro rata rights | Broad rights with expansion ability | Standard pro rata, limited super rights |

| Option pool | Increase pool before closing | Share dilution burden more evenly |

| Redemption rights | Early investor put-style exit pressure | Remove or delay heavily |

| Tranched funding | Later closings tied to milestones drafted tightly for investor discretion | Objective milestones, cure periods, automatic funding if achieved |

The rise of tranched or milestone-based financings is worth special attention. Recent updates to the NVCA model stock purchase agreement formalize later closings tied to specific milestones, and that changes the balance of influence, timing risk, and closing certainty for both sides (Foley analysis).

What usually works

Founders get better outcomes when they rank issues. If liquidation economics matter most, trade on board mechanics. If control is the core concern, don't spend all your negotiation capital on a minor drafting point in the information rights section.

What doesn't work is arguing that every investor protection is “non-standard.” The stronger response is narrower. Accept the concept, then narrow the trigger, define the threshold, add objective standards, or limit the duration.

For employee equity, the negotiation should also line up with future hiring. A term sheet that squeezes the common too hard can make the option pool less effective later. That's one reason to review how startup stock options fit into the financing model before the round closes.

What Are Common Red Flags in a Term Sheet?

Some terms aren't automatically unacceptable, but they should trigger a hard second look because they can distort the economics or freeze management.

Watch for these issues

-

Participating preferred with no meaningful limit

This can let investors recover their money first and still share in the rest. In modest exits, founders and employees may receive far less than expected. -

Protective provisions that reach ordinary operations

Investor approval for fundamental changes is normal. Investor approval for ordinary hiring, budget changes, debt within ordinary course, or minor commercial decisions can make the company hard to run. -

Super pro rata rights

Standard pro rata lets an investor maintain ownership. “Super” rights can let them increase ownership in future rounds, crowding out new money and compressing room for strategic investors. -

Redemption rights with real pressure behind them

If investors can force the company to repurchase shares, management may end up negotiating under financial stress rather than focusing on growth. -

Ambiguous milestone tranches

If a second closing depends on milestones, those milestones must be objective. “Investor satisfaction” language or vague commercial targets can turn committed capital into optional capital.

If a term gives the investor broad discretion after signing, assume it will matter most when the company is under pressure.

A founder should also pay attention to how many of these terms appear together. One aggressive term may be manageable. Several in the same sheet usually signal a much more investor-controlled deal than the headline summary suggests.

An Annotated Sample Clause Liquidation Preference

A liquidation preference clause looks dense because it compresses business logic into legal language. Here's a simple example of a standard non-participating formulation:

In the event of any liquidation, dissolution or winding up of the Company, either voluntary or involuntary, the holders of Preferred Stock shall be entitled to receive, prior and in preference to any distribution to the holders of Common Stock, an amount equal to the Original Purchase Price for each share of Preferred Stock, plus any declared but unpaid dividends. If the assets available for distribution are insufficient to pay such amount in full, the entire assets of the Company shall be distributed ratably among the holders of Preferred Stock in proportion to the full amounts to which they would otherwise be entitled.

What this means in plain English

“Prior and in preference” means the preferred gets paid before common receives anything. Founders and employees usually hold common, so this is the payment order.

“Original Purchase Price” is the investor's baseline recovery amount per preferred share. In a 1x preference, the investor is generally looking first to recover the original investment amount.

“Declared but unpaid dividends” may be irrelevant in many venture deals if no dividend is ever declared, but it still belongs in the reading.

What founders should ask

Ask whether the clause is strictly non-participating or whether another section lets the investor take the preference and then share again. Also ask what counts as a deemed liquidation event. A merger or asset sale can be treated as a liquidation for payout purposes even though the company is not formally dissolving.

That's where many founder misunderstandings happen. The clause sounds like it only applies in failure scenarios, but the definition often extends to successful exits too. If you want a broader primer on the underlying security, review how preferred stock works before negotiating the payout language.

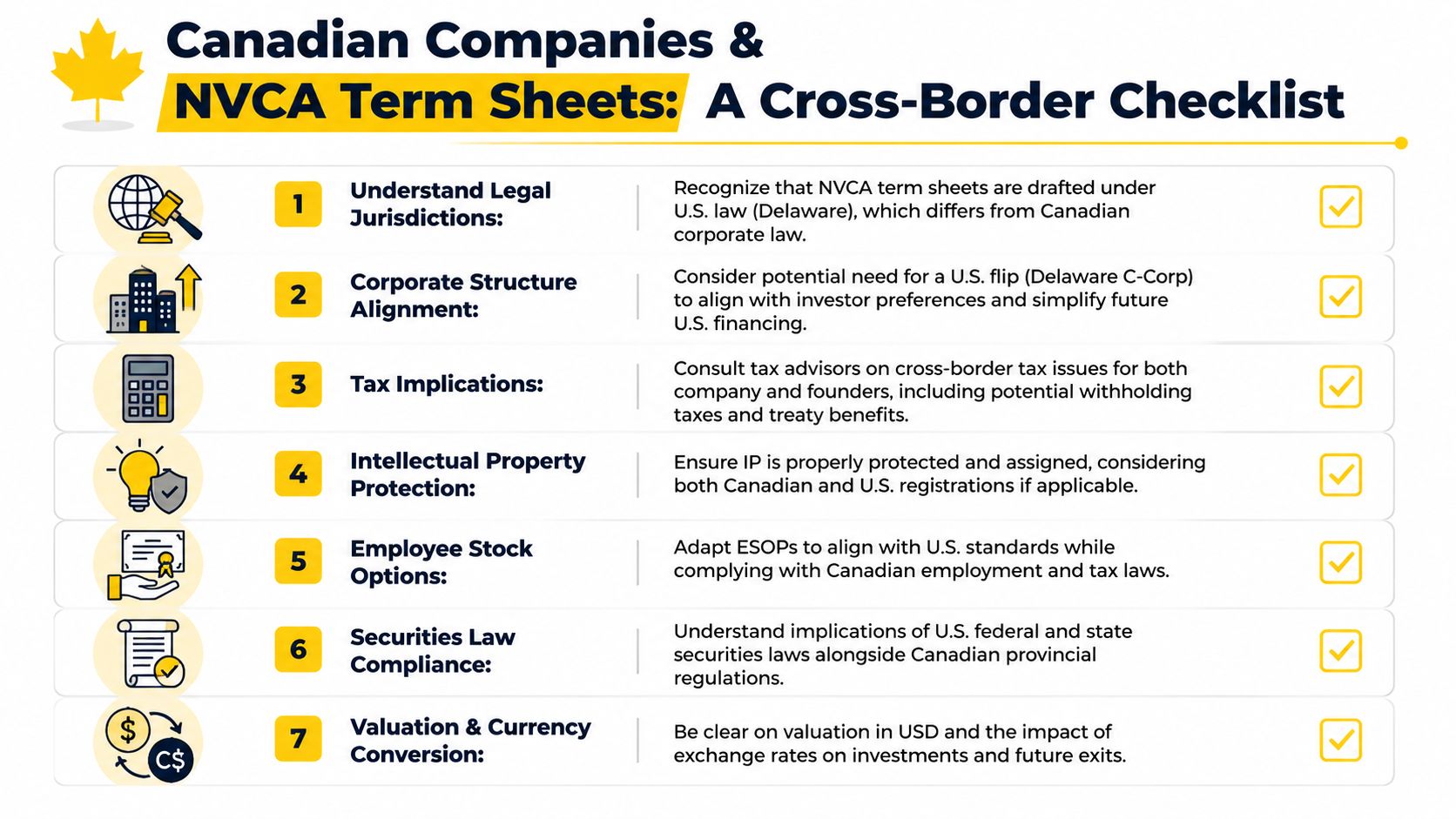

How an NVCA Term Sheet Works for Canadian Companies

A Canadian founder gets a U.S. NVCA term sheet on Friday, agrees with most of the economics by Monday, and then loses two weeks on points that were never obvious from the headline terms. The friction usually comes from implementation under Canadian corporate, securities, tax, and employment rules, not from the valuation or the size of the round.

That is the practical reality of cross-border venture deals. The NVCA form gives U.S. investors a familiar template, but many of its assumptions come from Delaware practice. Canadian companies can still use it effectively. The work is translating U.S. concepts into a Canadian company's articles, approvals, equity plan, and closing steps without changing the business deal by accident.

Canadian and U.S. venture terms often line up at a high level, which is why the NVCA form is commonly used as the starting paper in cross-border financings. The legal plumbing does not always line up. A founder should treat the term sheet as the commercial outline, then ask which terms need Canadian drafting changes, which terms may require a pre-closing reorganization, and which U.S. requests are really investor preference rather than true deal requirements. For a practical overview of the U.S. document set, see Cooley Go on NVCA financing documents.

Cross-border checklist for Canadian founders

-

Corporate statute fit

Confirm whether the company is organized under the CBCA, OBCA, or another provincial statute. Then check whether the proposed preferred share rights, protective provisions, and conversion mechanics can be implemented cleanly in the articles. -

Delaware flip analysis

Decide early whether the investor requires a Delaware parent. Some U.S. funds strongly prefer it because later rounds, option administration, and counsel workflows are simpler. Others are comfortable investing in a Canadian entity if the cap table, IP, and governance are tidy. A flip can help on one front and create tax, timing, and employee equity issues on another. -

Articles and approvals

Many NVCA terms assume rights that sit in a U.S. certificate of incorporation. In Canada, those rights may need to be built into amended articles and approved under the company's governing statute and existing shareholder arrangements. -

Canadian securities compliance

The financing still has to fit Canadian prospectus exemptions and local filing requirements in the relevant provinces. The U.S. side matters too, especially if the offering relies on private placement exemptions. Founders can review the regulator's overview at SEC guidance on exempt offerings. -

Tax planning before documents are finalized

Reorganizations, share exchanges, founder rollovers, and cross-border holding structures can produce tax results that are hard to reverse later. Term sheet language around structure, option pool sizing, and pre-closing steps should be checked against tax advice before anyone treats those points as settled. -

Equity incentive plan alignment

U.S. investors often expect an option plan that looks familiar to their market. Canadian tax and employment rules may call for different documentation, different award design, or a different approach for service providers in each country. -

IP chain of title

Investors will expect clean ownership and assignment records, especially where founders, contractors, or affiliates have worked in both Canada and the U.S. Cross-border deals slow down quickly when IP was developed in one entity and raised capital in another. -

Currency, reporting, and board assumptions

If the round is priced in U.S. dollars but the company operates mainly in Canada, the board should be explicit about FX exposure, reporting conventions, and how performance targets will be measured after closing.

Where Canadian founders usually gain or lose ground

The main negotiation point is not always whether a term is market. It is whether a U.S. term can be implemented in Canada without giving the investor more than the term sheet appears to say.

A simple example is board and veto language. A U.S. investor may ask for consent rights drafted around Delaware concepts and a clean charter structure. In a Canadian company, the same protection may need to be split across articles, a shareholders' agreement, and board approval mechanics. That drafting exercise can narrow or expand the investor's practical control depending on how carefully it is done.

Founders should also separate true investor priorities from inherited drafting. If a fund cares about information rights, board approval over major actions, and a standard 1x non-participating preference, there may be room to keep the Canadian entity in place. If the fund is underwriting for a fast U.S. Series A, broad employee option grants, and eventual U.S. acquirer diligence, a Delaware parent may become part of the price of admission.

What usually causes delay

Delay usually comes from four places at once. Corporate cleanup, tax structuring, equity plan revisions, and IP confirmation all tend to move on separate tracks, often with different advisors and different timelines.

Founders can reduce that delay by asking a short set of questions as soon as the term sheet arrives: Are we keeping the Canadian entity or adding a U.S. parent? Which rights must go into the articles? Which approvals do existing shareholders need to give? Do our option plan and IP assignments survive diligence in both countries?

Cross-border NVCA deals work well when those questions are answered early and documented clearly. The term sheet is only the starting point. For Canadian companies, the legal outcome depends on how the U.S. form is translated into Canadian reality.

Frequently Asked Questions

Is an NVCA term sheet legally binding?

Usually only parts of it are. The economic and governance terms are commonly non-binding, while confidentiality, exclusivity, expense allocation, and governing law provisions may be binding if drafted that way. Founders shouldn't assume “term sheet” means informal. Some clauses can restrict your conduct immediately, especially if you agree not to shop the deal while documents are being drafted.

How much does it cost to negotiate an NVCA term sheet?

Legal cost varies with the complexity of the round, whether the company is already well-organized, and whether there's a cross-border element. A Canadian company taking a U.S. term sheet usually spends more than a domestic one-entity financing because counsel may need to review articles, securities exemptions, tax planning, and option structure. The cheapest draft is rarely the cheapest outcome if the terms are wrong.

How long does it take to go from term sheet to closing?

That depends on how settled the key points are. A straightforward deal with aligned counsel moves faster than one with multiple side issues, milestone tranches, or a cross-border reorganization. Timing often slips because of diligence and implementation, not because the headline business terms are difficult. Regulatory guidance may also matter depending on the structure, including Canadian federal corporate resources.

Can a Canadian corporation use an NVCA term sheet without reincorporating in Delaware?

Yes, sometimes. The core economics and governance terms may still work well as a negotiating framework. The question is whether the rights can be implemented efficiently under the applicable Canadian corporation statute and whether the investor is comfortable investing into that structure. Some funds insist on a Delaware parent. Others don't, especially if the Canadian structure is already clean and the legal adjustments are manageable.

What's the biggest risk for founders signing too quickly?

The biggest risk is focusing on valuation and overlooking preference, control, and implementation terms. Founders often discover the underlying issue later, when they try to raise the next round, approve debt, grant options, or sell the company. A term that looked “standard” in a U.S. template may create friction when mapped onto a Canadian company's articles, tax plan, or shareholder approvals.

A U.S. NVCA term sheet can be a useful starting point. It gives both sides a common language and usually speeds up the first phase of negotiation. But founders shouldn't confuse a familiar template with a harmless one, especially when the company is Canadian and the investor is U.S.-based.

The practical work is in the details. Read the economics with the cap table beside you, read the control provisions with a future board dispute in mind, and read the cross-border mechanics before you accept the investor's version of “standard.”

How Mayo Law Can Help

A Canadian founder can accept an NVCA term sheet in a weekend and spend the next month discovering that the actual work starts after the signature. The pressure point is rarely the headline valuation. It is the gap between a U.S. form and the Canadian company that has to implement it cleanly.

Mayo Law advises on that gap. We review the business deal, then test whether the paper can be carried into the company's articles, shareholder approvals, option plan, securities filings, and tax structure without creating avoidable friction in the next round or at exit.

For Canadian companies dealing with U.S. investors, that usually means identifying the points where a Delaware-style term sheet needs adjustment under CBCA or provincial corporate law, deciding whether the existing structure should stay in place or be reorganized, and documenting the investor rights in a way that works on both sides of the border.

If you are reviewing an NVCA term sheet for a Canadian company, Mayo Law can help you spot the key negotiation levers, mark up the terms that matter, and prepare a practical U.S.-Canada implementation checklist before the deal hardens into definitive documents.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles