Published: June 21, 2026

Updated: June 21, 2026

Read time: 12 minutes

When a U.S. company sells into Canada, licenses software to Canadian customers, or centralizes IP in a U.S. corporation while operating through a Canadian affiliate, the tax question usually arrives late. By then, contracts are signed, transfer pricing is set, and the structure is harder to unwind. The Section 250 deduction can materially change the economics of that setup, but only if the company fits the rule and documents it properly.

At Mayo Law, we help companies in Toronto, the GTA, and across the border handle cross-border legal and tax-adjacent structuring that often touches both U.S. and Canadian issues. For businesses with U.S. operations, export revenue, or Canadian subsidiaries, Section 250 often matters long before the return is filed.

What Is the Section 250 Deduction

Section 250 is a U.S. corporate tax deduction that generally allows a domestic corporation to deduct part of its foreign-derived intangible income and part of its global intangible low-taxed income, subject to statutory rules and limits. It was created under the Tax Cuts and Jobs Act for tax years beginning after December 31, 2017.

For tax years through December 31, 2025, Section 250 generally allows a domestic corporation to deduct 37.5% of FDII and 50% of GILTI, subject to a taxable-income limitation, according to the IRS newsroom explanation of Section 250. For tax years beginning after December 31, 2025, those percentages are scheduled to drop to 21.875% and 37.5%.

Why CFOs care

This provision sits at the center of the post-2017 U.S. international tax regime because it links a favorable deduction to two very different fact patterns. One is export-linked income earned by a U.S. corporation. The other is income picked up from controlled foreign corporations.

For a U.S.-Canada group, that creates a practical planning split:

- U.S. operating company selling into Canada: FDII may be in play.

- U.S. parent owning a Canadian subsidiary: GILTI may be in play.

- Group with both models: both baskets may matter, but they don't work the same way.

What Section 250 is trying to do

In plain English, Congress used Section 250 to make the U.S. more attractive as a place to hold and exploit business value that isn't tied only to tangible assets. That often means software, brand, know-how, customer relationships, and service capability, even though the statutory formulas use terms that don't map neatly to business jargon.

Practical rule: If your U.S. company earns revenue from foreign customers or owns foreign subsidiaries, assume Section 250 deserves a review. Waiting until year-end usually means you're testing facts you should have built into contracts and reporting earlier.

A common mistake is treating Section 250 as an accounting exercise. It isn't. It affects where groups place IP, how they draft intercompany agreements, how they support foreign use, and whether a U.S. corporation should remain the principal contracting party for Canadian business.

Eligible Taxpayers and Qualifying Income

The first screen is simple. The second is not.

Who can claim it

Section 250 applies to a domestic C corporation. If a group is operating through a partnership, S corporation, or directly through individuals, the rule usually won't fit the way many founders expect. That corporate status point sounds basic, but it is often where planning starts or stops.

If the U.S. entity's organizational documents and tax classification haven't been reviewed in a while, it helps to confirm the basics before analyzing Section 250. A good starting point is understanding the underlying U.S. entity record, including the certificate of incorporation.

What income counts

Section 250 covers two separate income categories.

FDII

Foreign-derived intangible income, or FDII, is the export-facing side of the rule. In business terms, it generally targets income a U.S. C corporation earns from serving foreign markets, including sales of property or services to foreign persons for foreign use.

For U.S.-Canada companies, the practical issue usually isn't the label. It's proof. You need the transaction facts to support that the income is foreign-derived, and the contract trail matters. If the U.S. seller invoices a Canadian customer but the actual use is in the United States, the analysis can shift fast.

GILTI

Global intangible low-taxed income, or GILTI, is different. It doesn't focus on customer location. It arises from the U.S. tax treatment of income connected to controlled foreign corporations.

That means a U.S. corporation with a Canadian subsidiary may have a Section 250 issue even if the U.S. company never directly sells to Canadian customers. The deduction in that setting is tied to the U.S. inclusion from the foreign corporation, not to export revenue booked in the United States.

A lot of confusion comes from treating FDII and GILTI as variations of the same rule. They sit in the same section, but they respond to different business structures and different compliance risks.

What works and what doesn't

Some structures line up well with Section 250. Others don't.

- Often workable: A U.S. C corporation contracts directly with Canadian customers and performs from the United States.

- Often workable: A U.S. parent owns a Canadian operating subsidiary and models the GILTI impact at the parent level.

- Often weak: A group assumes all Canadian revenue qualifies without testing foreign use.

- Often weak: Founders expect pass-through entities to get the same result as a domestic C corporation.

The main point is that eligibility is less about broad international activity and more about matching the taxpayer, the income category, and the underlying legal facts.

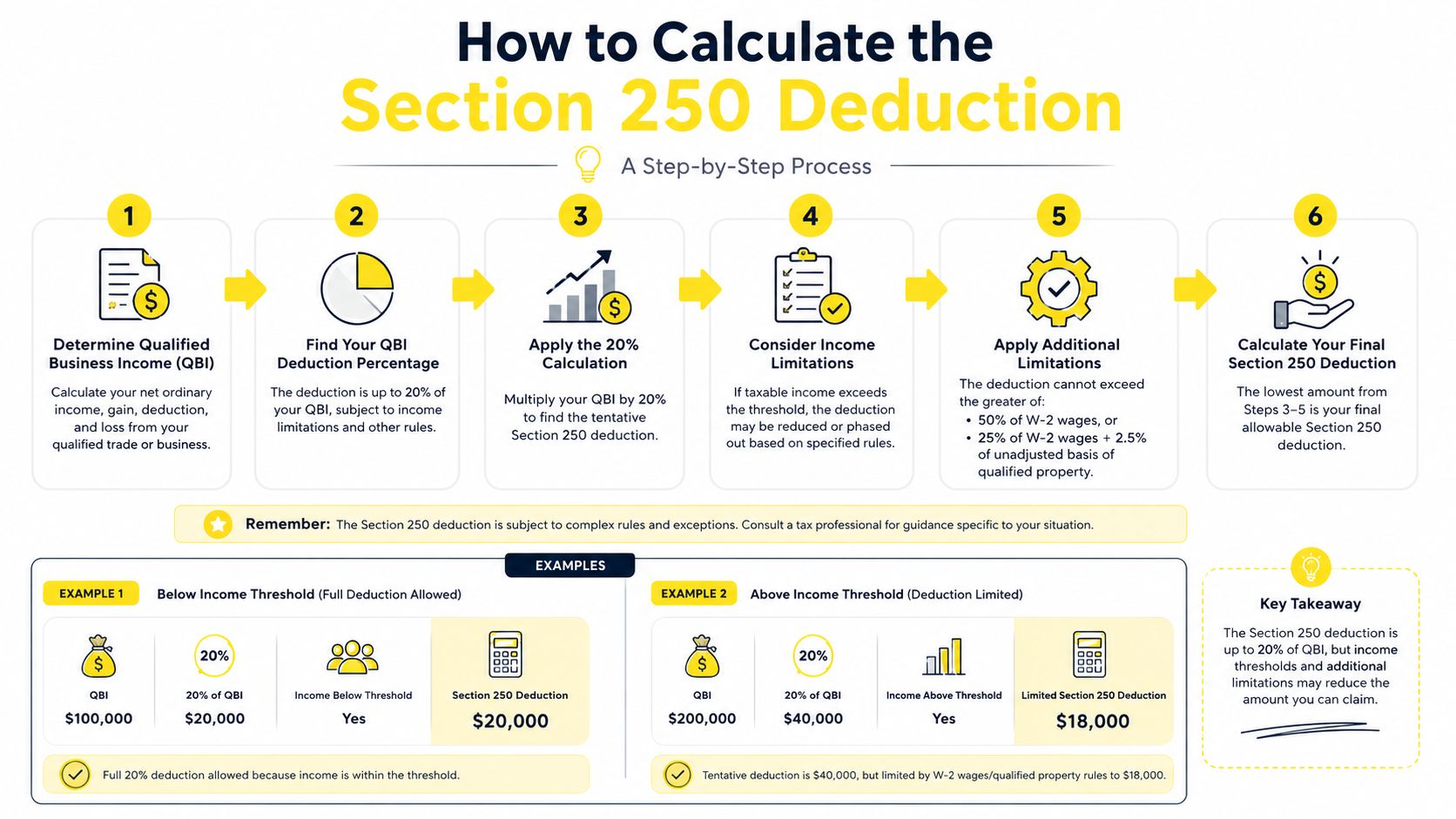

How to Calculate the Section 250 Deduction with Examples

The FDII side is formula-driven. That's useful because it gives finance teams a defined sequence, even if the inputs require judgment.

The IRS explains the core mechanics this way: a domestic C corporation computes deduction eligible income (DEI), subtracts a routine return equal to 10% of qualified business asset investment (QBAI) to reach deemed intangible income (DII), and then multiplies that amount by the foreign-derived ratio, FDDEI ÷ DEI, to determine the amount eligible for the deduction, as described in the IRS practice unit on the Section 250 FDII calculation.

The rate table

| Income Type | Tax Years Before Jan 1, 2026 | Tax Years After Dec 31, 2025 |

|---|---|---|

| FDII | 37.5% | 21.875% |

| GILTI | 50% | 37.5% |

A practical sequence for FDII

- Identify the U.S. C corporation's DEI.

- Determine its QBAI.

- Compute the routine return equal to 10% of QBAI.

- Subtract that amount from DEI to arrive at DII.

- Compute the foreign-derived ratio, FDDEI ÷ DEI.

- Apply that ratio to DII to isolate the foreign-derived amount.

- Apply the Section 250 deduction percentage in effect for that tax year.

That's the framework. The hard part is usually not arithmetic. It's classifying revenue correctly, identifying the right assets, and maintaining records that support the foreign-derived ratio.

Example using a U.S.-Canada structure

Assume a U.S. C corporation develops software in the United States and licenses it to Canadian business customers. It also owns a Canadian subsidiary that handles local marketing and support. The U.S. corporation wants to know whether its direct Canadian revenue may generate FDII and whether the Canadian subsidiary creates a separate GILTI inclusion issue.

On the FDII side, the U.S. corporation starts with DEI. It then identifies its QBAI and subtracts the routine return equal to 10% of that QBAI. That produces DII. If only part of its DEI is foreign-derived, it multiplies DII by the foreign-derived ratio rather than assuming all DII qualifies.

On the GILTI side, the analysis is separate. The U.S. corporation doesn't fold the Canadian subsidiary's results into the FDII formula. Instead, it evaluates the U.S. inclusion tied to the foreign corporation and then applies the Section 250 rules that relate to GILTI.

A startup that compensates key personnel with equity should also make sure the corporate tax model reflects the broader capitalization picture, including any startup stock options planning that affects ownership and cross-border group design.

Where examples usually break down

Finance teams often build a spreadsheet that looks clean but relies on assumptions that won't survive review. The common trouble spots are:

- Foreign use support: Invoices alone usually don't tell the full story.

- QBAI classification: Asset categorization can distort the routine return.

- Mixed functions: A U.S. entity may perform part of the work, while a Canadian affiliate performs another part.

- Taxable-income limitation: A mathematically correct draft calculation can still be capped.

Don't let the formula create false confidence. If the legal characterization of the transaction is loose, the calculation will only be precisely wrong.

Understanding the GILTI and FDII Interplay

FDII and GILTI are connected by the same code section, but they push in different directions.

They answer different policy concerns

FDII is the incentive side. It rewards a domestic corporation for earning qualifying foreign-market income from the United States.

GILTI is the anti-deferral side. It pulls certain foreign corporation income back into the U.S. tax base. The Section 250 deduction for GILTI softens that result, but it doesn't turn GILTI into an export incentive.

That distinction matters when a board asks a simple question: should we keep the value driver in the United States or move it to Canada? Section 250 doesn't answer that alone, but it changes the math.

Two common business profiles

U.S. export hub

A U.S. company develops the product, signs contracts with Canadian customers, and performs core functions from the United States. In that setup, the company often focuses first on FDII. The planning work is operational. Where are services performed? Who is the contracting party? How do you document foreign use?

Foreign subsidiary model

A U.S. parent owns a Canadian operating company that earns active income in Canada. That structure often raises GILTI issues at the U.S. level, even if the U.S. company does not itself have large direct export revenue. The planning work is more about ownership, tested income exposure, and the interaction between U.S. and Canadian tax profiles.

Why groups often have both

Many middle-market groups operate with a hybrid model. The U.S. entity owns the IP and contracts for some foreign sales, while a Canadian subsidiary handles local distribution, implementation, or support. In that case, the company may have both FDII-type and GILTI-type issues, but not because the same dollar of income fits both buckets.

Instead, the structure produces separate consequences in separate places.

The most effective planning usually starts with a map of functions, assets, and contracts, not with a tax form. Once the business facts are clear, you can tell whether the U.S. company is acting like an export principal, a foreign-parent owner, or both.

For technology-heavy groups, this often overlaps with the legal treatment of software and know-how arrangements. A weakly drafted technology licensing agreement can create tax ambiguity where the business thought it had certainty.

Filing Mechanics Recordkeeping and Audit Risks

The Section 250 deduction is claimed through Form 8993. That's the filing vehicle, but significant work happens before the form is prepared.

What the compliance file needs

For FDII, companies need support for the foreign-derived character of the income. In practice, that means pulling together the customer contract, invoice flow, service description, delivery facts, and evidence of foreign use or foreign recipient status where relevant.

For groups with a Canadian affiliate, the file should also be internally consistent across tax, legal, and operational records. If the intercompany agreement says one entity performs a function, but employees and system access logs suggest another entity did it, the story gets harder to defend.

Records that matter most

- Customer agreements: These should describe who buys what, from whom, and for what territory or use.

- Intercompany agreements: These should align with transfer pricing and actual conduct.

- Revenue mapping: The company should be able to trace revenue to transaction type, customer location, and business line.

- Asset records: QBAI inputs need support from fixed-asset and tax records.

- CFC reporting package: If GILTI is part of the picture, the U.S. reporting should reconcile to the foreign subsidiary data.

A governance review is often worthwhile when multiple entities are involved, especially if the group hasn't recently updated ownership and reporting controls around beneficial ownership reporting requirements.

Audit risk usually comes from inconsistency

The IRS doesn't need a dramatic fact pattern to challenge a Section 250 position. Ordinary sloppiness is enough.

Common pressure points include foreign-use documentation that doesn't go beyond billing address data, intercompany pricing that doesn't match the legal agreements, and QBAI calculations prepared in isolation from the fixed-asset ledger. Another recurring issue is treating labels as decisive. Calling something a service fee or a license doesn't settle the tax characterization if the underlying rights transferred suggest something else.

Watchpoint: If the tax team can't explain the transaction in plain English without resorting to spreadsheet labels, the deduction position probably needs more work.

This is one of those areas where prevention is cheaper than repair. By the time the company is responding to document requests, the best planning opportunities are usually gone.

Strategic Planning for US-Canada Cross-Border Companies

For U.S.-Canada companies, Section 250 planning only works if the legal structure, transfer pricing, and commercial model all point in the same direction.

Where to locate IP

This is usually the first strategic question. A group may instinctively place IP in Canada because development leadership sits there, or in the United States because the U.S. company signs the larger contracts. Section 250 adds pressure to analyze that choice more carefully.

A U.S. corporation that owns and exploits IP into foreign markets may support FDII exposure. But that doesn't mean U.S. ownership is always better. Canadian tax treatment, transfer pricing, withholding, and future exit planning can pull the other way. The right answer depends on how the business earns money.

Intercompany agreements should match operations

A lot of cross-border groups paper the structure after the fact. That's where problems start.

If the Canadian company is performing meaningful development, enhancement, maintenance, protection, or exploitation functions, the agreements should say so and the pricing should reflect it. If the U.S. company is the true principal for Canadian sales, contracts, invoicing, and personnel conduct need to look like a principal structure in real life.

Two anonymized scenarios

Scenario one

A U.S. software company sells subscriptions directly to Canadian customers while a Canadian affiliate provides onboarding and support. The company assumes all Canadian revenue is favorable for U.S. Section 250 purposes.

That's too simple. The better approach is to separate contracting, delivery, and support functions, then test which income is tied to the U.S. corporation's foreign-derived activities and whether the affiliate's role changes the transfer-pricing story.

Scenario two

A Canadian parent forms a U.S. subsidiary to hold North American IP but leaves legacy licensing rights and development obligations in Canada. The structure looks efficient on an org chart but produces mixed signals in agreements, payroll, and product governance.

In practice, that kind of split often creates more risk than benefit until the legal documents and operating behavior are aligned.

Mayo Law works with companies across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, so clients with U.S. ties coordinate their legal work in one place rather than juggling two firms.

What tends to work

- Clear principal model: One entity owns the customer contract and bears the core entrepreneurial risk.

- Aligned IP chain: Ownership, development activity, and licensing rights are documented coherently.

- Consistent transfer pricing: The legal agreement and the pricing model tell the same story.

- Early review before expansion: It's much easier to design this before launching than to rebuild it later.

For founders planning market entry on both sides of the border, the larger structuring question often starts before tax modeling, especially when deciding how to start a business in both Canada and the US.

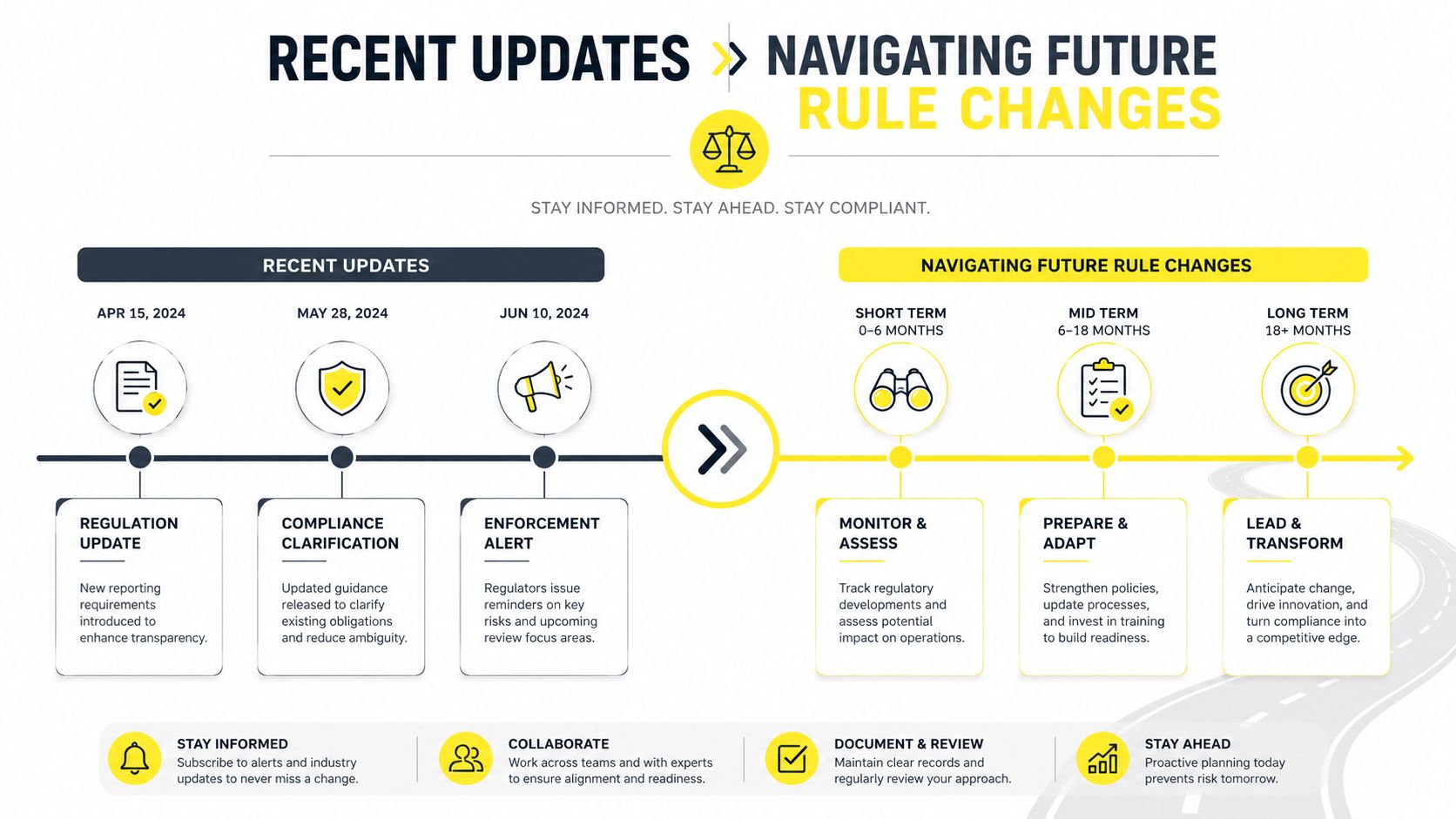

Recent Updates and Navigating Future Rule Changes

One of the most important recent developments is that Section 250 is no longer just about the classic FDII and GILTI computation many companies learned first.

The IRS issued Notice 2025-78 indicating its intent to issue proposed regulations on a new Section 250(b)(3) exclusion for income and gain from the sale or other disposition of certain property, including intangible property, and the guidance is expected to apply to dispositions after June 16, 2025, as summarized by Grant Thornton's discussion of the new Section 250 exclusions.

Why that matters for U.S.-Canada groups

This is especially relevant where a cross-border group is restructuring IP ownership, transferring intangible property, or entering a transaction labeled as a license that may be treated differently under general tax principles. Older Section 250 summaries often assume the main issue is whether foreign sales or CFC income fit the standard deduction framework.

That's no longer enough.

If a company is moving IP between U.S. and Canadian entities, or cleaning up an old structure, it now needs to ask at least two additional questions:

- Is this really a license, or could it be treated as a sale under general tax principles?

- If there is a sale or other disposition, does the new exclusion change whether the income remains in deduction eligible income?

The scheduled 2026 reduction

The other major planning point is already baked into the statute. For tax years beginning after December 31, 2025, the deduction percentages are scheduled to fall from 37.5% to 21.875% for FDII and from 50% to 37.5% for GILTI, based on the rule described in the earlier-cited IRS and RSM materials.

That isn't a technical footnote. It's a planning deadline.

Groups that expect significant foreign-derived income or meaningful GILTI exposure should model how the lower percentages affect the structure they already have. Some companies may decide to accelerate certain steps, revisit IP migration timing, or tighten documentation while the current framework is still in place.

If your cross-border group is considering an IP transfer, a deemed sale issue, or a U.S.-Canada restructuring, Section 250 now needs to be part of the transaction checklist from the start, not added after the draft documents are finished.

If your company is expanding between the United States and Canada, restructuring IP, or reviewing a U.S. subsidiary's tax position, Mayo Law can help coordinate the legal side of that cross-border planning with a practical view of the tax consequences. That includes business structuring, contracts, IP arrangements, and cross-border compliance issues that often drive the Section 250 analysis before the return is ever prepared.

How Mayo Law Can Help

Cross-border tax results often depend on legal facts your business creates long before filing season. Mayo Law serves clients across Toronto, the GTA, and on cross-border matters, helping businesses structure U.S.-Canada operations, contracts, IP ownership, and compliance processes in a way that reduces avoidable risk. To discuss your matter, visit international business legal services.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles