Published: June 25, 2026

Updated: June 25, 2026

Read time: 11 minutes

You may be at the point where smaller deals no longer move the needle. A GTA developer, family office principal, or operating business owner often gets there after a few successful acquisitions. The next deal is larger, the capital stack is tighter, and someone on the call says the obvious next step is private equity funds real estate.

That’s usually where confidence gives way to caution. The financial pitch sounds polished, but the legal paper is dense, the tax treatment crosses borders, and a U.S. vehicle can create risk for a Canadian investor in ways a domestic deal never would. At Mayo Law’s international business practice, we help clients in Toronto, the GTA, and across the border assist with these transactions with experience licensed in both Ontario and New York on a process that often spans both sides of the border.

What Is a Private Equity Real Estate Fund?

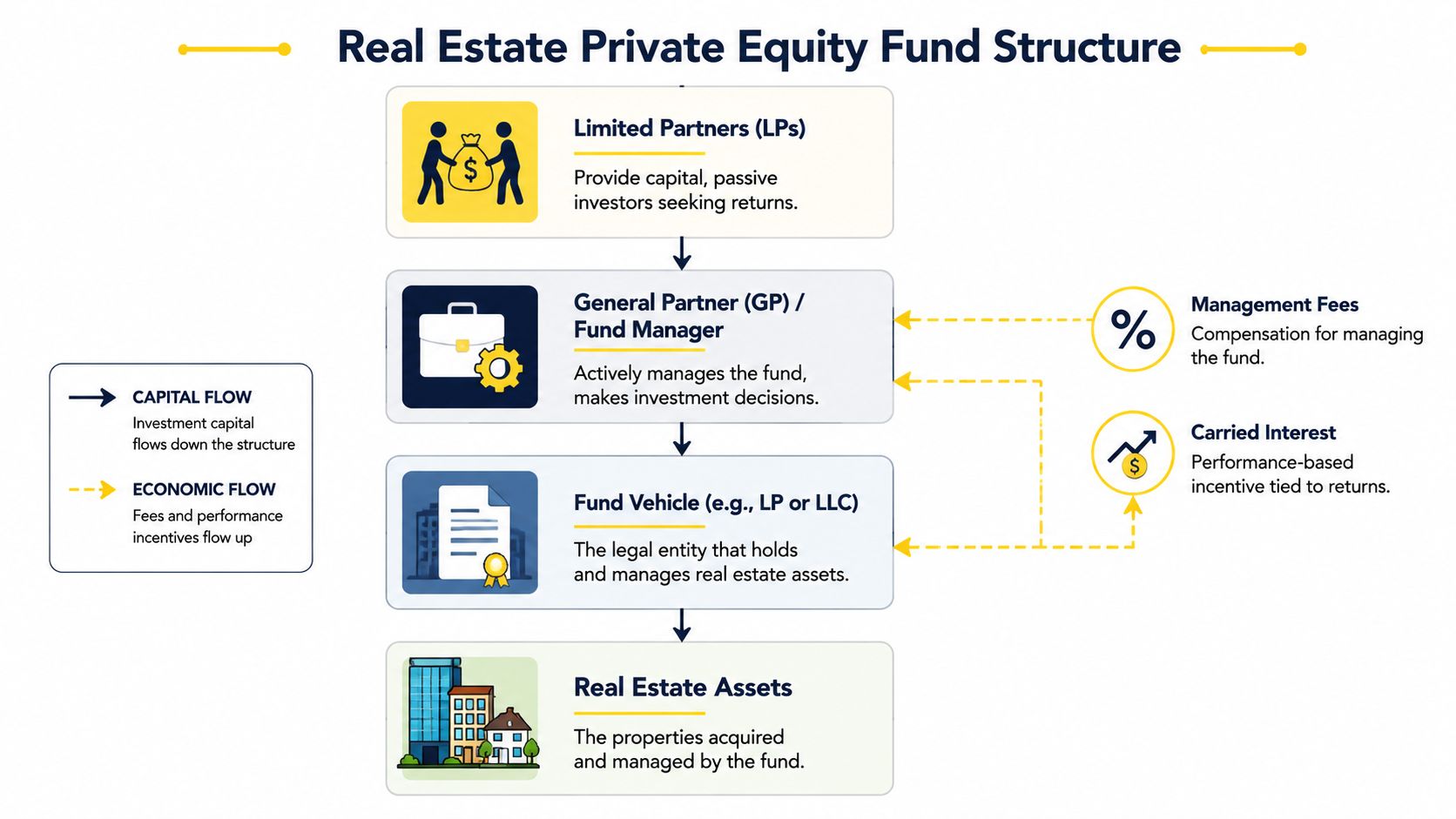

A private equity real estate fund is a professionally managed investment vehicle where a General Partner, or GP, pools capital from multiple investors, usually Limited Partners, or LPs, to acquire, manage, and sell real estate assets for profit over a defined investment period.

Think of it as a professional investment club, but one built for institutional-scale property. The GP finds deals, negotiates financing, supervises operations, and decides when to sell. The LPs usually provide capital and expect the GP to execute the strategy without giving each investor day-to-day control.

In practice, that division matters more than most first-time investors realize. If you’re reviewing a subscription package and side letter, you’re not buying a building directly. You’re buying into a legal and economic relationship. Your rights depend on fund documents, not on informal assumptions about how the sponsor “usually” treats investors.

A basic way to separate the moving parts is this:

- GP or sponsor: chooses the strategy, runs the deal, and earns promote if performance hurdles are met

- LPs: contribute capital and rely on negotiated protections in the fund documents

- Fund vehicle: often an LP or LLC that holds the investment

- Underlying assets: apartments, office, industrial, development sites, data centers, or mixed portfolios

Commercial real estate is the third-largest asset class in the United States, and CBRE projects overall commercial real estate investment activity will increase by 16% in 2026. The same CBRE source notes that performance is often measured by cash-on-cash return and equity multiple, where a 2.0x multiple means an investor has doubled their money.

That framework also helps explain why entity setup matters so much at the start. If you’re still sorting out how the investor entity should be formed before signing subscription documents, the question often connects back to corporate housekeeping, including basics such as what a certificate of incorporation does.

A first-time LP often focuses on the property story. Experienced counsel focuses on the governing documents first.

How Are Real Estate Private Equity Funds Structured?

Most real estate private equity funds are built as closed-end vehicles. That means investors commit capital for a finite term, the fund deploys that capital over an investment period, and the sponsor aims to exit assets before the fund winds up. According to the U.S. Government Accountability Office, these funds typically have a 5–7 year lifecycle. The same source notes that LPs receive return of capital plus a preferred return, often 6–8%, before the GP receives its promoted interest, which is typically 20% of profits after the hurdle is met.

The basic architecture

Most first-time investors will see some version of these layers:

-

Investor layer

LPs sign subscription documents and commit capital. -

Manager layer

The GP or affiliated manager controls deployment, reporting, and exit. -

Fund vehicle

Often a limited partnership, sometimes an LLC, occasionally with feeder entities. -

Property-level entities

Special purpose vehicles hold each asset or portfolio.

That sounds tidy on a diagram. It gets more complicated once there are co-investment rights, parallel funds, offshore feeders, tax blockers, and debt covenants that limit distributions.

How the waterfall actually works

The distribution waterfall is the part many investors skip until there’s a disagreement. Don’t. It determines who gets paid, in what order, and under what conditions.

A typical sequence looks like this:

- Return of capital: LPs first get back their contributed capital

- Preferred return: LPs then receive the agreed hurdle, often stated annually

- Catch-up: the GP may receive a larger slice until the economics align with the agreed split

- Carried interest or promote: remaining profits are split, with the GP taking its negotiated share

What works is a waterfall that is clear, testable, and illustrated with examples in the documents. What doesn’t work is vague drafting that leaves room for multiple interpretations of fees, reserves, and timing.

What is a preferred return in real estate?

A preferred return is the return threshold LPs typically receive before the GP shares in upside through carried interest. In a fund context, it helps align incentives by giving passive investors priority on early distributions, but the drafting matters because compounding, accrual, and catch-up language can change economics materially.

Why entity choice matters

A Canadian investor often assumes limited liability follows automatically from being called an LP. That assumption can fail if the structure is wrong or if the investor participates through an unsuitable entity. U.S. LLCs, limited partnerships, and blocker corporations can produce very different tax and liability outcomes.

For that reason, fund investing often starts before the fund does. It starts with the investor’s own structuring, governance, and authority chain, including whether the Canadian entity is properly organized through steps like incorporating a business in Ontario.

Practical rule: If you can’t trace who controls the fund, who holds the asset, and who gets paid first, you aren’t ready to subscribe.

The Spectrum of PERE Investment Strategies

Not all private equity funds real estate strategies belong in the same bucket. A fund buying stabilized apartment assets is doing something very different from a fund financing development, distressed repositioning, or niche sectors with operational complexity. If you miss that point, you can choose a fund that looks conservative in the deck but behaves aggressively in the documents.

The market context is worth keeping in mind. Private equity firms have acquired at least 11,800 apartment buildings containing nearly 3 million units, representing 13% of all U.S. apartment units, and 45% of those units were purchased since 2021, according to the Private Equity Stakeholder Project tracker. The same source states that 70% of private equity-owned units are concentrated in ten states, led by Texas.

PERE investment strategy comparison

| Strategy | Risk Profile | Typical Leverage | Target IRR | Asset Example |

|---|---|---|---|---|

| Core | Lower | Lower relative leverage | Not stated here quantitatively | Stabilized, fully leased institutional asset |

| Core-Plus | Moderate-low | Moderate relative leverage | 12–14% | Stable asset with light lease-up or renovation |

| Value-Add | Moderate | Higher relative leverage | 14–16% | Property needing operational improvement |

| Opportunistic | Higher | Often higher leverage, sometimes development-heavy | Qualitatively higher return target | Ground-up development or distressed repositioning |

The 12–14% and 14–16% benchmark ranges above come from the verified REPE benchmark data provided for Core-Plus and Value-Add strategies.

What investors usually get wrong

First, they treat the strategy label as enough. It isn't. I've seen “value-add” used for everything from ordinary renovation programs to highly execution-dependent redevelopment. The label matters less than the business plan, debt structure, and sponsor's decision rights.

Second, they focus only on projected upside. A better question is what has to go right for the model to work. In a Core-Plus deal, that may be modest leasing improvement. In an opportunistic deal, it may be zoning, construction, refinance availability, and a cooperative exit market all lining up.

What is an opportunistic real estate strategy?

An opportunistic real estate strategy targets higher-risk situations such as development, distressed assets, major repositioning, or niche sectors. It usually depends on active execution rather than stable in-place income, so investors should expect more moving parts, more sensitivity to financing conditions, and less tolerance for weak documentation.

A useful test is to ask where returns are supposed to come from. If the answer is mostly current income, you're likely closer to the left side of the spectrum. If the answer depends on redevelopment, recapitalization, or a specific market turn, you're further right.

Key Legal and Tax Issues for US-Canada PERE Investors

Generic fund guides typically prove insufficient when faced with the intricacies of cross-border PERE. The hardest problems in cross-border PERE are rarely the headline economics. They sit in tax classification, liability containment, sanctions screening, beneficial ownership, and document execution.

The Canadian LP problem inside a U.S. structure

A critical risk for Canadian LPs in U.S. funds is unforeseen GP liability if the fund uses a U.S. LLC structure without proper blocker entities. That can expose Canadian business assets to U.S. liabilities. The IRS FIRPTA guidance is a key reference point, and using U.S. C-Corps as blockers is a common strategy to prevent Canadian entities from being directly taxed on U.S. real estate income under those rules.

That doesn't mean every Canadian investor needs the same blocker. It means you should assume the default structure in the sponsor's memo was designed for the sponsor's convenience, not your cross-border tax posture.

Income classification and treaty friction

Canadian investors often ask whether they can treat their U.S. fund income as passive and move on. Sometimes they can't. The answer can turn on how the vehicle is classified, what the fund does, and whether the income is viewed as rental, business, effectively connected, or something else under U.S. tax rules and the U.S.-Canada treaty framework.

That's why the phrase “limited partner” can be misleading comfort. Limited economic rights don't automatically produce limited tax exposure.

How is rental income from U.S. property taxed in Canada?

Canadian residents generally report worldwide income to the CRA, which can include U.S. real estate income directly or indirectly received through an investment structure. The right analysis depends on the investor's entity, treaty position, foreign tax credits, and whether the U.S. structure creates direct exposure rather than a buffered return stream.

AML, KYC, and source-of-funds risk

Cross-border fund subscriptions trigger more compliance work than many investors expect. Sponsors, administrators, lenders, and sometimes title-side professionals may all ask for overlapping KYC packages. When funds are moving capital across the U.S.-Canada border, sloppy paperwork can create delays or worse.

Watch for these pressure points:

- Beneficial ownership: identify ultimate controlling persons early, especially where trusts or holdcos sit above the subscriber

- Document execution: notarization and apostille issues can stall closings if one side expects formal authentication

- Sanctions and AML screening: investor onboarding can pause if names, jurisdictions, or fund flows raise basic screening flags

- Authority evidence: resolutions, incumbency, and signing authority often matter more than the investor expects

If you're dealing with fund onboarding and entity transparency, the practical compliance work often overlaps with beneficial ownership reporting requirements, even when the underlying filing obligation sits outside the fund itself.

Mayo Law works with client types across the GTA and on cross-border matters. Joseph Mayo is licensed in Ontario and New York, so clients with U.S. ties coordinate their legal work in one place rather than juggling two firms.

If a subscription closes before tax, AML, and liability review are aligned, the investor may spend the next year fixing a problem created in one afternoon.

Two anonymized scenarios

A Mississauga business owner subscribed to a U.S. real estate fund through an operating company because it was “already there.” The fund accepted the investor, but the structure created avoidable tax friction and internal governance problems once distributions began. Re-papering later cost time and negotiating advantage.

In another file, a Toronto investor joined a U.S. LLC-based vehicle without asking how management authority was allocated. The commercial terms looked fine, but the governing documents gave broad discretion to affiliates and weak information rights to investors. The issue wasn't fraud. It was preventable imbalance.

Due Diligence, Valuation, and Exit Mechanics

A good fund doesn't just buy well. It investigates well, reports clearly, and exits on a timetable that supports returns rather than erodes them.

The three diligence tracks

The first track is financial diligence. That means testing rent rolls, arrears, concessions, operating statements, and assumptions behind the sponsor's business plan.

The second is physical diligence. Engineers, environmental consultants, and construction professionals determine whether the property can support the proposed strategy.

The third is legal diligence. Title, zoning, survey, entity authority, litigation, permit status, and contract assignability sit here. In cross-border deals, legal diligence also includes whether the investor's own entity can sign, fund, and receive distributions the way the model assumes.

How valuation affects the investor

Sponsors typically report asset values using accepted valuation approaches such as discounted cash flow analysis and capitalization-based methods. For LPs, the key point isn't mastering appraisal theory. It's understanding that reported value influences decision-making, reserves, refinancing posture, and whether the sponsor appears to be on track.

What works is consistent methodology and careful disclosure. What doesn't work is changing assumptions without explaining why.

Why exits deserve early scrutiny

The exit is where many projected returns either solidify or disappoint. A fund may sell assets one by one, sell a portfolio, recapitalize with a new partner, or refinance and return capital while holding longer through an extension right.

The SEC investor bulletin on private placements notes that shortening a holding period by 12 months can increase IRR by 1.5–2.0%. That is why sponsor execution matters so much. A capable GP doesn't just buy the right asset. The GP keeps the business plan moving so timing doesn't diminish performance.

For investors coming from operating businesses, this is often familiar territory. Exit rights, drag terms, buy-sell mechanics, and transfer restrictions can look a lot like private company deal terms in stock purchase agreements.

A projected return can survive a mediocre year. It often doesn't survive a delayed exit.

Frequently Asked Questions

How long does a typical private equity real estate fund last?

Most REPE funds are structured as closed-end vehicles with a finite life. The verified benchmark and government-backed material used here describes a typical 5–7 year lifecycle, often with extension rights in the fund documents. Investors should read those extension provisions closely because a stated term and an actual exit timeline aren't always the same thing.

What are the typical fees in a PERE fund?

The headline economics usually include management fees at the fund or asset level and carried interest or promote after investor hurdles are met. The exact percentages for management fees aren't provided in the verified data here, so the practical point is to review the LPA and side letters for hidden friction, including transaction fees, affiliate fees, disposition fees, and reserve practices.

Can I invest in a PERE fund as an individual?

Often yes, but eligibility depends on securities law exemptions, investor status, and the sponsor's onboarding requirements. In practice, many investors subscribe through corporations, trusts, or family office entities for tax, governance, and estate-planning reasons. Before choosing the subscriber, confirm that the entity aligns with both the fund's admission rules and your cross-border tax profile.

What is the biggest risk for a Limited Partner?

For a domestic investor, the largest risk is often loss of capital tied to poor underwriting or weak execution. For a Canadian LP entering a U.S. fund, I'd add structural risk. If the wrong entity subscribes, or the fund uses an LLC structure without proper blockers, you can inherit tax exposure and liability problems that don't show up in the marketing deck.

Do I need separate U.S. and Canadian advisers?

Sometimes, but not always. The key issue is whether your advisers understand how the structure behaves on both sides of the border. A clean Ontario corporate setup can still create U.S. tax problems. A well-drafted U.S. fund package can still create Canadian reporting issues. Coordination matters more than headcount.

If you're reviewing a first fund subscription, restructuring an existing cross-border holding vehicle, or trying to reduce tax and compliance risk before capital is called, Mayo Law can help you assess the structure before you sign.

Private equity funds real estate can be an effective way to scale beyond what your own balance sheet can support. They can also produce avoidable problems when investors accept fund documents at face value. The investors who do best usually slow down at the front end, test the structure, and treat tax, liability, and compliance as part of the investment itself. That's especially true once a U.S.-Canada element enters the deal.

How Mayo Law Can Help

Cross-border PERE investing often breaks down at the structuring stage, not because the asset is weak, but because the investor entered through the wrong entity or without proper tax and compliance review. Mayo Law serves clients across Toronto, the GTA, and on cross-border matters. To discuss your situation, visit international business counsel.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.