Published: July 5, 2026

Updated: July 5, 2026

Read time: 9 minutes

A client sends over onboarding paperwork. A payment platform asks for a taxpayer identification number. Your bank wants business documents before opening an account. If you’re a solo founder, freelancer, or consultant, the question lands fast: is your Social Security Number enough, or do you need an EIN?

That question gets harder when your work crosses the U.S.-Canada border. A Toronto founder serving U.S. customers, or a New York sole proprietor billing Canadian clients, often runs into privacy, banking, and paperwork issues that generic U.S. guides skip. At Mayo Law, we help entrepreneurs in Toronto, the GTA, and across the border handle business structuring issues that often touch both Ontario and New York.

The short answer is simple. Many sole proprietors don’t legally need an EIN. But many should still get one.

When Is an EIN Legally Required for a Sole Proprietor

A sole proprietor gets pulled into EIN territory once the business stops being a simple one-person operation for IRS purposes. The rule is narrower than many founders expect, but the consequences of getting it wrong are real. Payroll filings fail, bank onboarding stalls, and cross-border payments can trigger extra scrutiny if your tax paperwork does not match the structure you are using.

The core IRS triggers are straightforward:

- You hire employees. A sole proprietor with employees needs an EIN for payroll tax filings and wage reporting, as explained by Nolo on sole proprietors and EIN requirements.

- You file employment tax returns.

- You file excise tax returns.

- You withhold tax on income paid to nonresident aliens.

- You stop operating as a plain sole proprietorship and instead operate through a corporation, partnership, or Keogh plan.

For Canadian entrepreneurs entering the U.S. market, the fourth point gets overlooked. If you pay certain U.S. or foreign individuals in a way that creates U.S. withholding obligations, the EIN question can surface faster than expected. The same is true if a U.S. bank, marketplace, or payment processor asks for business tax identification to complete onboarding, even before the IRS strictly requires it for filing.

A simple rule works well here. If you are a one-owner business, have no employees, and do not file special tax returns, an EIN usually is not legally required. Once payroll, excise tax, nonresident withholding, or a new entity structure enters the picture, get the EIN before the filing deadline, not after.

If you are also sorting out whether your U.S. setup creates separate entity reporting duties, review these beneficial ownership reporting requirements alongside your tax ID decision.

Using Your SSN Versus an EIN for Your Business

A Canadian founder often hits this question early. A U.S. client wants a W-9, a payment processor asks for a tax ID, and the business is still just a one-owner operation. At that point, the legal answer and the practical answer are not always the same.

For federal tax purposes, a sole proprietorship usually reports under the owner’s personal tax identity. In many cases, that means you can use your SSN if you are operating as a plain sole proprietor and no separate EIN requirement has been triggered.

That is the minimum-compliance approach.

What using an SSN looks like

Using your SSN is simple at the start.

- No separate IRS application: You already have the number.

- Direct reporting: Business income and expenses are typically reported on your personal return.

- Fast launch: You can start invoicing and operating without waiting for a federal business tax ID.

For a freelancer with one or two clients, that may be enough. The trade-off is exposure. Each new client intake form, platform profile, or vendor setup creates another point where your personal identifier is stored outside your control.

What an EIN changes

An EIN is a federal business tax ID. It does not create a separate legal entity, and it does not change how a sole proprietor is taxed by itself. It gives you a business-facing number for forms, onboarding, banking, and tax administration.

That distinction matters in practice. If you are sending W-9s to U.S. customers, opening U.S. financial accounts, or signing up with marketplaces that expect business credentials, an EIN usually presents cleaner than an SSN. It also avoids making your personal identifier part of routine commercial paperwork.

I often see this issue with cross-border founders who start informally. One U.S. client does not feel like much. Then a bank asks for tax documentation, a platform requests account verification, and a second or third payer wants the same details. Using an EIN keeps those requests from turning into repeated disclosure of your SSN.

If you are still deciding whether to remain a sole proprietor or set up an LLC or corporation, review choosing the right entity for your U.S. business. The tax ID decision is easier once the entity decision is clear.

| Issue | Using SSN | Using EIN |

|---|---|---|

| Federal tax ID for a plain sole proprietor | Usually allowed | Also allowed |

| Privacy on client and vendor forms | Lower | Better |

| Business banking and platform onboarding | Can be more awkward | Often cleaner |

| Cross-border administration for Canadian founders | More personal disclosure | More business-facing |

| Future hiring or structural changes | Less flexible | Better positioned |

An EIN does not fix entity, tax residency, or withholding issues. It does reduce how often you have to hand out your personal tax identifier in the ordinary course of business.

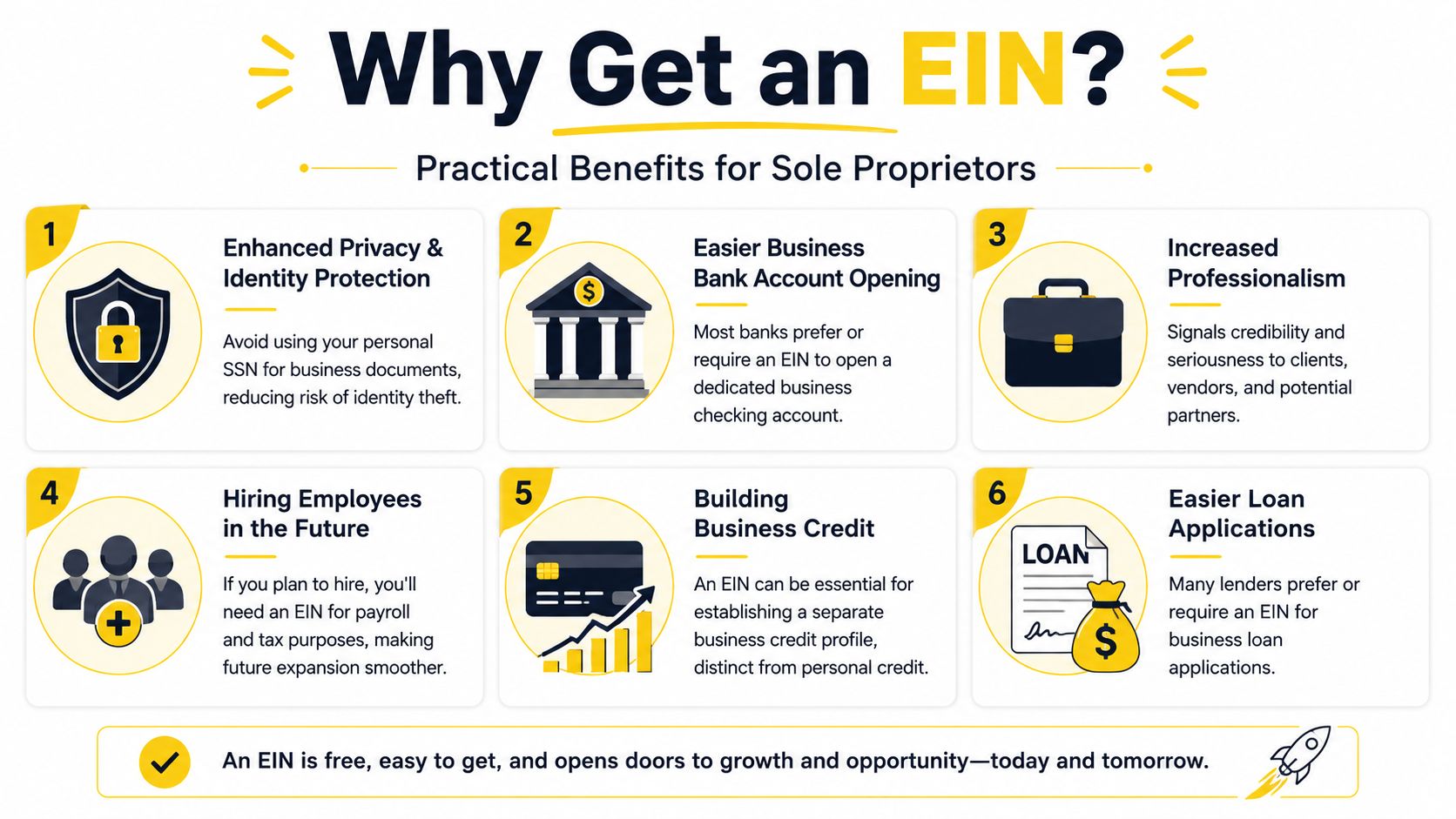

Practical Benefits of an EIN Even When Not Required

A founder in Toronto lands a first U.S. client, then gets asked for a tax form, vendor setup details, and banking information in the same week. At that point, the question is no longer whether an EIN is strictly required under IRS rules. The question is whether continuing to use a personal identifier creates avoidable friction.

Privacy matters more than most founders expect

The IRS may allow a sole proprietor to use an SSN. That does not make widespread commercial use a good practice.

Each time you provide an SSN on a client onboarding form, payment processor application, contractor file, or vendor record, you increase the number of places where your personal tax identifier is stored. For Canadian entrepreneurs entering the U.S. market, that risk is easy to underestimate because the requests often come from ordinary business operations, not from tax authorities. An EIN gives you a business-facing identifier for routine paperwork and reduces how often your personal number circulates across companies and systems you do not control.

That is a practical risk-management choice, not just a tax choice.

Banking is often easier with an EIN

Banks and payment providers look for consistency between the name of the business, the tax forms on file, and the account they are being asked to open or service. A sole proprietor can sometimes open accounts without an EIN, but many institutions treat an EIN as cleaner evidence that the activity is business-related rather than purely personal.

This point matters more in cross-border setups. A Canadian founder opening a U.S. business account or merchant account often faces extra review already. Presenting a business tax ID can make the file easier to process and easier to explain.

Business credit and lender readiness

An EIN does not separate you from your sole proprietorship in the way a corporation can. It does, however, help create a clearer administrative record for the business itself.

That can help when you apply for a business credit card, set up supplier accounts, complete marketplace verification, or respond to lender diligence requests. Many founders wait until financing is on the table before cleaning this up. By then, they are rebuilding records under time pressure.

Cross-border professionalism

Cross-border counterparties often expect business credentials, even where the law still permits a less formal setup. A U.S. client may be uneasy seeing a personal identifier on business paperwork. A Canadian service provider supporting your U.S. operations may not know why your SSN appears in its records at all.

An EIN helps present the relationship as business-to-business. That can make contract intake, accounts payable setup, and platform onboarding more straightforward.

Two common examples come up often:

- A freelance consultant in Toronto with U.S. clients: The first engagement starts informally, but the client's finance team asks for tax documentation and vendor registration. Using an EIN usually creates a cleaner file.

- A U.S. sole proprietor selling into Canada: The owner may be permitted to use an SSN, but may reasonably prefer not to distribute that number to Canadian distributors, bookkeepers, or software providers.

An EIN does not solve entity classification, U.S. tax residency, withholding, or permanent establishment issues. It does solve a narrower problem well. It lets you keep your personal tax identifier out of routine business circulation where there is no good reason to use it.

When Business Changes Force You to Get an EIN

A sole proprietor in Ontario may start with one U.S. client and no staff. Six months later, that same business hires a part-time assistant, opens a retirement plan, or brings in a U.S. partner. At that point, the EIN question stops being optional and becomes a compliance issue.

The rule is simple. If the facts of the business change, the tax ID analysis can change with them.

Do I need an EIN if I hire my first employee

Yes. Once you hire an employee, you need an EIN for payroll reporting, wage statements, and related tax filings.

This catches founders by surprise because the trigger is the first employee, not a larger team. If you are a Canadian owner using U.S. workers or setting up U.S. payroll, get the EIN in place before payroll goes live. Cleaning this up after wages have already been paid is harder and more expensive.

Do I need an EIN if I set up a retirement plan

Often, yes. Certain retirement plan arrangements, including a Keogh plan, can trigger the need for an EIN.

This issue is easy to miss because founders usually focus on hiring, banking, or contracts. Retirement plan paperwork can create its own filing requirements. Confirm the tax setup before the plan is adopted, not after.

Do I need a new EIN if I form a partnership or corporation

Yes. If the sole proprietorship becomes a partnership because you add an owner, or you incorporate the business, you generally need a new EIN tied to that new tax structure.

The same point applies in bankruptcy situations that change how the business is treated for tax purposes.

Founders often assume the old number can stay with the business name. Usually it cannot. The legal form controls. That matters in cross-border work because U.S. banks, payment processors, and counterparties often key their records to the exact taxpayer identity. If your structure changed but your tax ID paperwork did not, onboarding delays usually follow.

What if I only change my name or address

A name change or address change usually does not require a new EIN.

That is an administrative update, not a new taxpayer identity.

What about a single-member LLC

A single-member LLC does not automatically require a separate EIN just because the LLC was formed. The filing obligations matter. If the LLC has employees or must file certain federal tax returns, the answer can change.

That distinction causes confusion for sole proprietors who form an LLC for liability or contract reasons and assume the EIN rules changed at the same time. Sometimes they did. Sometimes they did not. If you are weighing whether to stay a sole proprietorship or switch structures, it helps to compare the legal and tax consequences together. See LLC vs corporation in New York and which to choose.

Forming an LLC does not answer the EIN question by itself. The required tax filings do.

Another trigger gets overlooked. If you buy or inherit a business and continue operating it as a sole proprietorship, you should not assume the prior owner's tax ID carries over. In practice, this is a point to verify early, especially in family transitions or cross-border acquisitions where ownership records are often less tidy than the parties expect.

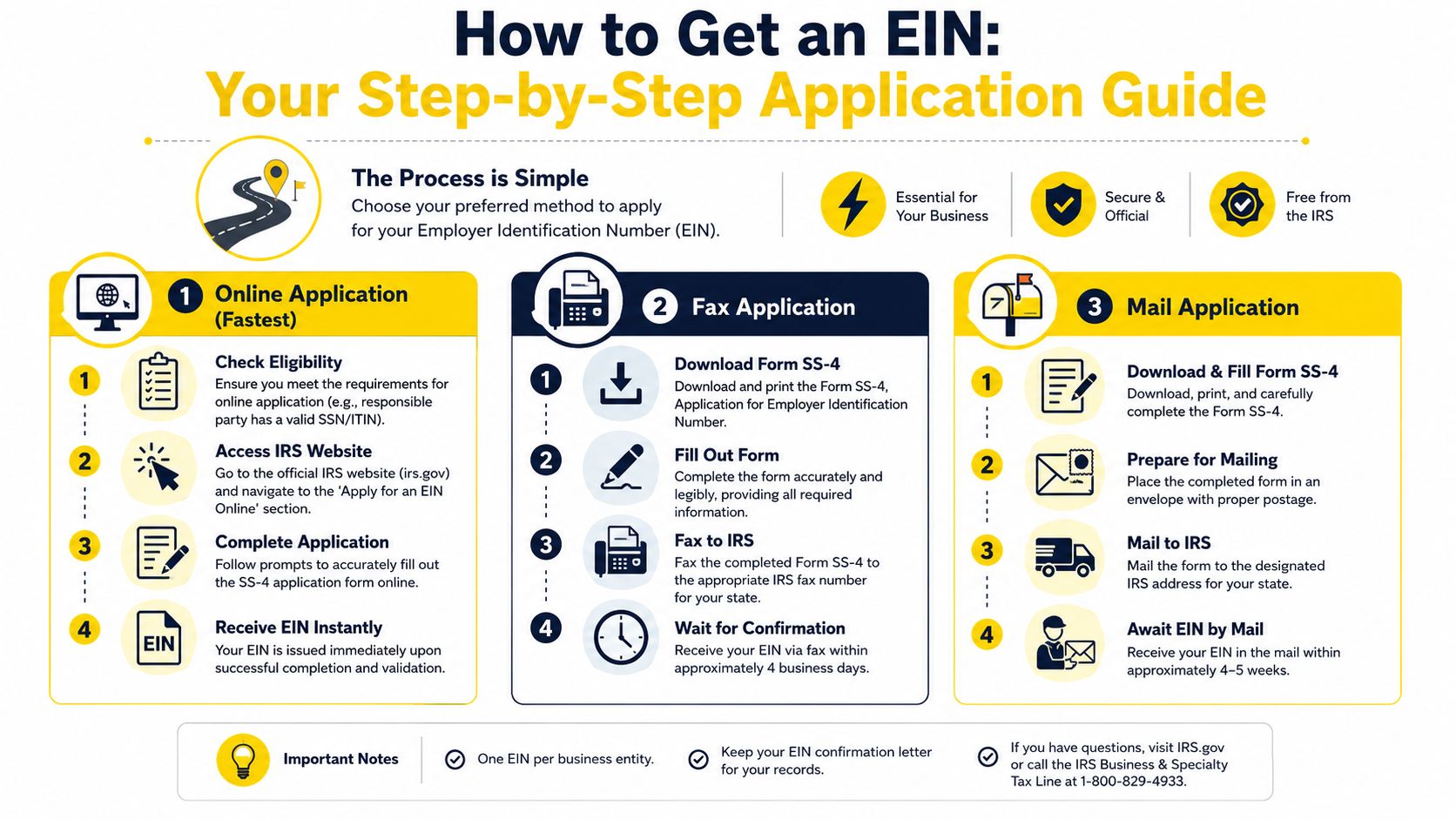

How to Apply for an EIN A Step-by-Step Guide

A common scenario is a founder who is ready to open a U.S. bank account, onboard with a payment processor, or send tax forms to a U.S. client, then realizes the tax ID question has to be dealt with first.

Start with the right application method

If you are eligible for the IRS online application, use it. It is the fastest option for many U.S.-based applicants, but the session can time out if you leave it idle, so gather your details before you begin.

If the online system does not fit your situation, use Form SS-4. That is often the practical route for applicants with cross-border facts, identity mismatches across records, or filing constraints that make the online flow less reliable.

Have your information ready before you apply

Small errors cause avoidable delays. The IRS, banks, and payment platforms compare the application against other records, and those records do not always forgive inconsistencies.

Before starting, confirm:

- Owner name and business name: Use the same spelling and order that appears on your tax and banking records.

- Mailing address: Use the address where you can receive IRS correspondence.

- Reason for applying: Hiring employees, opening a bank account, changing structure, and vendor onboarding can all lead to different follow-up questions.

- Entity classification: Sole proprietor, single-member LLC, partnership, and corporation are different categories. Choosing the wrong one creates cleanup work later.

- Responsible party details: The IRS will want the individual who controls or owns the business.

For Canadian entrepreneurs, this step matters more than it seems. If your Canadian business records, U.S. client contracts, and IRS application describe the business differently, onboarding problems usually show up before the first payment does.

Treat the EIN confirmation like a core business record

Once the EIN is issued, keep the confirmation notice with your formation, tax, and banking documents. You will likely need it again for a bank, payroll provider, marketplace, or withholding form review.

Cross-border businesses should also think about document handling early. If supporting records need to be recognized in another jurisdiction, proper certification and document authentication services can matter as much as the EIN itself.

Practical filing point

Do not rush through the form just because the application looks short. In practice, the hard part is not getting the number. The hard part is making sure the name, address, ownership, and entity description match the rest of your U.S. and Canadian paperwork.

An EIN for Canadian Entrepreneurs Doing US Business

Here, the generic advice usually breaks down.

A Canadian sole proprietor doing business in the U.S. may not start from a U.S. SSN-based framework at all. Even so, U.S. counterparties often want a federal tax identifier attached to onboarding, payment, or tax forms. In practice, an EIN can become the cleaner business credential for a Canadian founder with U.S.-source activity.

Why cross-border founders often get one early

A Toronto consultant billing a New York client may find that the client wants tax paperwork, vendor setup, and banking details before the first payment goes out. A U.S. marketplace or payment processor may also ask for business identification that fits its internal compliance flow.

The legal point is one thing. The commercial point is another. If the U.S. side expects a business identifier, an EIN often removes friction.

Privacy is a bigger issue across the border

Cross-border files move through more hands. Clients, accounting teams, payment processors, and compliance staff may all touch the onboarding package. If a U.S. sole proprietor can avoid circulating an SSN into that chain, an EIN is usually the better practice.

For Canadian entrepreneurs expanding south, the same principle applies in reverse. Keep the founder's personal identifiers as contained as possible.

Cross-border business runs on documents. Small mistakes in names, tax IDs, and entity descriptions can slow payment, banking, and later immigration or investment planning.

It also helps future-proof the business

Many founders start with one contract and later pursue a U.S. subsidiary, investor visa planning, or a formal entity. Getting the tax ID side organized early often makes the next step easier.

If your operations are starting in both countries at the same time, structure and tax ID choices should be made together. See starting a business in both Canada and the US.

Frequently Asked Questions

How much does it cost to get an EIN

An EIN from the IRS is free.

The caution point is practical. Many filing services charge for submitting the application, and some founders do not realize they are paying a third party for something the IRS issues without a government fee. For a Canadian entrepreneur entering the U.S. market, the main cost is usually delay caused by mismatched names, addresses, or responsible party details across tax forms, banking documents, and incorporation records.

Do I need a new EIN if I change my business name or move

Usually no. A sole proprietor generally does not need a new EIN just because the business name changes or the address changes.

A new EIN is more often tied to a real change in tax or legal status, such as bringing in a partner, incorporating the business, or entering bankruptcy. Name and address updates still need to be handled properly with the IRS and with banks, payment processors, and vendors. In cross-border files, inconsistent records create avoidable compliance questions.

Can a non-U.S. citizen get an EIN

Yes, many non-U.S. citizens can get an EIN.

The harder issue is process. Some applicants cannot use the online system and must apply by Form SS-4 through manual channels. That tends to matter for Canadian founders because U.S. onboarding often starts before the tax file is fully organized. If the legal name, trade name, entity type, and owner information do not match across the application and the supporting paperwork, the delay usually shows up at the worst time, during banking, platform approval, or first-client onboarding.

What is the difference between an EIN, ITIN, and SSN

An SSN is a personal U.S. taxpayer identification number. An ITIN is also a personal tax number, used by individuals who are not eligible for an SSN. An EIN is a business tax identifier issued for a business or business-related tax administration.

That distinction matters in practice. A sole proprietor may be allowed to use a personal number in some settings, but using an EIN often reduces how often that personal identifier gets shared. For founders doing business between Canada and the U.S., that privacy benefit is not theoretical. Tax forms, vendor packets, and payment onboarding documents often pass through several organizations before payment is released.

What happens if I was supposed to get an EIN but didn't

The problem usually appears when the business outgrows the original setup.

Payroll reporting can be wrong. Vendor forms can be rejected. A bank may freeze onboarding until the tax ID issue is fixed. If the business has already hired workers, changed entity type, or started filing on a basis that no longer matches a sole proprietor using an SSN alone, the cleanup can take time and can require corrected filings.

Conclusion

If you're asking whether sole proprietors need an EIN, the legal answer is often no. The practical answer is often yes. An EIN can protect your privacy, reduce friction with banks and clients, and make growth easier when your business changes shape.

That is especially true if your work touches both the U.S. and Canada. The right choice depends on how you operate now, what documents you are being asked to provide, and where the business is headed next.

If you're weighing SSN use against an EIN, or setting up a U.S. business with Canadian ties, Mayo Law advises founders on cross-border business structure, compliance, and startup documentation so the paperwork matches the reality of the business. A short legal review at the start is often cheaper than fixing tax ID, banking, or entity problems later.

How Mayo Law Can Help

A Canadian sole proprietor selling into the U.S. can run into problems long before tax filing season. Banks may ask for an EIN, a platform may request U.S. business details, or a client may reject forms that show a personal identifier. Those issues are easier to prevent than to fix after accounts are opened or contracts are signed.

Mayo Law advises founders who need the legal setup to match how the business operates across Canada and the U.S. That includes choosing the right structure, reviewing whether an EIN should be obtained now or later, and aligning tax ID, contracts, banking, and registration steps so they do not conflict.

The goal is practical. Reduce privacy exposure, avoid avoidable banking friction, and set up documents that support growth instead of creating cleanup work later. Mayo Law serves clients in Toronto, across the GTA, and on cross-border business matters.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

- International business legal services

- Regulatory compliance legal services

- Business immigration legal services