Published: June 28, 2026

Updated: June 28, 2026

Read time: 11 minutes

You’ve closed the credit committee calls, agreed the term sheet, and lined up funding for U.S.-Canada expansion. Then the lender sends one more document: a Deposit Control Account Agreement. If you’re a CFO or founder, this is usually the point where the deal stops feeling commercial and starts feeling operational. Suddenly your main cash account is part of the collateral package, and the core question becomes simple. Who controls your money if the relationship turns?

At Mayo Law, we help businesses in Toronto, the GTA, and across the border handle financing documents that affect both legal rights and day-to-day operations, with experience licensed in both Ontario and New York on a process that often spans both sides of the border. A deposit control account agreement isn’t exotic. It’s standard secured lending machinery. But the drafting choices matter a great deal, especially where a U.S. lender, a Canadian operating company, and a third-party bank are all involved.

One borrower may be comfortable with a springing arrangement because it preserves working capital access until a trigger event. Another may discover that an account freeze would interrupt payroll, tax remittances, or supplier payments on both sides of the border. The paper looks technical. The business consequences are not.

What Is a Deposit Control Account Agreement?

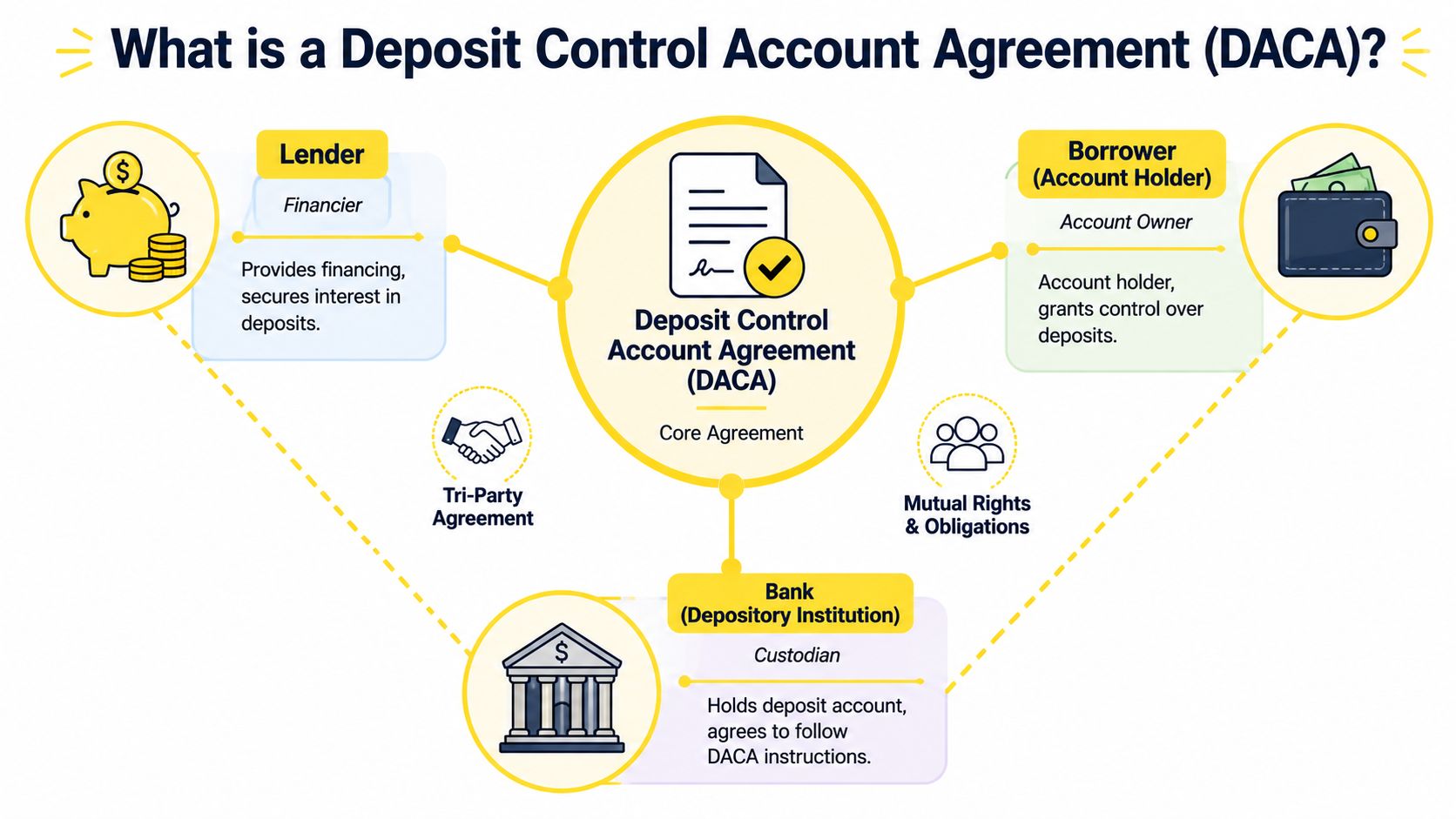

A Deposit Control Account Agreement is a tri-party contract between a borrower, a lender, and a bank that gives the lender legal control over a deposit account for collateral purposes. Under UCC Article 9, that control is what allows the lender to perfect its security interest in the account and claim priority if the borrower becomes insolvent.

The legal point is narrower than many borrowers expect. A lender doesn’t ask for this document just to monitor balances. It wants enforceable rights against the account itself. Under the Uniform Commercial Code, perfection by control is the exclusive and mandatory means for perfecting a security interest in deposit accounts when they serve as primary collateral, as explained in Liskow’s discussion of account control under the UCC.

That’s why this agreement often appears late in a deal but becomes critical very quickly. Without it, the lender may have no priority claim to those funds. With it, the account becomes usable collateral in commercial lending and structured finance.

Who Are the Parties to a DACA?

A DACA works because each party signs for a different reason, and those reasons do not fully align.

The borrower

The borrower is the account holder and the operating business. It wants the financing, but it also wants to preserve practical control over receipts, disbursements, and treasury routines. In cross-border deals, that usually means protecting cash movement between a U.S. parent, a Canadian subsidiary, or parallel operating entities.

For the borrower, the hard question isn’t whether the lender gets collateral support. It’s how much operating friction the agreement creates before any default occurs. A borrower can live with a security package on paper. It struggles when ordinary-course payments become uncertain.

The lender

The lender is the secured party. Its goal is to make the deposit account recoverable collateral, not merely a promise in the loan agreement. Under the verified legal framework, a DACA is designed to perfect the lender’s security interest under UCC § 9-104, and the depository bank agrees to follow the lender’s instructions regarding the borrower’s cash without further action by or consent of the borrower.

From the lender’s side, ambiguity is the enemy. If trigger mechanics are vague, if the account name is wrong, or if the bank’s setoff rights remain intact, the collateral package may fail when it matters most.

The bank

The depository bank often appears neutral, but it has its own risk concerns. It is being asked to accept instruction protocols, recognize the lender’s control rights, and usually waive or subordinate its own competing claims except for ordinary service fees and returned unpaid deposits.

Banks also care about administration. Who can send notices? In what form? When does the bank stop honoring the borrower’s instructions? What if instructions conflict?

Practical rule: Many DACA disputes are not about lofty legal theory. They begin with a bank operations team trying to apply a document that the deal team signed months earlier.

This is why related collateral documents need to line up. If your financing package also includes contract collateral or revenue rights, your counsel should check whether those pieces work together with the account control structure. That issue often overlaps with assignment of contract considerations.

Decoding Typical DACA Provisions

Most DACAs use familiar language, but the commercial outcome depends on a handful of clauses. On these points, borrowers often sign too quickly and lenders sometimes overreach.

Control language

The control clause is the center of the agreement. It states that the bank will comply with the lender’s instructions regarding the account without requiring further borrower consent. That sounds abstract until you translate it into operations.

If the lender can instruct the bank unilaterally after a trigger event, the borrower may lose practical access to incoming receipts immediately. If the language is active from signing, the borrower may never have that access in the first place.

A lender should want clarity. A borrower should want limits. The clause should identify the exact accounts, exact legal names, and exact instruction path. If any of those are wrong, the agreement can become hard to enforce or easy to dispute.

Trigger events

This is usually the first negotiated issue because it determines when control shifts in practice. According to Stripe’s explanation of passive and active DACA structures, in a passive DACA the borrower keeps day-to-day control unless a trigger event such as a missed payment, bankruptcy filing, or covenant breach occurs. In an active DACA, sometimes called a blocked account arrangement, the lender has immediate and complete control from the outset.

That legal distinction has an obvious business effect:

- Passive or springing DACA: Better for operating flexibility.

- Active or blocked DACA: Better for immediate lender protection.

- Poorly drafted trigger definition: Bad for everyone.

Borrowers should push for objective trigger events. “Material default” is less useful than a defined payment default, insolvency filing, or uncured covenant breach. Lenders should resist triggers that require prolonged factual debate before the bank can act.

Borrowers often focus on whether there is a trigger. The real issue is whether the trigger can be proven quickly and administered cleanly.

Sweep mechanics

Once control shifts, money has to move somewhere. The DACA should specify whether the lender can direct a freeze, a sweep to a designated account, or both. Timing matters. If funds arrive after a notice is delivered, does the bank continue to process automatic payments? Does the bank batch sweeps at end of day, or act immediately?

Treasury staff involvement is essential. Legal language that ignores actual payment rails creates avoidable disruption. I’ve found that the best agreements are drafted with finance and operations in the room, not only external counsel.

Payment priorities

A good DACA states who gets paid from the account and in what order. The bank typically preserves rights for ordinary service fees and returned unpaid deposits. The lender wants priority over the remaining balance. The borrower wants clarity on whether any carve-outs survive after control shifts.

If the document is silent, everyone may assume something different. That is how disputes start.

A short priority table inside the agreement often helps:

| Payment item | Typical treatment |

|---|---|

| Ordinary bank service fees | Usually preserved for the bank |

| Returned unpaid deposits or chargebacks | Usually preserved for the bank |

| Lender-directed transfer after trigger | Subject to control rights |

| Borrower operating payments | Only if expressly permitted |

Waiver of setoff

This clause matters more than many borrowers realize. Banks commonly have rights of setoff or liens under general account terms. In DACA practice, lenders often require the bank to waive its right of setoff and subordinate existing liens on the account except for ordinary service fees and returned unpaid deposits.

If that waiver is weak, the lender's expected priority can be diluted. If it is too broad, the bank may resist signing at all. The drafting needs to reflect the actual operational relationship between bank and customer.

Permitted payments and carve-outs

Practical negotiation earns its keep. Many businesses can tolerate lender control after a serious default. Few can tolerate a sudden stop on payroll, source deductions, tax payments, or critical vendor obligations that preserve enterprise value.

A borrower should ask for narrow carve-outs where the lender's risk profile allows it, especially in a springing arrangement. Examples include:

- Payroll and remittances: Limited continuation for a short transition period.

- Ordinary bank fees: Expressly permitted so the account remains functional.

- Critical suppliers: Only where interruption would reduce collateral value.

- Tax payments: Often important in cross-border groups with parallel obligations.

In some deals, these issues overlap with software escrow, customer collections, or licensed technology dependencies. If a company's revenue engine depends on access to code, platforms, or hosted infrastructure, account control should be reviewed alongside software in escrow arrangements.

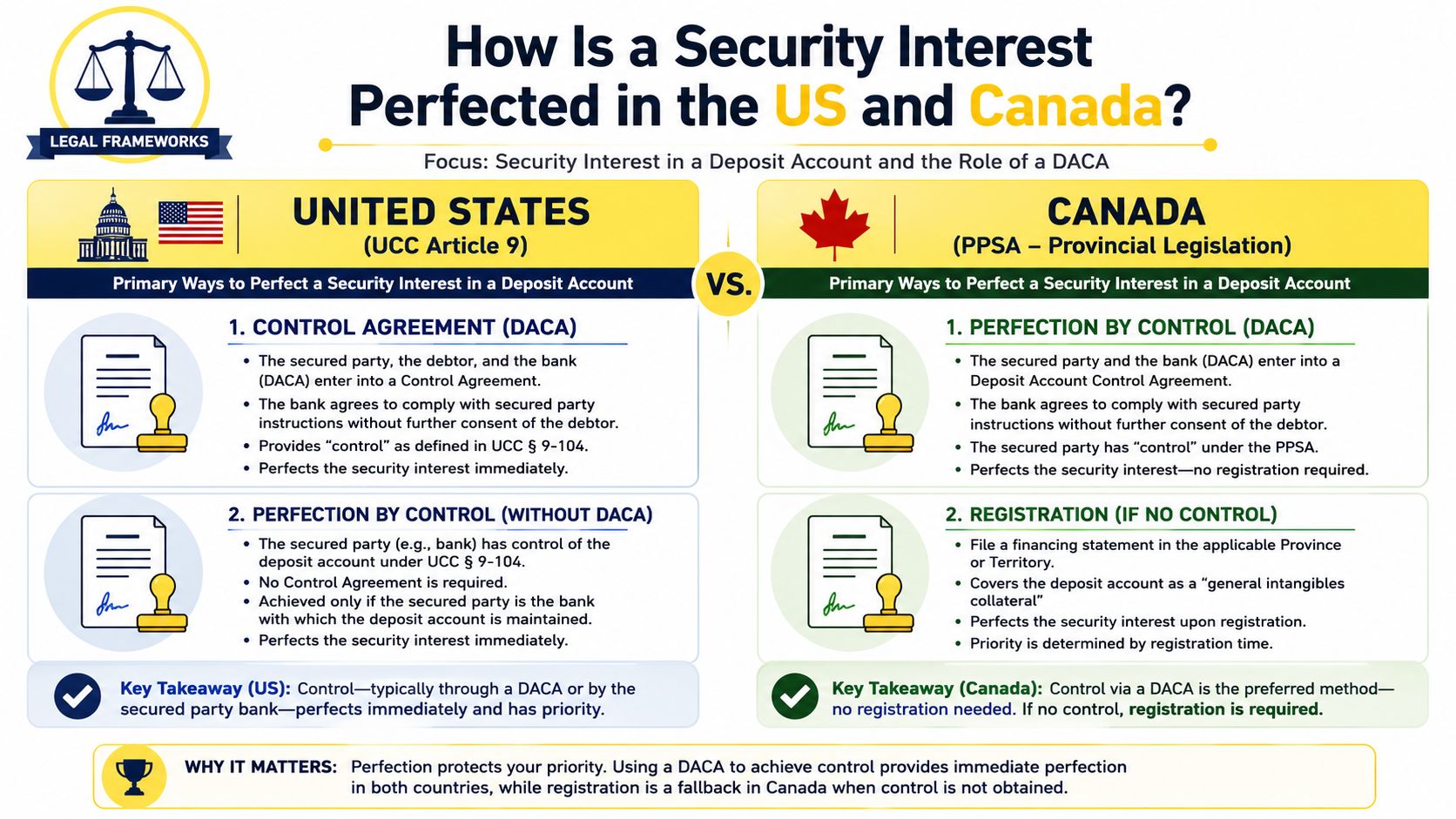

How Is a Security Interest Perfected in the US and Canada?

The U.S. and Canadian systems solve a similar problem, but they don't always use the same instrument or timing model.

In the United States, a DACA is a tri-party legal contract between the borrower, the secured lender, and the third-party depository bank, expressly designed to perfect the lender's security interest in the borrower's deposit account under Article 9 of the Uniform Commercial Code, UCC § 9-104. The point of perfection is priority. If insolvency happens, the lender needs a legally recognized claim that ranks ahead of competing creditors.

In Canada, especially in common-law provinces, the comparable document is usually a Blocked Account Agreement or BAA. It also involves the borrower, lender, and bank. But standard Canadian forms often restrict borrower access immediately rather than waiting for a springing trigger, although springing BAAs also exist.

US DACA vs. Canadian BAA at a glance

| Feature | United States (DACA) | Canada (BAA) |

|---|---|---|

| Main legal framework | UCC Article 9 | Provincial secured transactions law in common-law provinces |

| Typical purpose | Perfection by control over deposit account | Transfer of account control to support cash collateral enforcement |

| Borrower control before default | Often preserved in passive or springing forms | Often restricted immediately in standard blocked forms |

| Bank instruction model | Bank follows lender instructions without further borrower consent | Bank recognizes lender’s authority over the subject account |

| Commercial use | Secured lending and structured finance | Asset-based lending and cash collateral structures |

The trap in cross-border deals is assuming the U.S. form can be used as-is in Canada. It often can't. A U.S. lender may expect a springing control structure because that is common in its market. A Canadian bank may be more comfortable with immediate restrictions if its standard blocked account language works that way.

Cross-border friction usually appears when the parties agree on economics but use different assumptions about when control shifts and how the bank administers instructions.

There's also a process point. If signatures, notarization, or supporting certificates have to move between jurisdictions, the closing checklist should reflect that early. In practice, execution problems delay these agreements more often than parties expect. For related cross-border document formalities, businesses often need Ontario notary support.

For statutory reference, businesses dealing with U.S. perfection should review the Uniform Commercial Code material made available through New York State resources and corporate teams working in Canada should confirm provincial secured transactions requirements through the relevant Ontario government legal and business resources.

Drafting and Negotiation A Practical Checklist

Closing is set for Friday. The credit agreement is signed, the security documents are ready, and treasury assumes cash can keep moving on Monday. Then the depositary bank sends back its DACA markup with new notice contacts, a broad account freeze right on delivery of a notice, and no carve-out for payroll already queued in the system. That is a common failure point in U.S.-Canada deals. The legal issues are manageable. The operational mistakes are what create the true cost.

A workable DACA is one the bank can administer, the lender can enforce, and the borrower can live with if relations deteriorate. Drafting should be done with default-day mechanics in mind, not just closing-day signatures.

Borrower checklist

Borrowers should start with one question: which accounts need to be under control? Many companies agree too early to sweep in every operating account, then discover that routine cash management becomes harder than the lender intended.

Focus on these points:

- Define the trigger with precision: Use objective events tied to the loan documents. Avoid language that lets a contested default or administrative misunderstanding shut down account access.

- Ask for a short cure period for technical defaults: Reporting slips and minor covenant delivery failures should not produce the same result as a payment default.

- Protect business-critical payments: If the account touches payroll, sales taxes, source deductions, pension contributions, or key supplier payments, deal with those items expressly in the text.

- List every relevant account and service: Include concentration accounts, zero-balance accounts, foreign currency accounts, lockboxes, sweeps, and any automatic transfers that treasury already uses.

- Match legal names exactly: The account holder name, borrower name, and grantor name need to line up across the account records, security agreement, and closing certificates.

- Review the document with treasury, not only legal: ACH pulls, pre-authorized debits, wire templates, returned items, and bank cutoff times often matter more in practice than a heavily negotiated recital.

Borrowers also need to ask what happens in the gap between notice and implementation. Some banks can stop outgoing payments quickly. Others need internal processing time. If the DACA says control shifts immediately, but the bank's operations team acts later, both sides are exposed to avoidable disputes.

Lender checklist

Lenders usually focus on getting control language signed. That is only part of the job. The harder question is whether the arrangement will hold up when someone sends a notice under pressure.

Review these items before closing:

- Make the bank's instruction standard clear: The bank should agree to follow the secured party's instructions without further consent from the borrower once the notice becomes effective under the agreement.

- Address the bank's competing rights: Setoff, account fees, returned item claims, and overdraft exposure should be waived or subordinated to the extent negotiated, with carve-outs stated clearly.

- Stress-test the notice mechanics: Identify names, titles, email addresses, physical delivery details, and backup contacts. A DACA should still work if the primary relationship manager is unavailable.

- Check the collateral flow across borders: If collections move between U.S. and Canadian affiliates, the DACA should fit the actual cash path. Otherwise, the lender may control the wrong account while cash lands elsewhere.

- Confirm the account opening sequence with the depositary bank: Some institutions insist on their own onboarding order and will not accept a near-final form dropped on them at the end of closing.

- Assess the bank's operational capability: A signed form is less useful if the bank lacks a team that understands control notices, freezes, and post-notice account administration.

Bank capability is often underestimated. A smaller institution may agree to lender-friendly language, then struggle to execute it consistently across branches, treasury services, and deposit operations.

Bank-side questions the deal team should ask

Even if the bank is not your client, these questions should be answered before funds start moving:

- Who inside the bank has authority to place a stop or redirect instructions on the account?

- Are those steps available only during business hours, or can they be implemented after-hours?

- Will the bank insist on its own DACA form or a specific rider?

- Does the bank accept notice by email, secure portal, courier, or only wet-ink originals?

- How are pending wires, debit pulls, chargebacks, fraud holds, and returned items treated after a control notice?

- What fees will the bank continue to debit from the account after control shifts?

One sentence in the DACA rarely answers all of that. An operations call often does.

As noted in Vorys' discussion of deposit account control agreements, implementation risk is real when the depositary institution does not have clear internal processes for acting on lender instructions.

Cross-border points that are often missed

U.S.-Canada DACAs often fail at the edges of the structure, not in the core control clause.

- Entity mismatch: The borrower, pledgor, and account holder may not be the same entity. If a Canadian affiliate owns the account and a U.S. borrower owes the debt, the documents need to reflect that directly.

- Currency mismatch: If receipts come in Canadian dollars but the borrowing base, cash dominion test, or blocked account mechanics assume U.S. dollars, the agreement should deal with conversion timing and exchange-rate risk.

- Priority mismatch: A U.S. lender may assume its standard form resolves priority. In Canada, provincial PPSA issues, local bank rights, and account location analysis still need to be checked against the full collateral package.

- Notice mismatch: A New York-law notice clause may not fit a Canadian bank's internal signing and delivery requirements. Use notice mechanics the depositary institution will honor.

- Execution mismatch: Cross-border closings often require certificates, incumbencies, notarizations, or authentication steps that take longer than the finance team expects.

Execution planning matters most when documents or affidavits need to move across jurisdictions on a short timeline. If New York authentication is part of the closing set, review the apostille process for New York documents before the signing date, not after a bank or foreign recipient rejects the package.

A practical DACA checklist is simple: confirm who controls the account, when control shifts, how notice is delivered, what payments can still go out, what rights the bank keeps, and whether the cash path matches the legal structure. If those answers are clear, the document usually works. If they are vague, the dispute starts before enforcement does.

Frequently Asked Questions

Does every secured loan need a deposit control account agreement?

No. It usually matters when deposit accounts are part of the collateral package and the lender wants control rights against cash held at a third-party bank. In asset-based lending and structured finance, it is common. In other transactions, the lender may rely more heavily on different collateral or different account structures.

How much does it cost to put a DACA in place?

There is no standard published government fee for a DACA itself. Costs usually come from legal drafting, lender counsel review, and bank administrative requirements. The practical point is to ask early whether the bank charges its own implementation fee and whether amendments later will require a fresh round of approvals.

What happens if my business has accounts at multiple banks?

In practice, lenders often require DACAs for each third-party depository bank where the borrower keeps deposit accounts designated as collateral. That means a multi-bank treasury setup can create multiple negotiation tracks, each with its own operational forms and internal bank review process.

Can a DACA be terminated?

Yes, typically when the secured obligations are paid off or the lender releases its security interest, subject to the agreement's termination mechanics. The document should say who sends the release notice, what the bank must receive, and when ordinary borrower control resumes.

Is a Canadian blocked account agreement the same as a U.S. DACA?

Not exactly. They address similar cash-collateral concerns, but the market practice can differ. In common-law Canada, a BAA often restricts the borrower immediately, while many U.S. arrangements are springing and shift control only after a defined trigger event.

Conclusion

A DACA becomes important at the worst possible time. The week liquidity tightens, a borrower learns whether it still controls collections, and a lender learns whether its rights work on paper only or at the actual deposit bank.

That is why the right question is not whether the agreement is "market." The right question is whether the control mechanics match the borrower's cash cycle, the lender's enforcement plan, and the bank's operating procedures in both countries. In U.S.-Canada deals, small drafting choices can have outsized consequences, especially where the loan documents are governed by one system, the account is maintained in another, and treasury personnel are trying to keep payroll, taxes, and supplier payments running.

For borrowers, the practical focus is narrower than many guides suggest. Confirm who can issue instructions, what notice starts exclusive control, which accounts are covered, and which payments remain permitted after a trigger event. For lenders, the key factor is administrative enforceability. If the depository bank will hesitate, require extra forms, or route instructions through internal teams that were never reflected in the DACA, control may be slower and less certain than expected.

Good DACA drafting reduces that execution risk. It also prevents avoidable fights over sweeps, setoff, FX conversions, and conflicting instructions between Canadian and U.S. account management teams. For broader cross-border structuring support, see our international business lawyer services.

If your financing deal involves a deposit control account agreement, Mayo Law can help you review the control mechanics, coordinate U.S.-Canada documentation, and negotiate practical carve-outs that fit your operations.

How Mayo Law Can Help

A DACA often breaks down at the last mile. The credit agreement is signed, the security package looks complete, and then the depository bank pushes back on its form, its notice process, or who inside the bank can act on a control instruction.

Mayo Law helps borrowers and lenders address those points before they delay closing or weaken enforcement. Our work typically includes reviewing whether the control provisions match the actual account set-up, aligning U.S. and Canadian loan and security documents, and marking up bank forms that shift operational or legal risk in ways the parties did not intend.

In cross-border deals, we focus on the clauses that cause real friction. That includes exclusive control triggers, blocked account mechanics, bank setoff language, governing law mismatches, and the practical treatment of Canadian accounts tied to U.S. credit facilities. We also help treasury and finance teams confirm what can still be paid, by whom, and on what notice if a trigger event occurs.

Mayo Law serves clients across Toronto, the GTA, and on U.S.-Canada matters. If your financing deal involves a deposit control account agreement, we can help you assess the documents, identify negotiation points quickly, and get the control package into a form the parties and the bank can implement.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Every situation is different. Consult a licensed lawyer about your specific circumstances. Mayo Law provides legal services through Mayo Law PC in Ontario and Joseph Mayo PLLC in New York.

Related Articles

If you are working through a DACA in a U.S.-Canada financing, the related issues usually do not stop at account control. The same file often pulls in regulatory review, signing mechanics, and cross-border corporate housekeeping.